Quick Note: Above each graph is a URL, you can ignore this! They only appear as the WordPress theme for this website has an issue with embedding content.

Last year I made a series of presentations about market share across Scotland to the ten largest inbound tourist markets as identified by Visit Scotland. Now that 2024 has concluded and we have a years worth of data I thought it would be a good idea to revisit each of these markets in a bit more detail.

A disclaimer is needed here, I have done this from an airport neutral point of view, and it is very important to remember that just because a load factor is high, that does not necessarily mean that yields are high.

This particular post is focusing specifically on the Scotland-Ireland market, which is the sixth largest inbound tourism market for Scotland.

For those unfamiliar with the route networks and airlines below is a summary of the routes and airlines that operated flights in 2024;

- Aberdeen to Dublin with Aer Lingus and Loganair

- Edinburgh to Cork with Ryanair

- Edinburgh to Dublin with Aer Lingus and Ryanair

- Edinburgh to Knock with Ryanair

- Edinburgh to Shannon with Ryanair

- Glasgow to Cork with Aer Lingus

- Glasgow to Donegal with Loganair

- Glasgow to Dublin with Aer Lingus and Ryanair

To try and simplify this articles format I will do a general section which will provide a holistic overview of the market, then I will provide sections for each airports performance.

If you are only interested in a specific market segment use the list below to jump to the relevant section;

