Quick Note: Above each graph is a URL, you can ignore this! They only appear as the WordPress theme for this website has an issue with embedding content.

Last year I made a series of presentations about market share across Scotland to the ten largest inbound tourist markets as identified by Visit Scotland. Now that 2024 has concluded and we have a years worth of data I thought it would be a good idea to revisit each of these markets in a bit more detail.

A disclaimer is needed here, I have done this from an airport neutral point of view, and it is very important to remember that just because a load factor is high, that does not necessarily mean that yields are high.

This particular post is focusing specifically on the Scotland-Spain market, which is the fifth largest inbound tourism market for Scotland.

For those unfamiliar with the route networks and airlines below is a summary of the routes and airlines that operated flights in 2024;

- Aberdeen to Alicante with Ryanair

- Aberdeen to Malaga with Ryanair

- Aberdeen to Reus with TUI

- Aberdeen to Palma with TUI

- Aberdeen to Tenerife with TUI

- Edinburgh to Alicante with easyJet, Jet2 and Ryanair

- Edinburgh to Barcelona with Ryanair and Vueling

- Edinburgh to Fuerteventura with easyJet, Jet2 and Ryanair

- Edinburgh to Gran Canaria with easyJet, Jet2 and Ryanair

- Edinburgh to Ibiza with Jet2 and Ryanair

- Edinburgh to Lanzarote with easyJet, Jet2 and Ryanair

- Edinburgh to Madrid with easyJet, Iberia and Ryanair

- Edinburgh to Mahón with Jet2

- Edinburgh to Malaga with Jet2 and Ryanair

- Edinburgh to Palma with British Airways CityFlyer, easyJet, Jet2, TUI and Ryanair

- Edinburgh to Reus with Jet2

- Edinburgh to San Sebastian with British Airways CityFlyer

- Edinburgh to Santander with Ryanair

- Edinburgh to Seville with Ryanair

- Edinburgh to Tenerife with easyJet, Jet2 and Ryanair

- Edinburgh to Valencia with Ryanair

- Glasgow to Alicante with easyJet, Jet2, Ryanair and TUI

- Glasgow to Barcelona with easyJet

- Glasgow to Fuerteventura with easyJet and Jet2

- Glasgow to Gran Canaria with easyJet, Jet2 and TUI

- Glasgow to Girona with Jet2

- Glasgow to Ibiza with Jet2 and TUI

- Glasgow to Lanzarote with easyJet, Jet2 and TUI

- Glasgow to Mahón with Jet2 and TUI

- Glasgow to Malaga with easyJet, Jet2, Ryanair and TUI

- Glasgow to Palma with easyJet, Jet2 and TUI

- Glasgow to Reus with Jet2 and TUI

- Glasgow to Tenerife with easyJet, Jet2 and TUI

- Inverness to Palma with TUI

- Prestwick to Alicante with Ryanair

- Prestwick to Barcelona with Ryanair

- Prestwick to Gran Canaria with Ryanair

- Prestwick to Lanzarote with Ryanair

- Prestwick to Malaga with Ryanair

- Prestwick to Murcia with Ryanair

- Prestwick to Palma with Ryanair

- Prestwick to Tenerife with Ryanair

This post is probably the most challenging of the ten in this series to write, the Spanish market is massive, especially for an airport like Prestwick where 80% of its routes are Spanish. To try and make this post as easy as possible to follow I will use the format in the contents table below;

- Passenger Numbers By Month

- Passenger Numbers By Year

- Market Share Per Airport

- Spanish Mainland

- Balearic Islands

- Canary Islands

- Previously Served Destinations

- Final Thoughts

Without wasting any more time, lets get started!

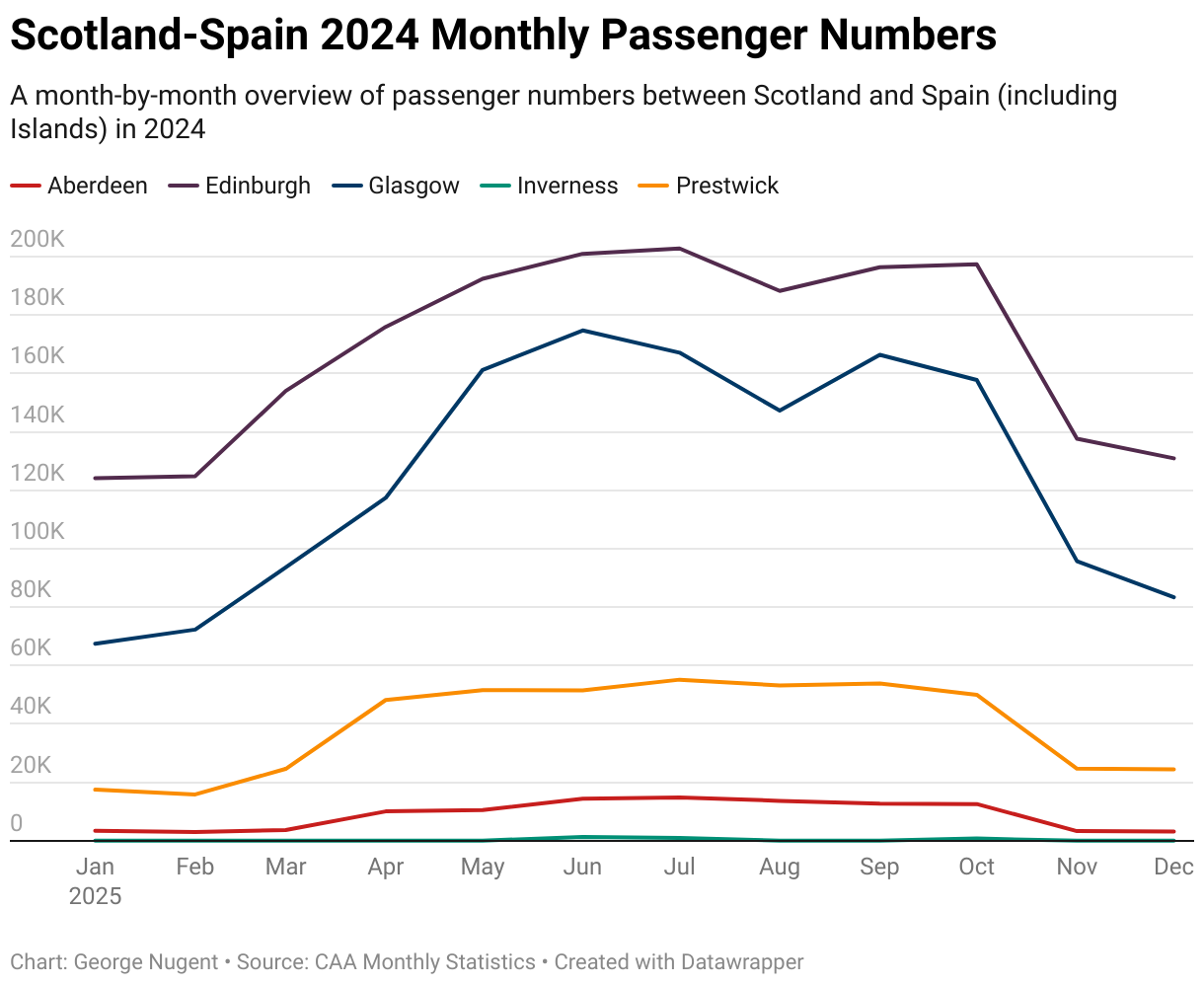

Passenger Numbers By Month

Passenger numbers between Scotland and Spain follow a trend that was easy to predict, stable passenger numbers in winter months with demand rising in the summer when the tourist season in the Balearic Islands comes online.

Later on in this post you will have the opportunity to see how passenger numbers in each segment of the Spanish market change month on month, with destinations across the Spanish Mainland and Islands having different tourist seasons throughout the year.