- Passenger Numbers By Month

- Passenger Numbers By Year

- Market Share Per Airport

- Route Specific Numbers

- My Final Thoughts

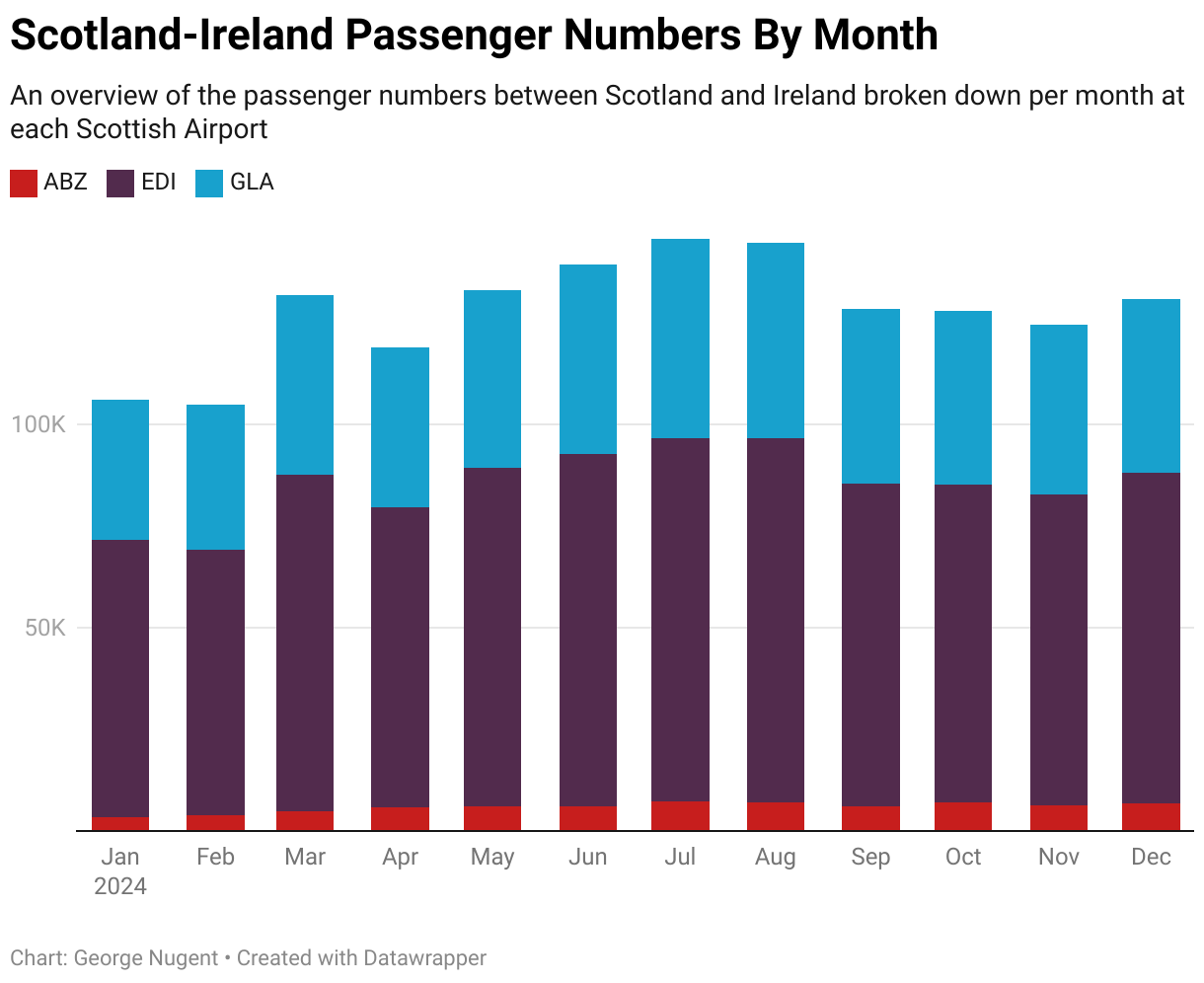

Passenger Numbers By Month

Passenger numbers between Scotland and Ireland typically remain stable throughout the year, with the two countries benefiting from a distinctive lack of seasonality between them.

At this point I should make a number of observations on this market, you can see them below;

- Aer Lingus is primarily connecting passengers from Scotland to their USA flights, therefore, Ireland is not their final destination.

- The Dublin Airport Passenger Cap significantly limited growth in Q4 of 2024, with the Dublin Airport Authority requiring airlines to cut flights to try and meet the cap. December was most impacted as airlines could not offer additional flights at Christmas like they did in 2023.

- March passenger numbers were boosted by Scotland playing Ireland in the Six Nations (coinciding with St Patrick’s Day), with a number of additional flights laid on the meet demand.

If the Passenger Cap at Dublin Airport had not been in place, it is therefore reasonable to assume that the 2024 growth rate would have been higher.

Edinburgh Airport remained the market leader throughout 2024, however, there was no single month when any airport had 100% of the market.

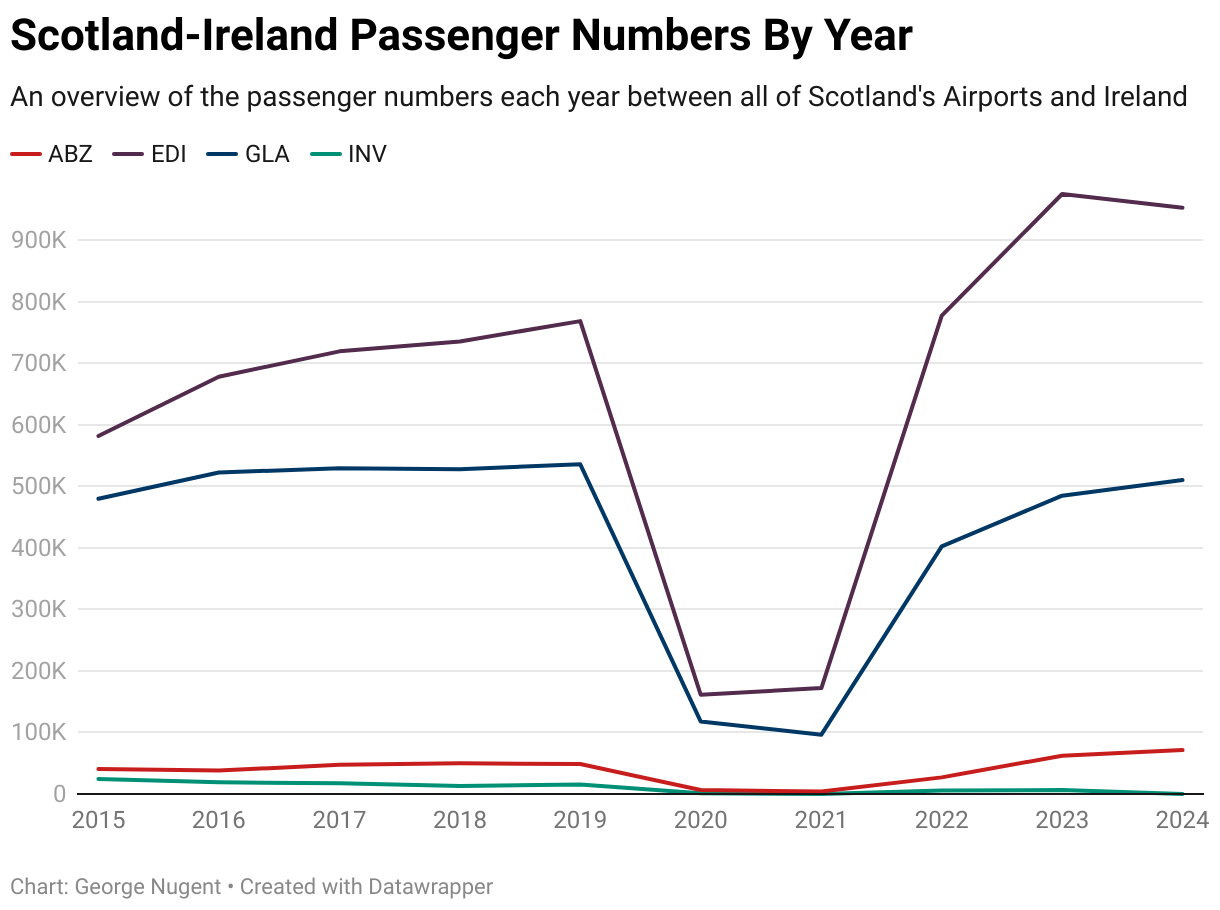

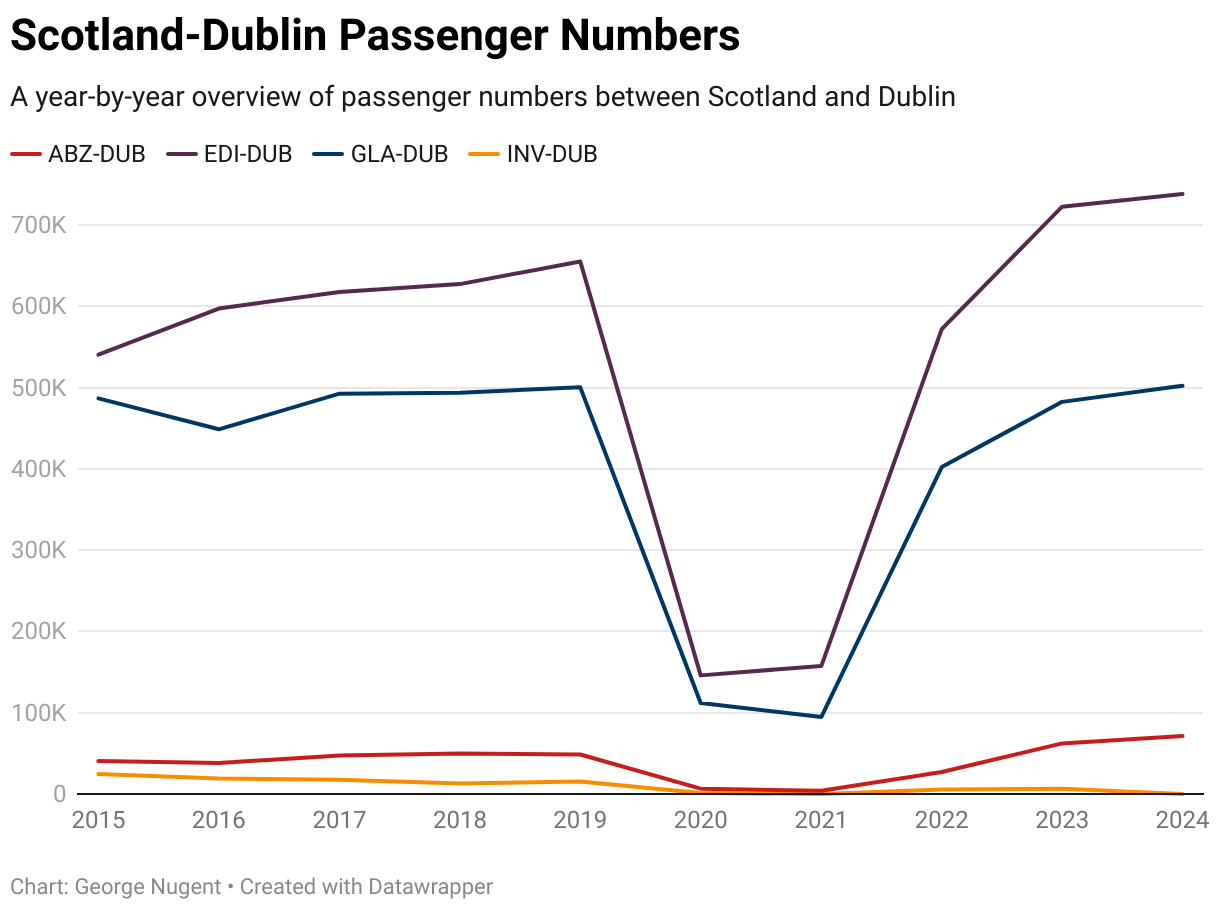

Passenger Numbers By Year

Compared to previous years, growth between Scotland and Ireland appears to have reduced in 2024, with the rate of growth slowing to 0.37%, likely a result of several factors including the Dublin Airport Passenger Cap and more direct US and Canada flights reducing the need to connect in Ireland.

Irish passenger numbers increased at Aberdeen and Glasgow Airports, but reduced at Edinburgh Airport, primarily fuelled by a reduction to regional airports such as Knock in summer, and constrained passenger numbers in winter on Dublin flights due to the cap.