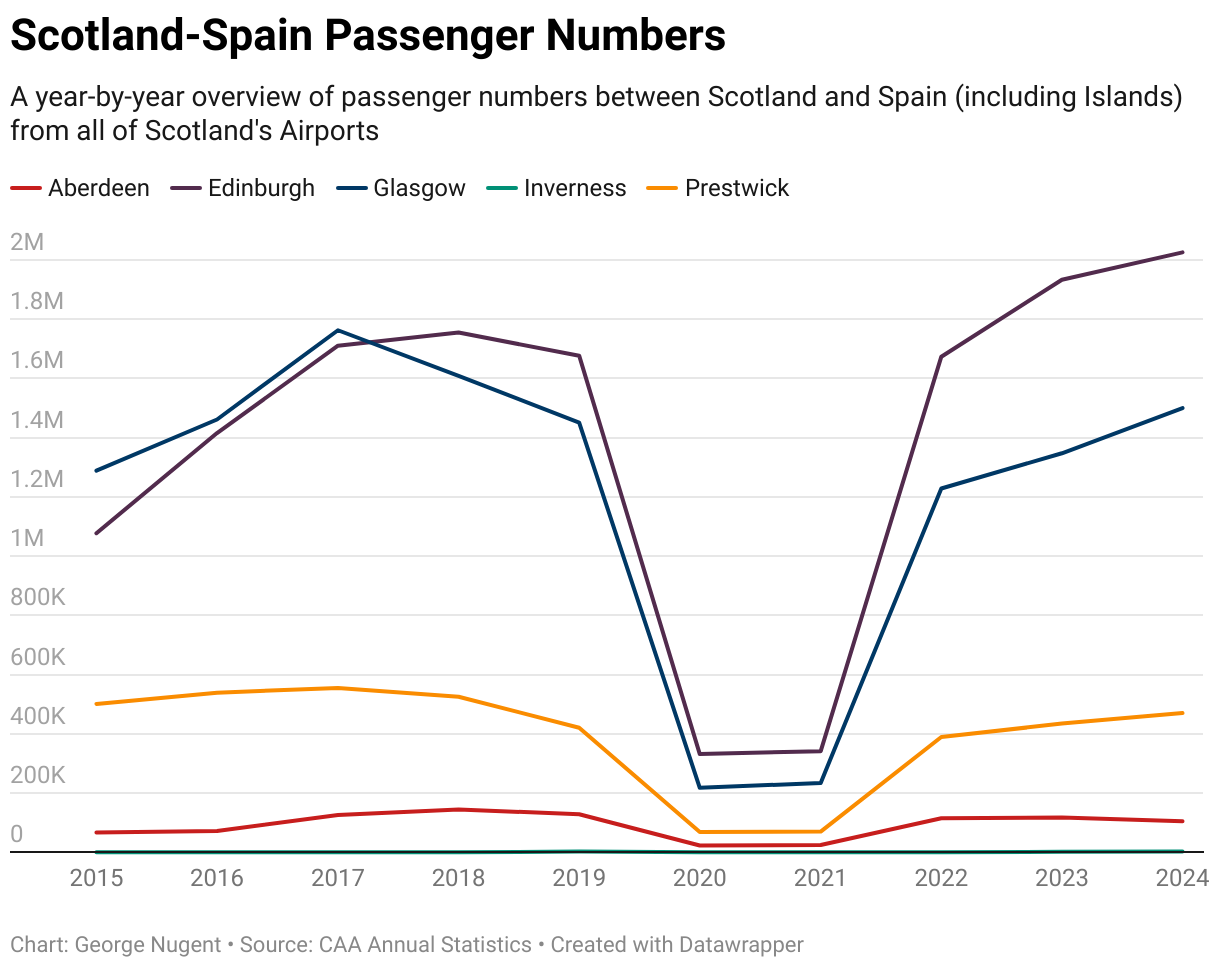

Passenger Numbers By Year

Passenger numbers between Scotland and Spain are above pre-pandemic levels as a whole, but, as I will show later on in this article, passengers appear to have changed where they are travelling to, partially as a result of some destinations no longer being offered from Scotland.

Overall, Edinburgh, Glasgow, Inverness and Prestwick have all recovered their 2019 traffic levels and exceeded them, with Aberdeen being the outlier still operating below 2019 levels.

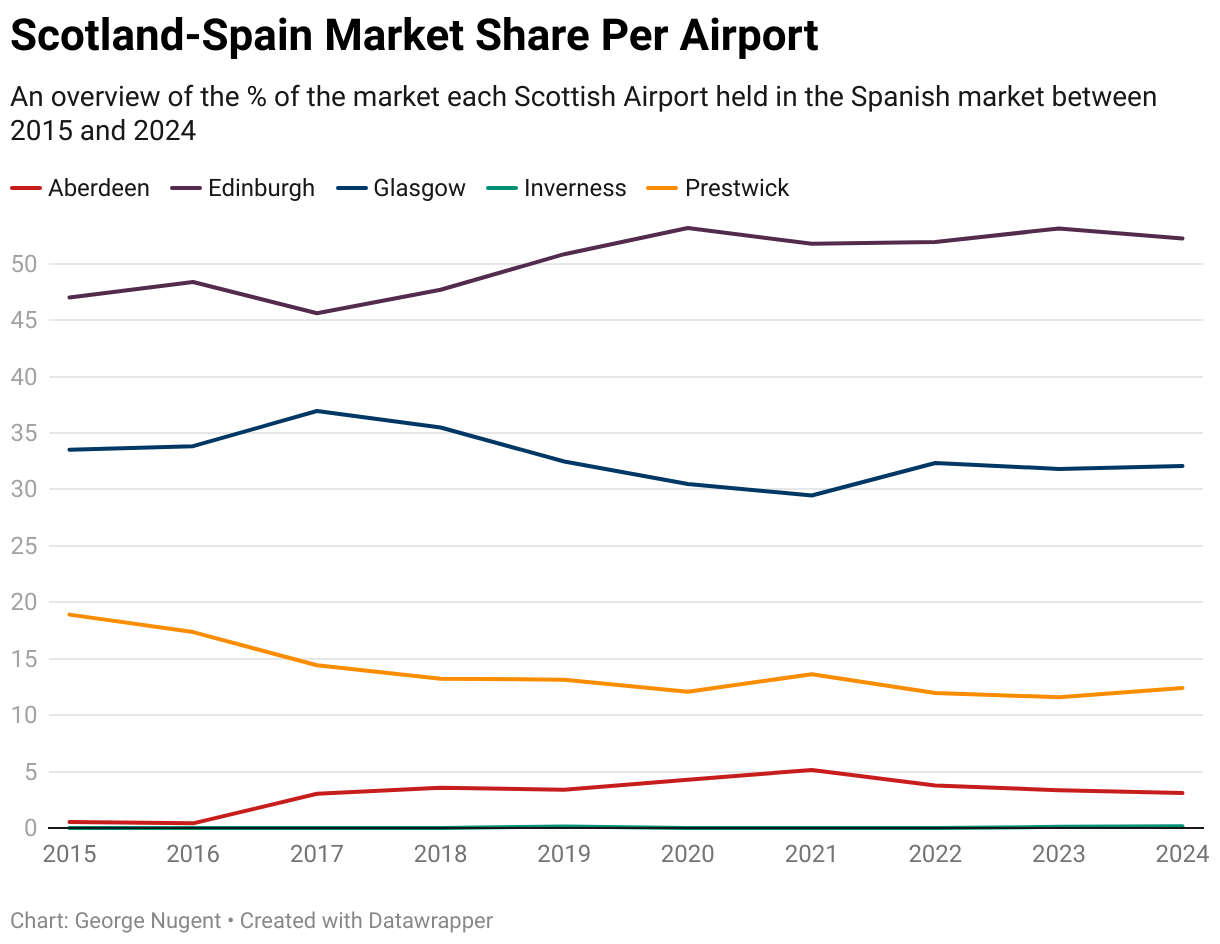

Market Share Per Airport

In recent years market share across Scotland’s Airports has remained relatively stable, with Edinburgh holding a slim majority of the market, and the Glasgow Airport’s also holding a respectable share.

Aberdeen market share has declined in recent years, but as I will explain further in this post, there is a reason for this, and there is also a reason to remain optimistic for summer 2025.

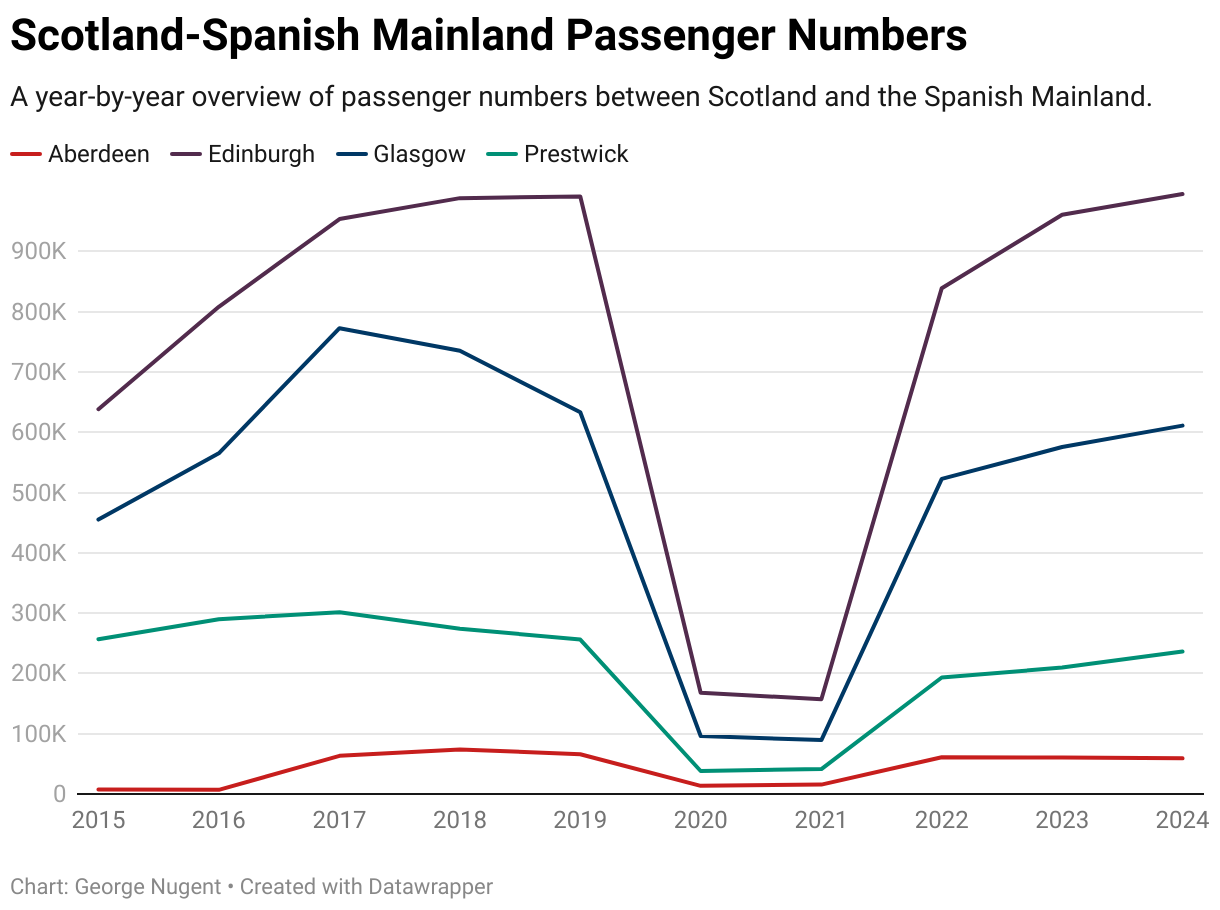

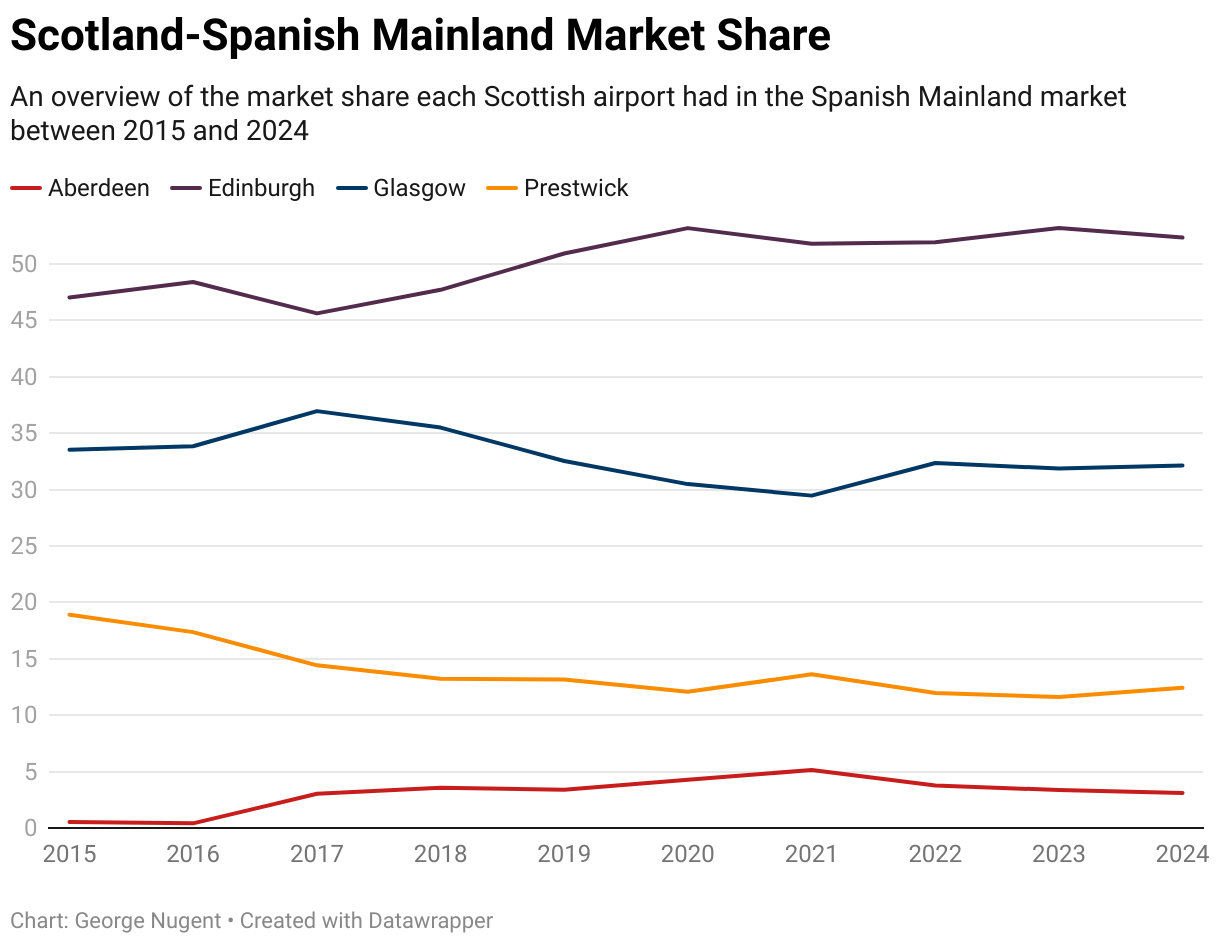

Spanish Mainland

All of the data in this section specifically relates to destinations located on the Spanish Mainland, all other data has been removed.

Passenger Numbers By Month

Passenger numbers from Scotland to the Spanish Mainland follow a trend that was to be predicted. Services operate throughout the year, however, Aberdeen is the only airport in Scotland to have a seasonal service.

Passenger numbers trend upwards significantly in the Summer as destinations such as Girona, Reus and Valencia only operate in the Summer season, alongside additional services to key destinations such as Alicante and Malaga.

Edinburgh consistently has the higher passenger numbers, however, it is stark to see how big the gap is in the winter months compared to the summer months.

Passenger Numbers By Year

Passenger numbers from Scotland as a whole are just below 2019 levels (1,946,210 passengers in 2019 vs 1,901,560 in 2024), however, Edinburgh Airport has slightly exceeded its 2019 passenger totals, all other airports remain below this level, however, I would not rule out Aberdeen, Glasgow and Prestwick also recovering to 2019 levels in 2025.

I should point out that Thomas Cook collapsed in September 2019, therefore, it is reasonable to assume that the actual passenger numbers for 2019 should have been higher than they were despite airlines best attempts to source additional capacity.

Furthermore, at the end of Summer 2018 Ryanair closed their Glasgow Airport base, resulting in the loss of two routes (Madrid, and Valencia) somewhat explaining the steep drop in passenger numbers between 2018 and 2019.

Market Share Per Airport

Compared to 2019, not much has changed, with all four airports remaining relatively stable, it is what was happening before 2019 that is much more interesting.

Between 2017 and 2019 market share at Glasgow Airport fell by 4.42%, partially as a result of the collapse of Thomas Cook and the loss of a Ryanair base as mentioned earlier, however, market share at Edinburgh Airport increased by 4.69%, one of the rare occasions where it appears that passengers directly transferred travel from one airport to the other.

Market share in Aberdeen (a very heavily outbound market) remains relatively consistent both pre and post pandemic.

Route Specific Numbers

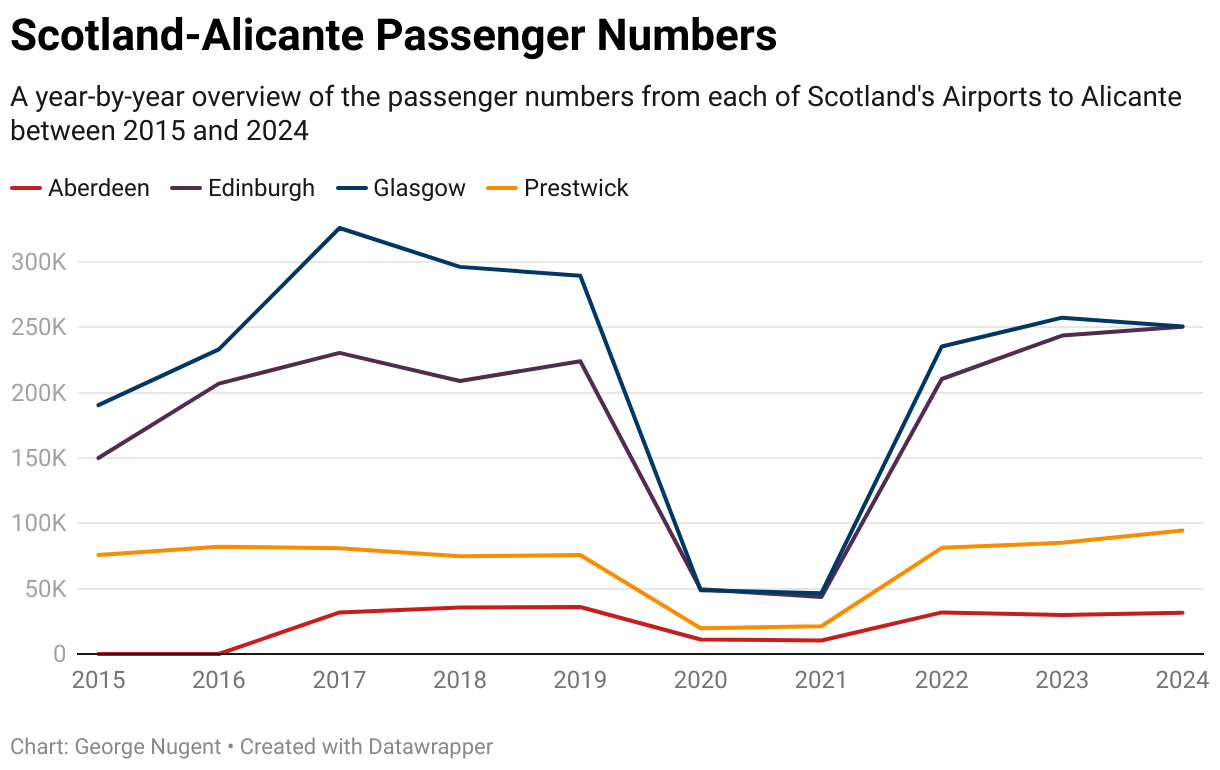

Alicante

In the Alicante market, Glasgow retains its position as the busiest airport in Scotland, just, however, given how close the gap is between both Glasgow and Edinburgh in 2024 something as simple as a flight cancellation could have changed this graph to show Edinburgh as the new market leader.