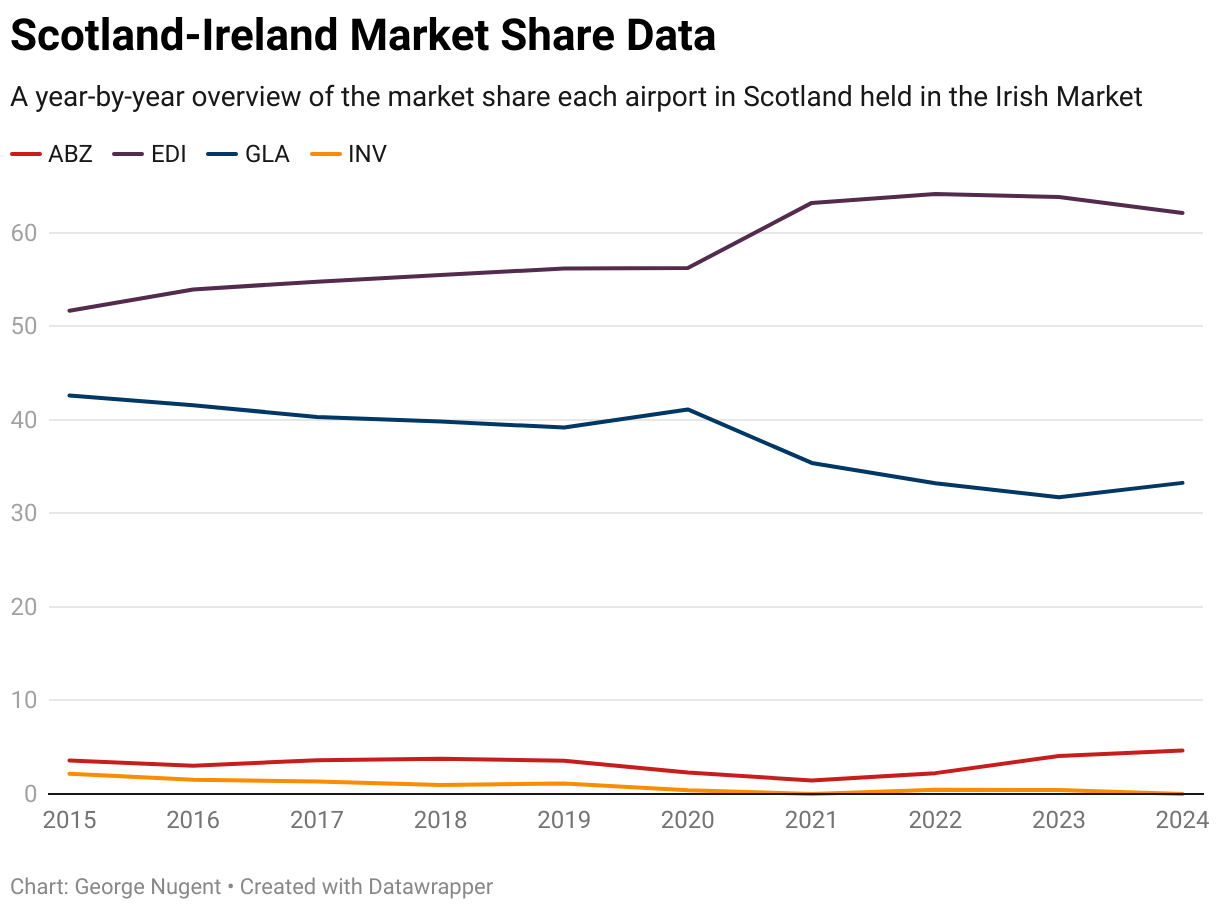

Market Share Per Airport

Edinburgh Airport has consistently held not only the largest share of the market, but crucially, the majority of the market, with the airport increasing its share year-on year before the pandemic.

When travel resumed in 2022, Edinburgh had significantly increased its market share when compared to Glasgow, however, in 2024 this trend appeared to be reversing slightly, however, a firm conclusion cannot be drawn from just one years worth of data.

Outside of the central belt, Aberdeen continues to increase its market share, and crucially, has both recovered and exceeded its 2019 share figure. One notable difference between Aberdeen and Edinburgh/Glasgow is the lack of Ryanair service, instead, Loganair is the second operator on the route alongside Aer Lingus.

In 2024, Aberdeen held 4.65% of the Irish market, Edinburgh held 62.09% and Glasgow held 33.25%.

Route Specific Numbers

To keep this post to a reasonable length, any routes that have only seen service from one Scottish Airport since 2015 will not have a graph, but rather a table showing the passenger numbers each year.