Passenger numbers at Prestwick Airport have also exceeded 2019 levels by 24.9%, seeing as Prestwick is the only one of the three central belt airports to not have been impacted by base closures or airline collapses, it is not unreasonable to use it as a barometer of demand between the Central Belt and Alicante.

Looking at Aberdeen it is worth noting that Ryanair converted their Alicante-Aberdeen route from year round operation to a summer seasonal operation, meaning no flights in Q1 of 2024, despite that, the airport still put in a solid performance on the route, only losing 4,300 passengers thanks to an increase in flights during the summer months.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Aberdeen Airport shows the following in terms of movements and seats;

- Movements will reduce from 180 to 162 – equating to a reduction of 10%

- This means reducing from 90 round trips to 81 round trips.

- Seats will reduce from 35,460 to 31,914 – also equating to a reduction of 10%

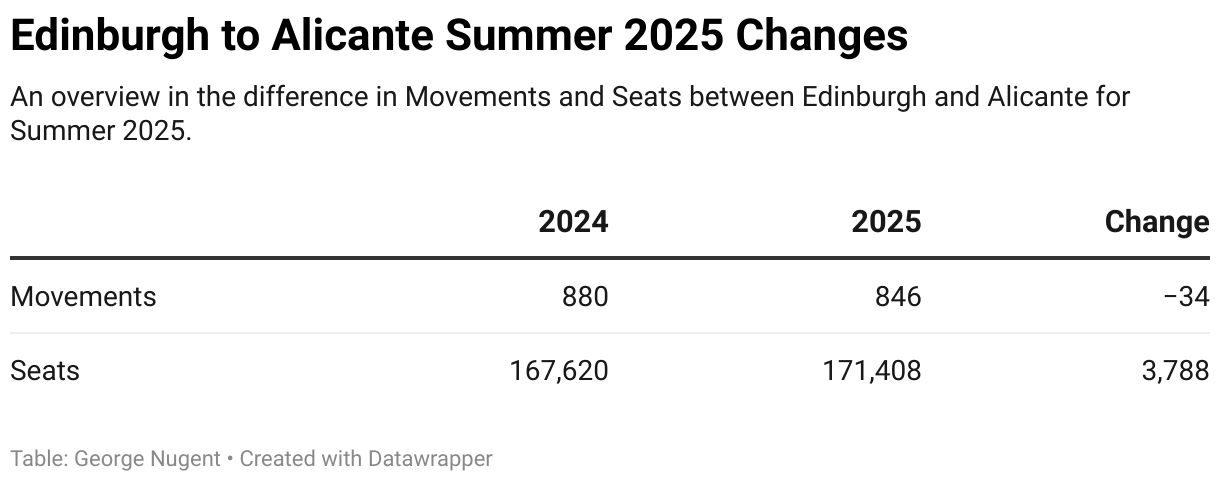

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

easyJet UK

- Movements will remain the same at 180 – the same as 2024.

- The number of seats will remain the same at 33,480

Jet2

- Movements will reduce from 308 to 288 – equating to a reduction of 6%

- This means reducing from 154 to 144 round trips

- The number of seats available will increase from 58,212 to 63,462 – equating to an increase of 9%

- Jet2 will use the larger A321 on a number of Alicante flights, allowing less flights but more seats

Ryanair (FR)

- Movements will increase from 272 to 378 – equating to an increase of 39%

- This means increasing from 136 to 189 round trips.

- The number of seats available will increase from 53,248 to 74,466 – equating to an increase of 40%

Ryanair UK

- Movements will reduce from 120 to 0 – equating to a reduction of 100%

- This means reducing from 60 round trips to 0.

- The number of seats available will reduce from 22,680 to 0

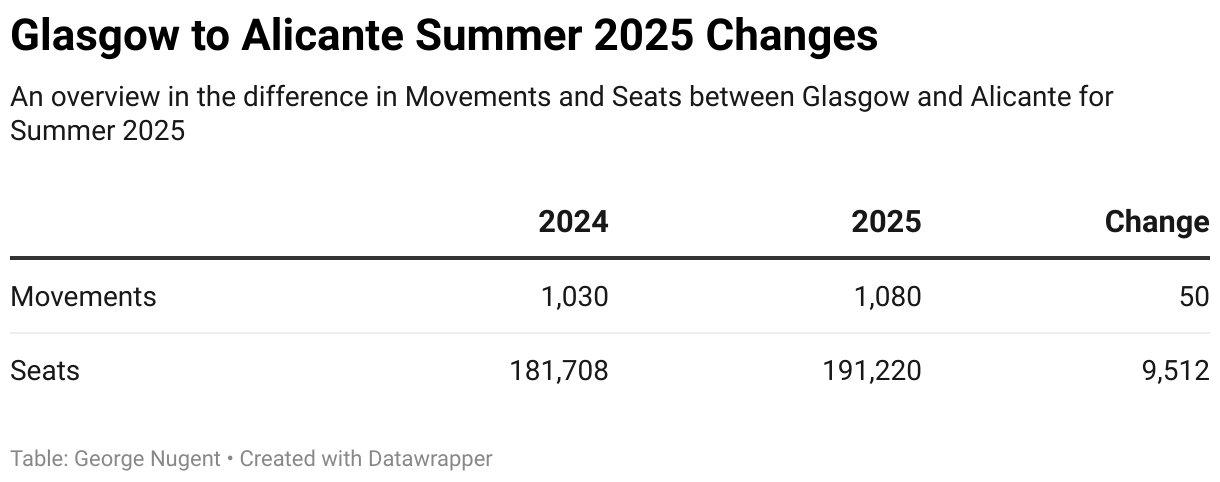

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

easyJet Europe

- Movements will increase from 402 to 420 – equating to an increase of 4%

- This means increasing from 201 to 210 round trips

- The number of seats available will also increase from 62,712 to 65,520

Jet2.com

- Movements will increase from 388 to 420 – equating to a rise of 8%

- This means increasing from 194 to 210 round trips

- The number of seats available will increase by 8% from 73,332 to 79,380

Ryanair

- Movements will remain the same at 120 – equating to 60 round trips

- The number of seats available will rise by 3% from 22,984 to 23,640

TUI

- Movements will remain the same at 120 – equating to 60 round trips

- The number of seats available will remain the same at 22,680

Moving to Prestwick Airport, no Start of Season Report is published, however, Ryanair will continue to operate a daily service from the airport, and has also upgraded a number of flights to the larger Boeing 737-8-200 series of aircraft with 197 seats.

As a result, passenger numbers on the route should increase when compared to Summer 2024.

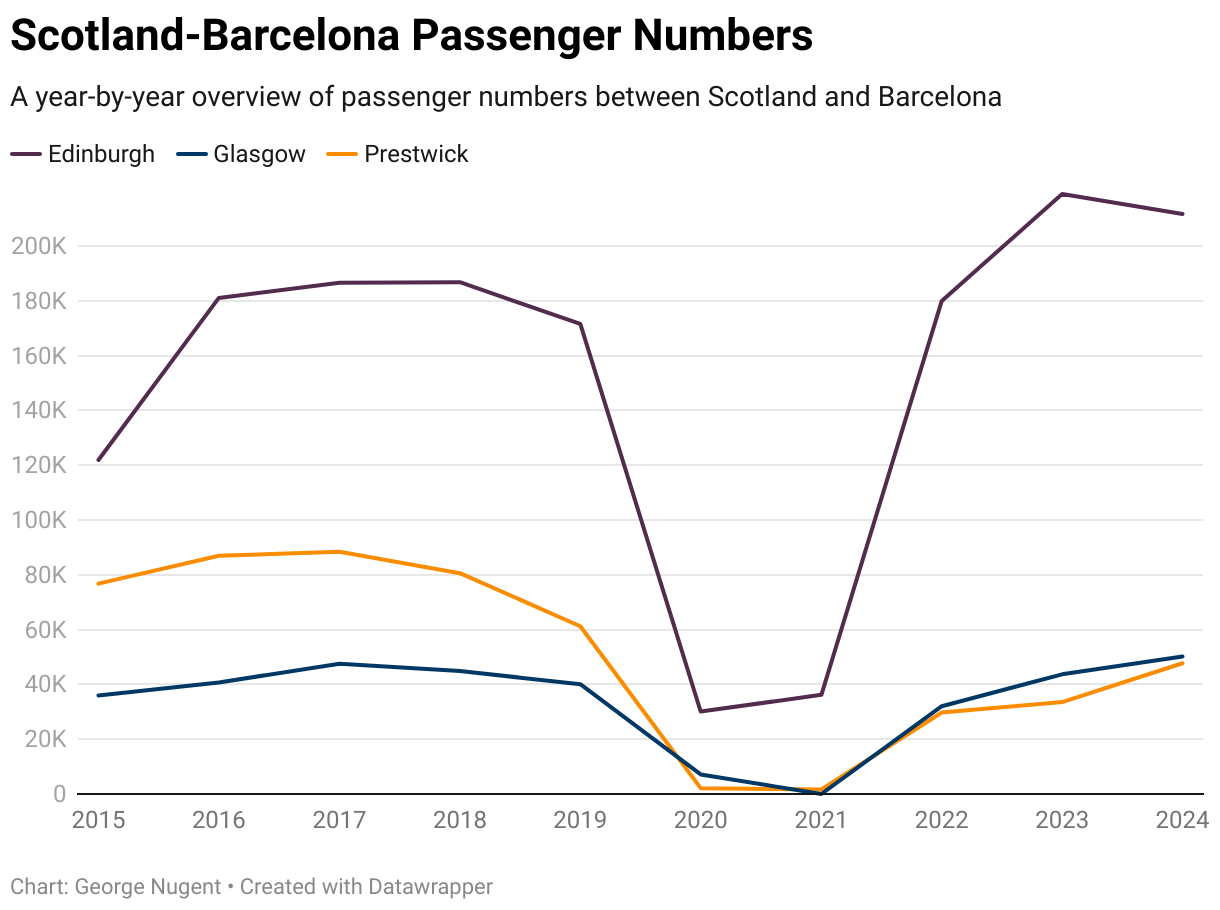

Barcelona

Unlike Alicante, there is a clear market leader when it comes to the Barcelona market. Edinburgh Airport remains the largest airport in Scotland when it comes to Barcelona flights, partially because of the airlines who serve the route.

Ryanair is very well known in Spain and caters to both Spanish and UK travellers, allowing for a healthy mix of two way traffic on the route. Vueling also operates Edinburgh flights and is one of the largest Spanish based carriers, the airline also offers connecting flights through Barcelona to smaller regional destinations such as Asturias and Vigo where Ryanair is retreating from.

Compare this to easyJet who operate flights from Glasgow who are much less known in Spain for UK flights, with passengers on flights from Glasgow to Barcelona more likely to be UK originating it can make overall demand for the route lower, especially as Ryanair operates into Prestwick to the South West and Edinburgh to the East. I should also point out that before 2020, the Glasgow to Barcelona route was operated by Jet2 and not easyJet, the former of whom would be almost exclusively UK originating passengers.

Interestingly, passenger numbers declined on the Edinburgh route in 2024, largely due to Vueling making the decision to reduce the route to Summer Seasonal apart from a brief Christmas programme of flights, whereas both easyJet and Ryanair expanded their operations from Glasgow during the winter months.

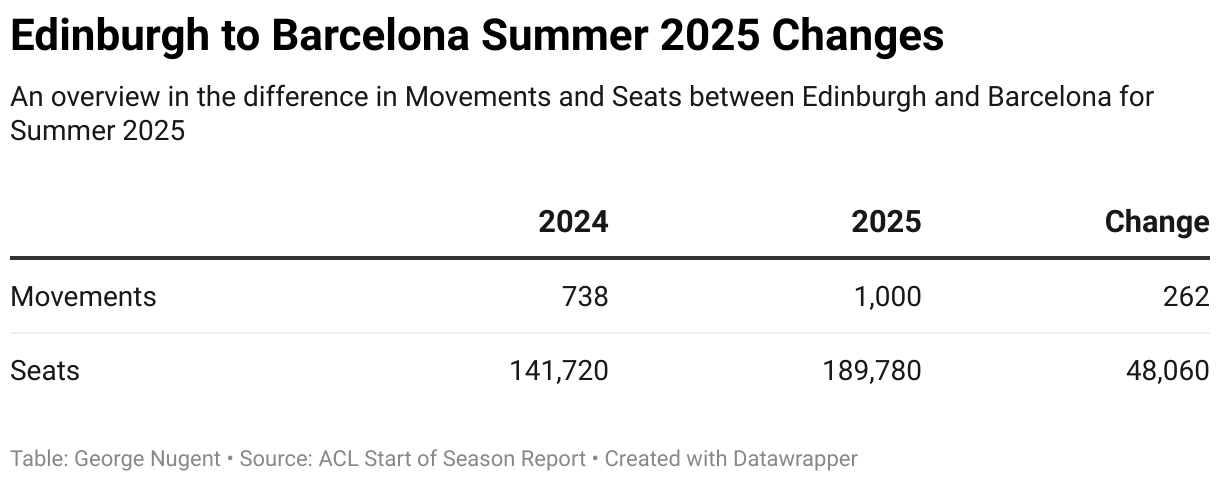

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Ryanair (FR)

- Movements will increase from 624 to 660 – equating to an increase of 6%

- The number of seats will increase from 121,200 to 128,580.

Vueling

- Movements will increase from 114 to 340 – equating to an increase of 198%

- This means increasing from 57 to 170 round trips.

- The number of seats available will increase from 20,520 to 61,200 – equating to an increase of 198%

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

- Movements will decrease from 236 to 234 – equating to a decrease of 1%

- This means reducing from 168 to 167 round trips

- The number of seats available will decrease from 41,556 to 39,924 – equating to a decrease of 4%

- The fact seats are down more than movements suggests easyJet is using more Airbus A319 aircraft on the route rather than A320’s

Moving to Prestwick Airport, no Start of Season Report is published, however, Ryanair will continue to operate 4 flights per week from the airport, and has also upgraded a number of flights to the larger Boeing 737-8-200 series of aircraft with 197 seats.

As a result, passenger numbers on the route should increase when compared to Summer 2024.

It should be noted however that Ryanair did plan to operate 5 weekly flights on this route, which would have taken it back to it’s 2019 levels of service, the airline has since removed this planned increase.

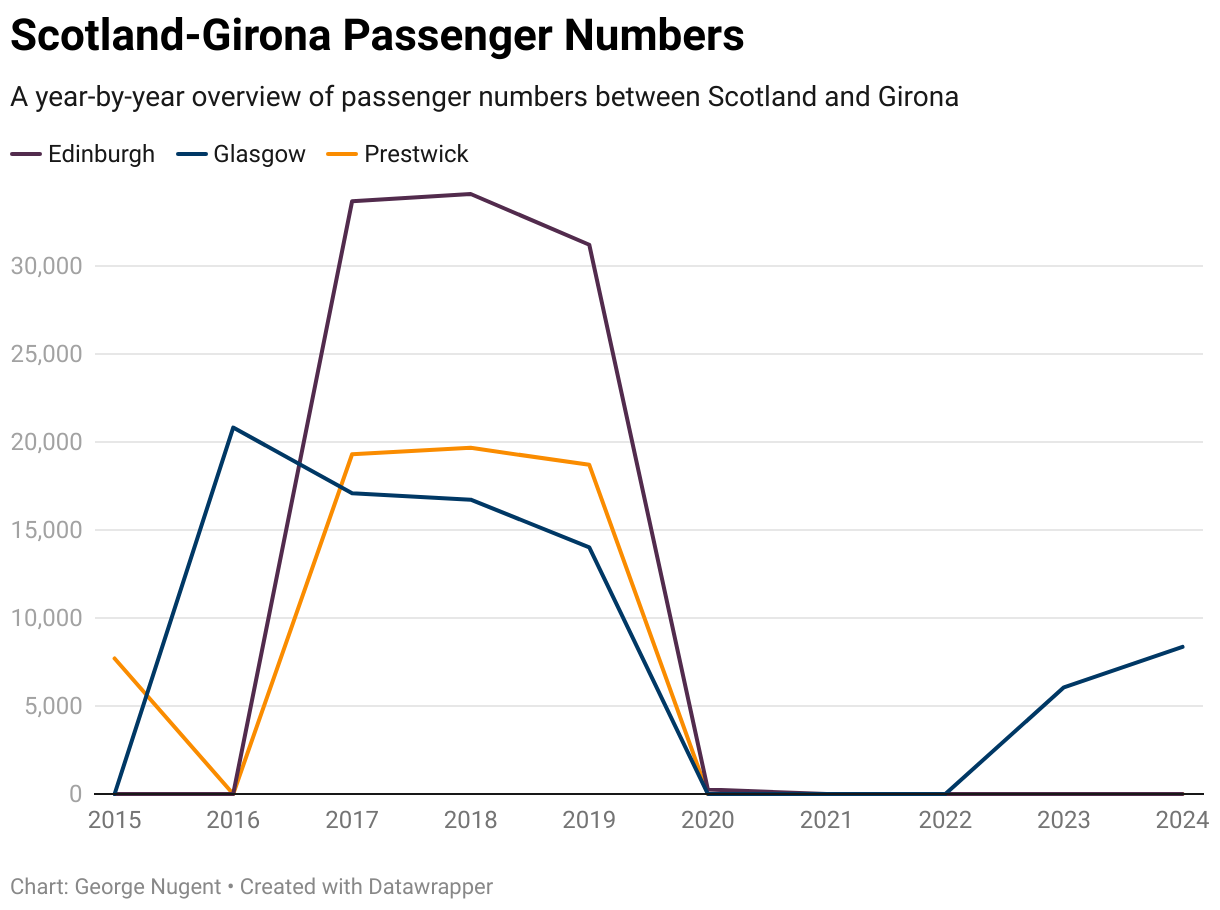

Girona

Outside of destinations that are no longer served, Girona holds the rather unfortunate title of being the slowest destination to recover across the entirety of Spain – for context passenger numbers are only operating at 13.07% of 2019 levels, with the number of airports seeing service having reduced by 66%.

Glasgow Airport is currently the only Scottish Airport with flights to Girona, however, from May 2026, Edinburgh will also regain flights, however, these flights will only reintroduce approximately 25% of the available capacity compared to 2019 from the airport.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

- Movements will remain the same at 50.