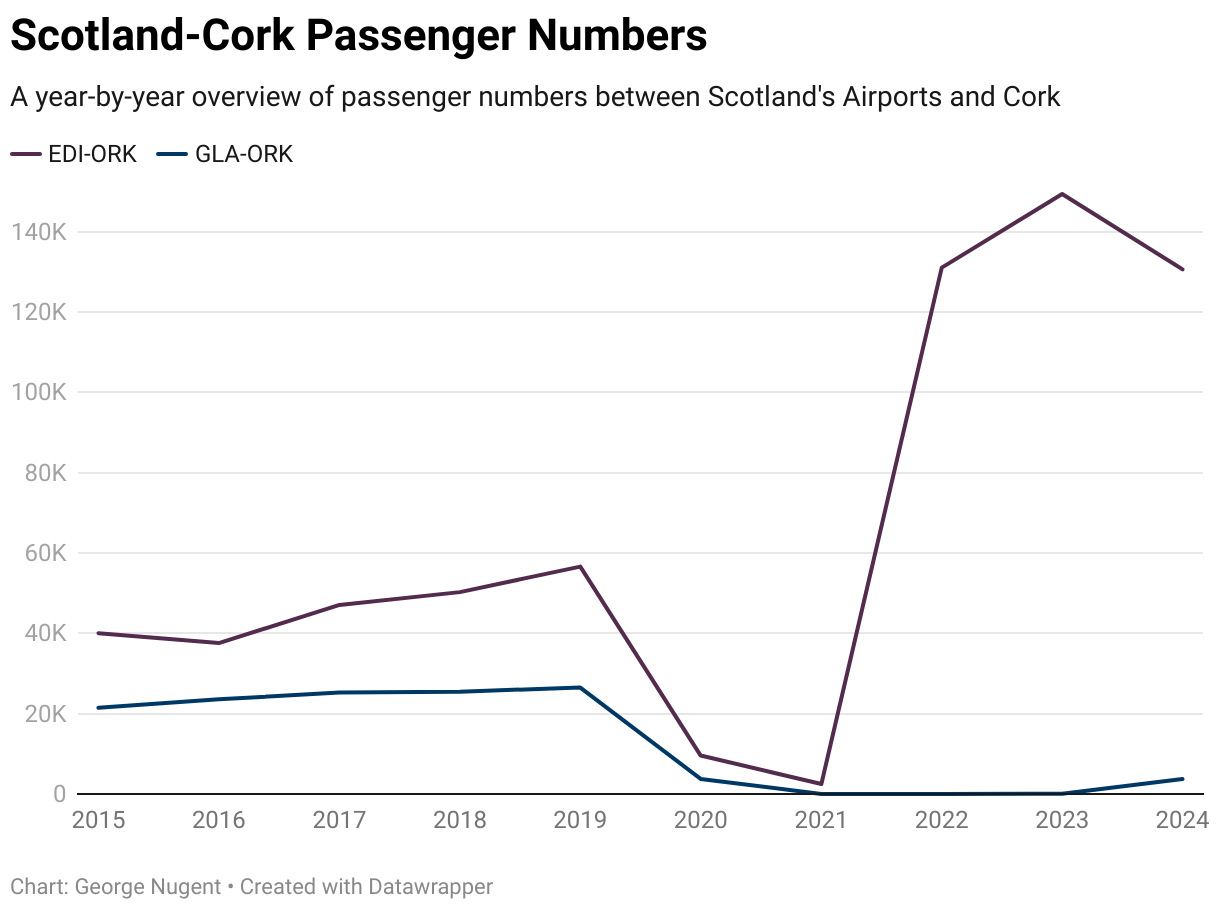

Cork

Sometimes a graph can say far more than words ever could!

This graph certainly is impressive, and on the surface reveals a lot, but it is important that I provide some context here;

- Until the pandemic both the Edinburgh and Glasgow flights were operated by Aer Lingus using ATR72 aircraft with 72 seats.

- When Stobart Air (who had the Aer Lingus Regional contract collapsed) Ryanair stepped in to provide a route between Edinburgh and Cork using their Boeing 737-800 and 737-8-200 aircraft with 189 and 197 seats respectively.

- Ryanair’s replacement flights commenced in December 2021 operating three times per week (the schedule has since grown)

- The use of larger aircraft allowed passenger numbers to grow despite less weekly flights, so growth using one metric but a reduction using another.

- Although Aer Lingus Regional resumed operations in February 2022 they only have operating bases in Belfast and Dublin with operations focused on linking these two cities to the UK.

- When Aer Lingus resumed their flights to Glasgow in October 2024 it is being operated by something known as a “W Pattern” (i.e. Belfast-Glasgow-Cork-Glasgow-Belfast)

As a result of Ryanair operating the Edinburgh route and not Aer Lingus, it has ultimately allowed passenger numbers on that route to soar, but, 2025 will need to finish in order to see how the Glasgow route impacts (if it even does) the Edinburgh flights.

Looking ahead to Summer 2025, the recently published “Start of Season Report“ for Edinburgh Airport shows the following for Cork flights;

- Ryanair will operate 480 movements (that’s 240 round trips) which is an increase of 60 on last year.

- The number of seats on offer will increase from 80,292 to 92,160 when compared to Summer 2024.

- Ryanair UK will also operate flights in Summer 2025, operating 60 movements (that’s 30 round trips), an increase of 60 on last year.

- The number of seats on offer will increase from 0 to 11,340.