- This means 25 round trips will operate

- The number of seats available will remain the same at 9,450

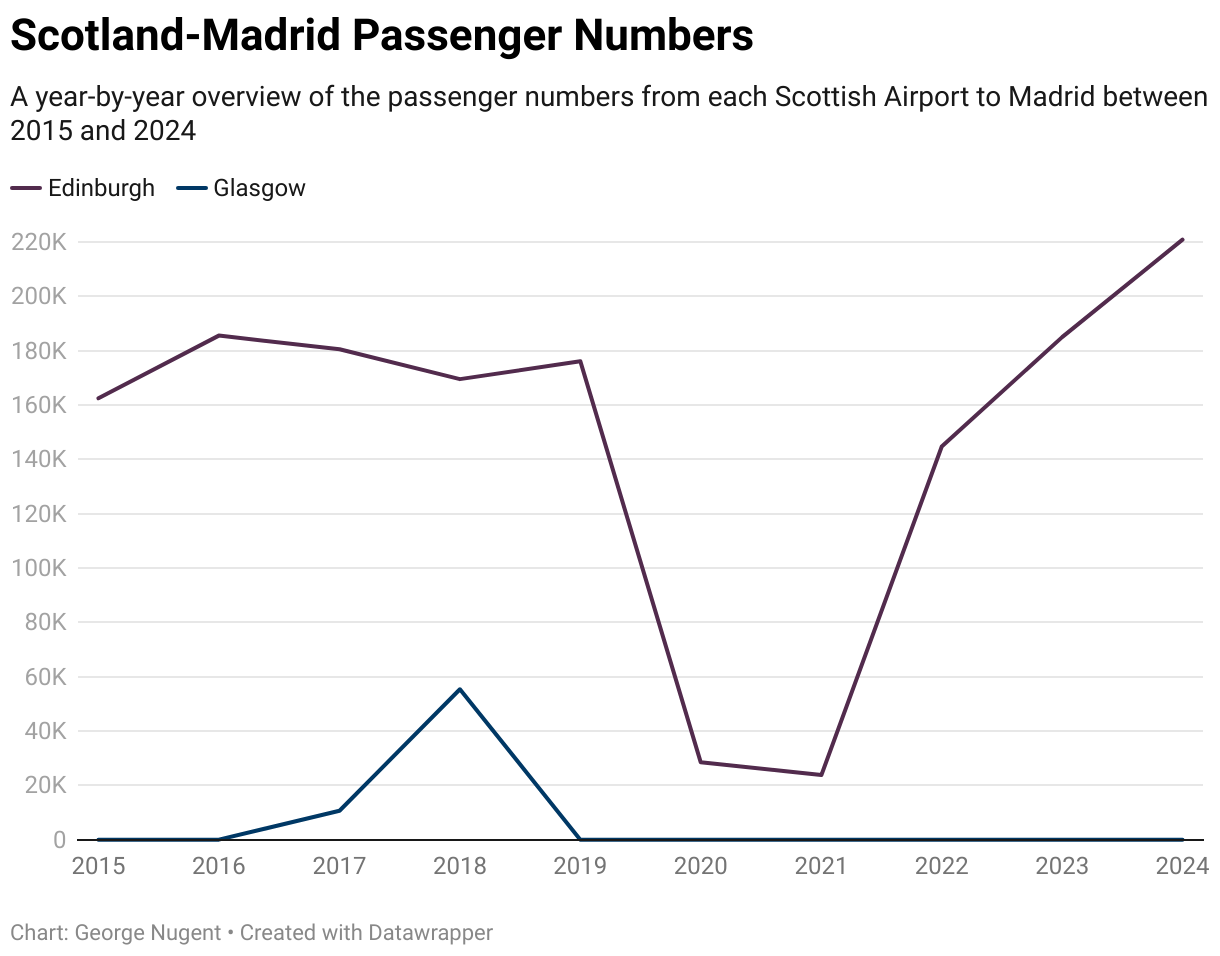

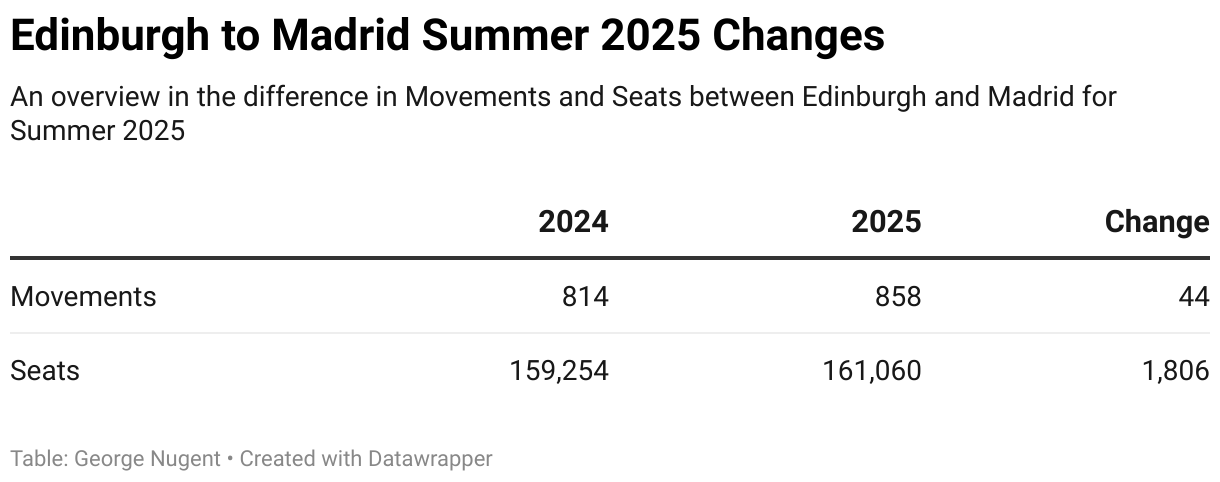

Madrid

Madrid was one of the two airports in Spain that consolidated operations at Edinburgh Airport following the decision by Ryanair to close their Glasgow base in October 2018, yet despite that, passenger numbers at Edinburgh did not rise as some may have expected.

The rapid recovery post pandemic has been helped by the blend of airlines operating the route, with easyJet catering to the UK based market, Ryanair catering to both the Spanish and UK point to point traffic, and Iberia catering to the Spanish market as well as connecting traffic through their Madrid hub.

Traffic to Madrid is operating at 125.4% of 2019 levels, and as things stand just now, Edinburgh will remain the only Scottish Airport with flights to Madrid in 2025.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

easyJet UK

- Movements will increase from 420 to 460 – equating to an increase of 10%

- The equivalent of increasing from 210 to 230 round trips

- The number of seats available will also increase from 78,120 to 85,560

Iberia Express (I2)

- Movements will increase from 180 to 218 – equating to an increase of 21%

- The equivalent of increasing from 90 to 109 round trips

- Seats will increase from 39,600 to 41,000 – equating to an increase of 4%

- The fact the seats increase is significantly lower than movements suggests that Iberia Express will use smaller aircraft on a number of flights.

Ryanair (FR)

- Movements will reduce from 214 to 180 – equating to a decrease of 16%

- The equivalent of decreasing from 107 to 90 round trips

- Seats will decrease from 41,534 to 34,500 – equating to a decrease of 17%

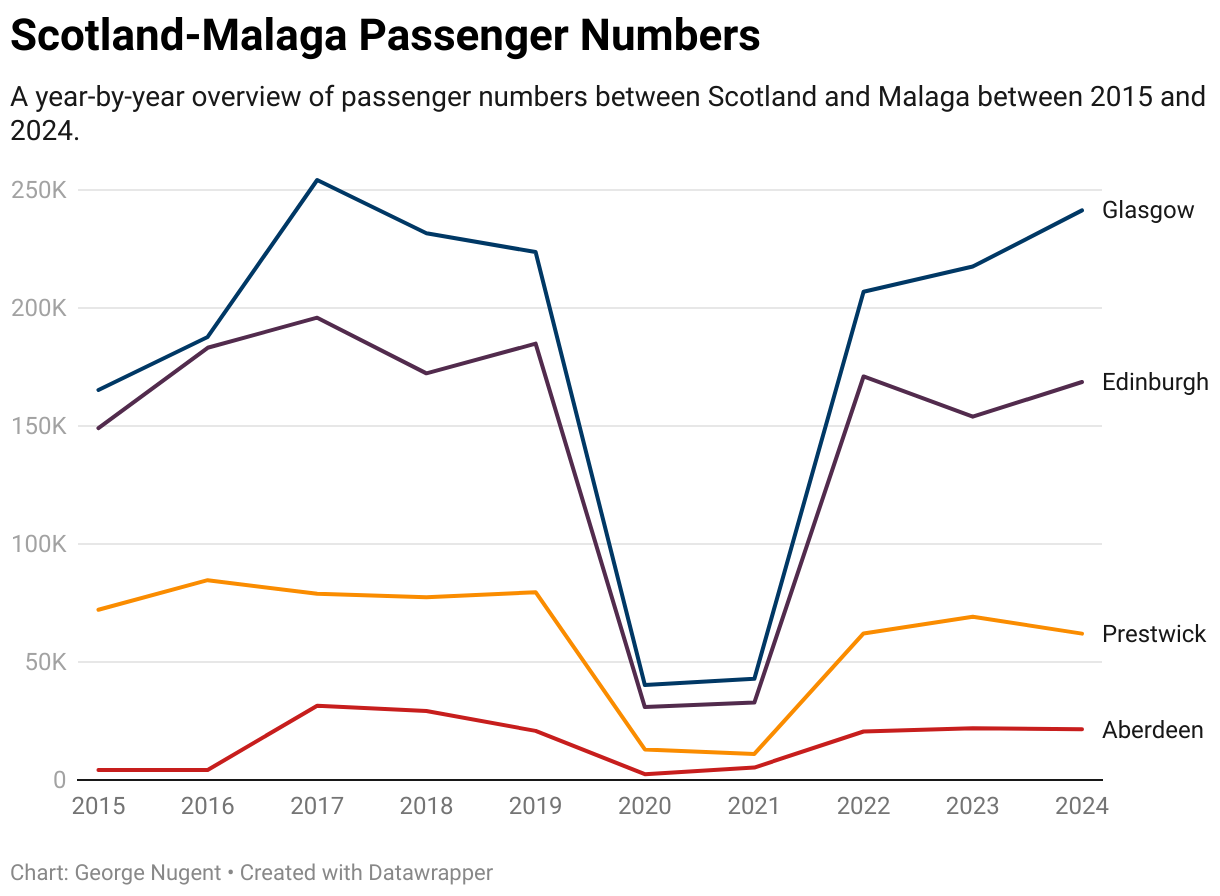

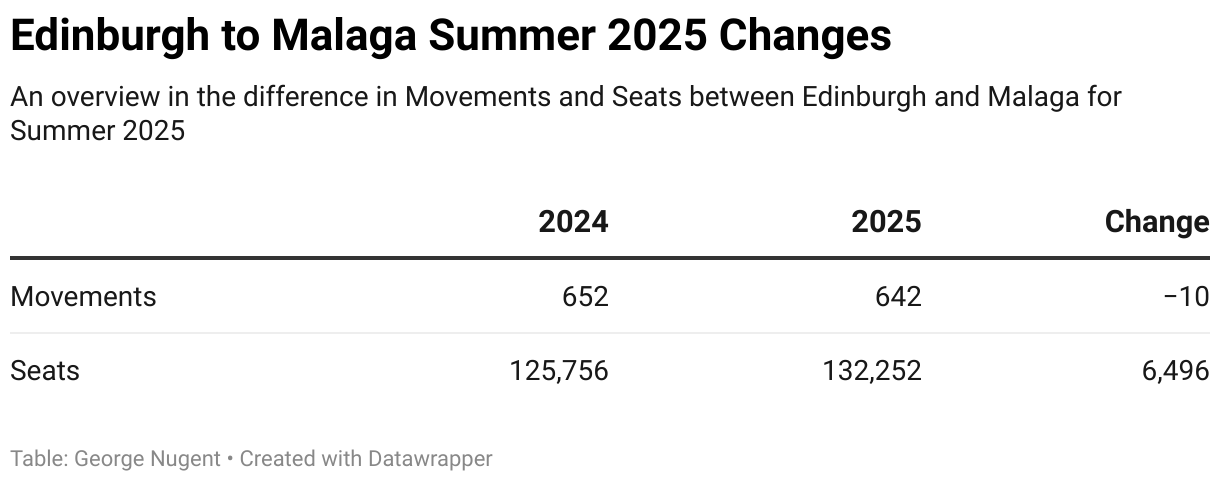

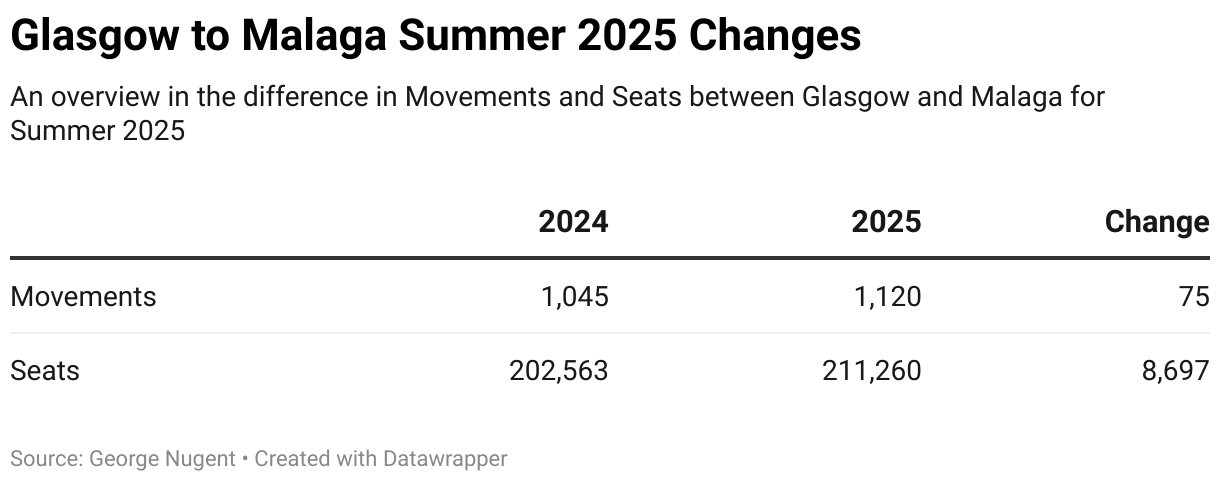

Malaga

Malaga presents something unique when it comes to pre and post pandemic recovery, it is one of only a handful of destinations where both Aberdeen and Glasgow have exceeded 2019 levels, and Edinburgh and Prestwick have not.

Taking a holistic view of the Malaga market, passenger numbers are operating at 97% of their 2019 levels, with the recovery rate for each airport below;

- Aberdeen = 103.5%

- Edinburgh = 91.2%

- Glasgow = 107.9%

- Prestwick = 77.9%

Malaga remains the second largest destination on the Spanish Mainland in terms of passenger numbers, behind Alicante, but it is interesting to see the market more split across Scotland’s Airports compared to Alicante, after all, the gap for ALC is less than 200 people.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Aberdeen Airport shows the following in terms of movements and seats;

- Movements will increase from 120 to 180 – equating to a increase of 50%

- This means increasing from 60 round trips to 90 round trips.

- Seats will increase from 23,224 to 35,460 – also equating to a increase of 50%

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Jet2

- Movements will reduce from 284 to 240 – equating to a reduction of 15%

- This means reducing from 142 to 120 round trips

- The number of seats available will increase slightly from 53,676 to 53,874 – equating to an increase of less than 1%

- Jet2 will use the larger A321 on a number of Malaga flights, allowing less flights but more seats

Ryanair (FR)

- Movements will reduce from 368 to 342 – equating to a decrease of 7%

- This means increasing from 184 to 171 round trips.

- The number of seats available will reduce from 72,080 to 67,038 – equating to an increase of 40%

Ryanair UK

- Movements will increase from 0 to 60 – a new service for Summer 2025.

- This means that 30 round trips will operate

- The number of seats will increase from 0 to 11,340.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

easyJet Europe

- Movements will increase from 0 to 18 – a new service for Summer 2025

- The number of seats available will increase from 0 to 3,348

easyJet UK

- Movements will reduce from 206 to 204 – equivalent to a decrease of 1%

- This means reducing from 103 to 102 round trips

- The number of seats available will reduce from 75,276 to 74,172 – equivalent to a decrease of 1%

Jet2

- Movements will increase from 340 to 348 – equivalent to an increase of 2%

- This means increasing from 170 to 174 round trips

- The number of seats available will increase from 64,260 to 65,772 – equivalent to an increase of 2%

Ryanair (FR)

- Movements will remain the same at 240 – the same as Summer 2024

- This means 120 round trips will operate

- Seats available will increase from 46,576 to 46,800 – equivalent to an increase of less than 1%

TUI

- Movements will increase from 59 to 112 – equivalent to an increase of 90%

- This means increasing from 29.5 to 56 round trips

- TUI is moving one of its weekly flights from British Airways CityFlyer to their own aircraft, as a result BA will reduce from 50 to 0 movements.

- This means increasing from 29.5 to 56 round trips

- The number of seats available will increase from 11,151 to 21,168 – equivalent to an increase of 90%

- TUI is moving one of its weekly flights from British Airways CityFlyer to their own aircraft, as a result BA will reduce from 5,300 to 0

Moving to Prestwick Airport, no Start of Season Report is published, however, Ryanair will increase from 5 to 6 weekly from the airport, and has also upgraded a number of flights to the larger Boeing 737-8-200 series of aircraft with 197 seats.

As a result, passenger numbers on the route should increase when compared to Summer 2024.