When both subsidiaries are combined, the Ryanair Group will operate 540 movements (260 round trips), with 103,500 seats provided.

Moving over to Glasgow Airport, the recently published “Start of Season Report” shows the following for Cork flights;

- Aer Lingus will operate 240 movements (120 round trips), as this is a new route for 2025 this is an increase of 240.

- These flights will provide 17,280 seats

Donegal

Donegal has always been an exclusive route to Glasgow Airport and is currently operated by Loganair.

Passenger numbers since 2015 can be seen in the table below;

| Year | Passenger Numbers |

|---|---|

| 2015 | 9,401 |

| 2016 | 11,829 |

| 2017 | 11,496 |

| 2018 | 8,335 |

| 2019 | 8,770 |

| 2020 | 2,291 |

| 2021 | 1,534 |

| 2022 | 0 |

| 2023 | 2,050 |

| 2024 | 3,916 |

The recently published “Start of Season Report” for Glasgow Airport shows the following for Donegal flights;

- Loganair will operate 168 movements (84 round trips), an increase of 26 compared to Summer 2024.

- The number of seats offered will also increase from 6,816 to 8,072, representing an increase of 18%

Dublin

Traffic between Scotland and Dublin appears to have recovered to pre-pandemic levels, however, as I mentioned at the beginning of this post, Aer Lingus primarily operate their flights as feeder flights to their US network out of Dublin, as a result, for a significant chunk of Scotland-Dublin passengers, their final destination is not even in Ireland.

The Dublin Airport passenger cap also impacted passenger numbers on these routes, as airlines were forced to change winter schedules to try and avoid breaching the cap, something that the airport and airlines want scrapped – but that is a separate post in itself!

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Aberdeen shows the following for Dublin flights;

- Aer Lingus will increase the number of movements they operate from 420 to 600 – that’s equivalent to increasing from 210 round trips to 300.

- The number of seats they will offer will also increase from 30,240 to 43,196 – an increase of 43%

- Loganair will increase the number of movements they operate from 394 to 678 – that means increasing from 197 to 339 round trips – a 72% increase.

- The number of seats offered will also increase from 28,092 to 46,976 – representing a 67% increase

When both airlines are combined, movements will increase from 814 to 1,278. Furthermore, seats available will increase from 58,332 to 90,172.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following for Dublin flights;

- Aer Lingus will increase the number of movements they operate from 2,574 to 3,034 – that’s equivalent to increasing from 1,287 round trips to 1,517.

- The number of seats they will offer will also increase from 228,168 to 264,880 – an increase of 16%

- Ryanair will increase the number of movements they operate from 1,674 to 1,834 – that’s equivalent to increasing from 837 round trips to 917.

- The number of seats they will offer will also increase from 318,642 to 347,586 – an increase of 9%

- Ryanair UK will not operate any flights in Summer 2025, they operate 104 movements in Summer 2024.

- As a result, this means the 19,656 seats provided by Ryanair UK are not available this summer.

When both airlines are combined, movements will increase from 4,248 to 4,868. Furthermore, seats available will increase from 566,466 to 612,466.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following with regards to Dublin flights;

- Aer Lingus will increase the number of movements they operate from 1,762 to 2,244 – that’s equivalent to increasing from 881 round trips to 1,122.

- The number of seats they will offer will also increase from 126,864 to 161,568 – an increase of 27%

- Ryanair will increase the number of movements they operate from 1,302 to 1,320 – that’s equivalent to increasing from 651 round trips to 660.

- The number of seats they will offer will also increase from 246,078 to 252,856 – an increase of 3%

When both airlines are combined, movements will increase from 372,942 to 414,421. Furthermore, seats available will increase from 566,466 to 612,466.

Knock

Knock has always been an exclusive route to Edinburgh Airport and is currently operated by Ryanair.

Passenger numbers since 2015 can be seen in the table below;

| Year | Passenger Numbers |

|---|---|

| 2015 | 0 |

| 2016 | 19,652 |

| 2017 | 25,360 |

| 2018 | 28,776 |

| 2019 | 27,227 |

| 2020 | 1,916 |

| 2021 | 6,292 |

| 2022 | 36,452 |

| 2023 | 43,868 |

| 2024 | 35,581 |

Similar to Cork, this route used to be operated by somebody else, in this case Flybe and is now operated by Ryanair.

Passenger numbers have recovered and exceeded 2019 levels, however, the route recorded a rather significant drop in passengers in 2024 as Ryanair reduced capacity on the route to deploy the aircraft elsewhere.

Looking ahead to Summer 2025, the recently published “Start of Season Report“ for Edinburgh Airport shows the following for Knock flights;

- Ryanair will continue to operate 120 movements (60 round trips) on the route, the same as Summer 2024.

- The number of seats on offer will increase by 1% from 23,032 to 23,160 suggesting a very small number of flights will be operated by the larger Boeing 737-8-200.

- Ryanair UK will also operate a very limited number of flights for the first time, operating 24 movements (12 round trips), they did not operate any in Summer 2024.

- These flights will offer 4,536 seats.

When both subsidiaries are combined, the Ryanair Group will operate 144 movements (72 round trips) and will offer 27,696 seats.

Shannon

Shannon is an exclusive route to Edinburgh Airport and is currently operated by Ryanair.

Passenger numbers since 2015 can be seen in the table below;

| Year | Passenger Numbers |

|---|---|

| 2015 | 1,107 |

| 2016 | 23,277 |

| 2017 | 28,839 |

| 2018 | 28,802 |

| 2019 | 29,187 |

| 2020 | 3,850 |

| 2021 | 5,721 |

| 2022 | 37,581 |

| 2023 | 58,867 |

| 2024 | 47,845 |

Similar to Cork and Knock, this route used to be operated by Aer Lingus and is now operated by Ryanair.

Passenger numbers have recovered and exceeded 2019 levels, however, the route recorded a rather significant drop in passengers in 2024 as Ryanair reduced capacity on the route to deploy the aircraft elsewhere.

It is notable at this point that despite the passenger cap constraining growth in Dublin, traffic has not shifted to regional airports across Ireland, supporting comments by Ryanair Group CEO Michael O’Leary that passengers want to go to Dublin, and that extra Cork, Shannon and Knock flights will not make a difference.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following for Knock flights;

- Ryanair will increase their movements from 162 to 308 – increasing from 81 round trips to 154.

- The number of seats on offer will increase by 84% from 31,914 to 58,740.

- Ryanair UK will also operate a very limited number of flights for the first time, operating 24 movements (12 round trips), they did not operate any in Summer 2024.

- These flights will offer 4,536 seats.

When both subsidiaries are combined, the Ryanair Group will increase from 162 movements to 332. The number of seas available will also increase from 31,914 to 63,276. However, these increases suggest the route is only returning to 2023 levels and that their is not much in terms of organic new growth.

My Final Thoughts

Overall, Ireland remains a significant inbound market to Scotland, but I do find myself wondering how 2025 will play out, primarily for Aer Lingus and Loganair.

With travel to America becoming less appealing to UK based travellers, and prices likely to rise for US based travellers it remains unclear if this will have any impact on Aer Lingus, yes the airline relies on connecting passengers, but changes to pricing patterns could allow them to pivot some capacity to UK-Ireland traffic without connections, especially from Glasgow and Edinburgh as some people will do anything to avoid flying Ryanair.

As for Loganair, their Aberdeen-Dublin route is expanding significantly, as is its competitor Aer Lingus, will this much of a capacity increase be absorbed by the market or is their now too much capacity to Aberdeen?

Looking at Glasgow Airport, this will be the first year since the pandemic that Cork and Donegal will operate all year, providing a good base line for pre and post pandemic comparisons.

Want to Find Out More about this brand, and how to contact us you can click here.

About The Author

George Nugent is an independent travel writer focused on honest reviews of rail, air, and coach journeys in the UK, Europe, and USA. Passionate about statistics and clear reporting, George shares insights to help travellers make informed choices.

One thought on “Market Overview: Scotland to Ireland”