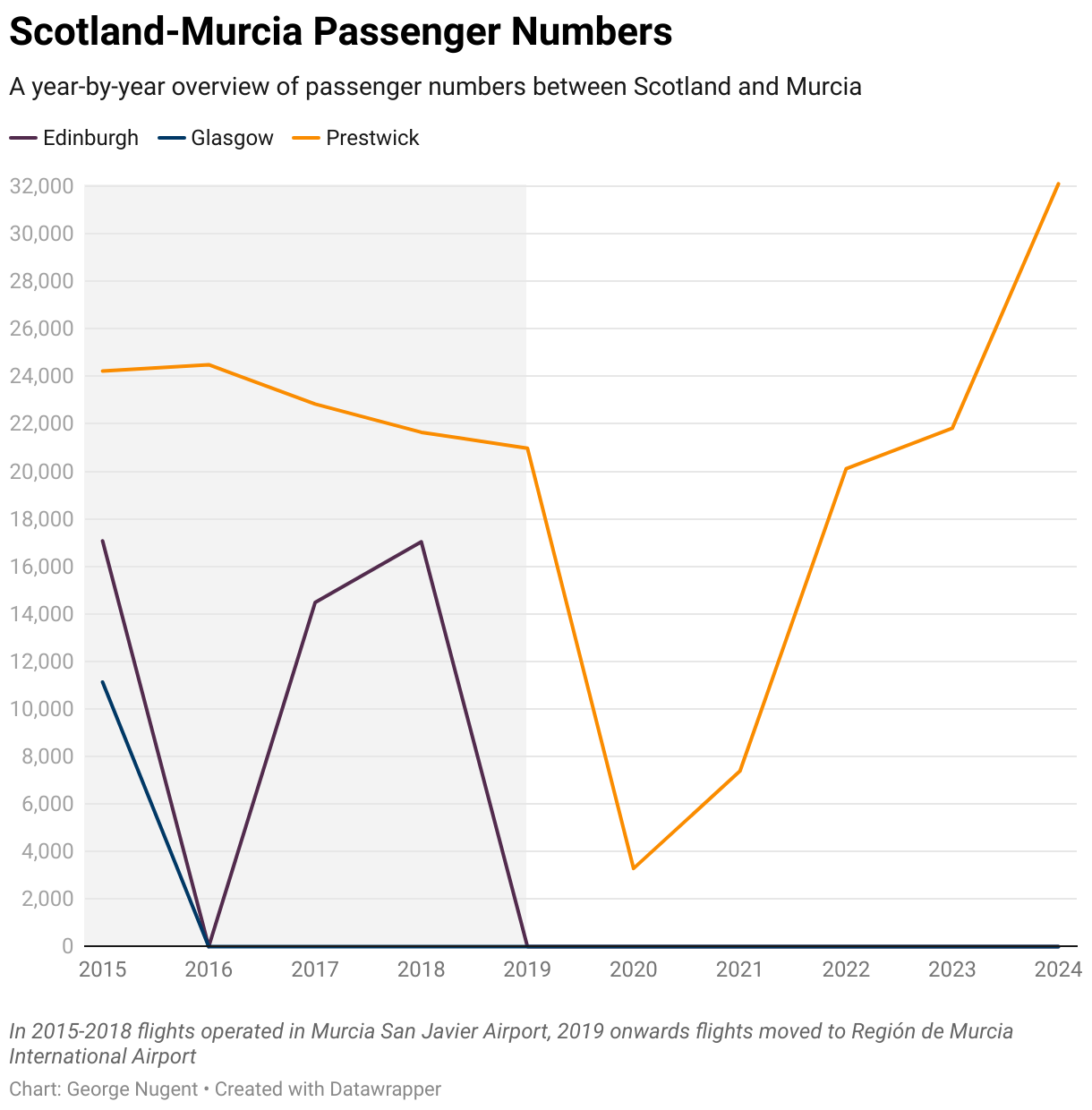

Murcia

Murcia is unique in Scottish aviation, as it is the only route to be served from Prestwick alone – with no other airport in Scotland having flights to Murcia!

Despite this, passenger numbers at Prestwick quickly recovered from the pandemic, and as of the end of 2024, are operating 153% above 2019 levels.

Looking ahead to Summer 2025, Ryanair has significantly expanded its Prestwick-Murcia route, increasing from 3 to 5 weekly, and will also operate all flights on the larger Boeing 737-8-200, increasing capacity on each flight by 8 seats.

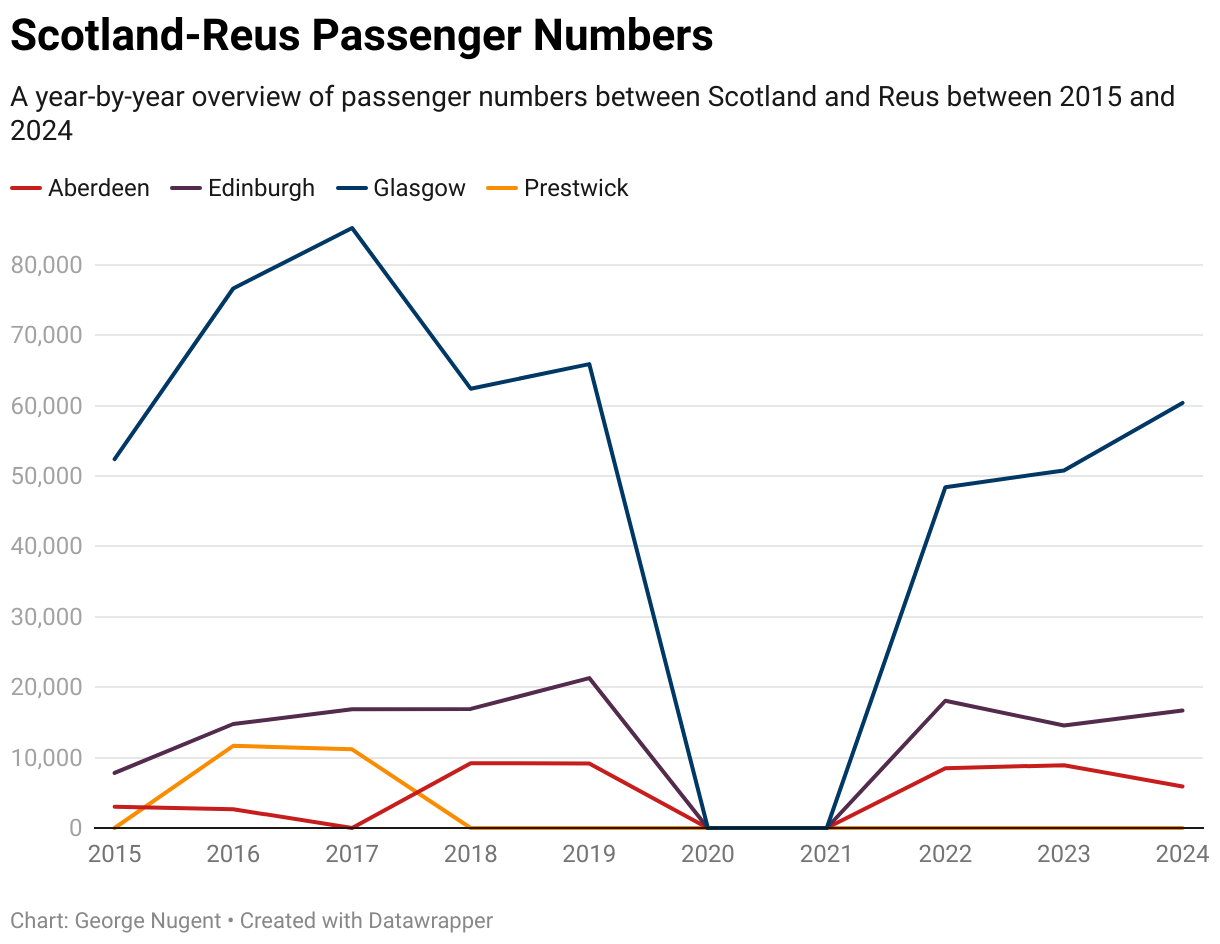

Reus

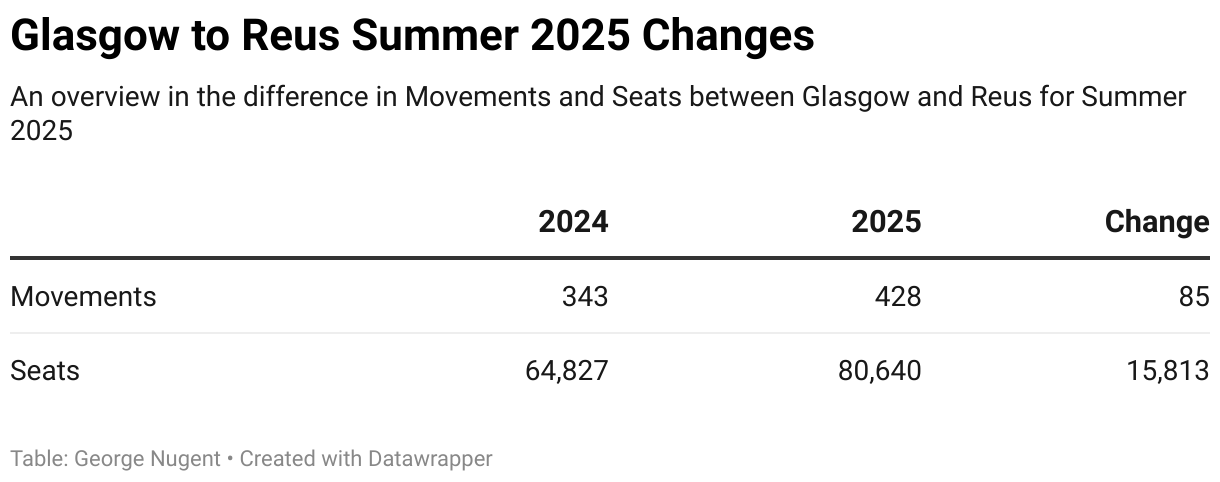

Reus passenger numbers continue to recover from the impact of the pandemic and the collapse of Thomas Cook, however, the recovery is not even across the country, with Aberdeen passenger numbers on the decline – partly due to the closure of TUI’s single aircraft base in Aberdeen. As a result of this base closure, Aberdeen flights now have to be worked around Glasgow flights.

Passenger numbers to Reus are currently operating at 86.1% of 2019 levels, with no airport having recovered passenger numbers to pre 2019 levels, however, both Edinburgh and Glasgow should exceed 2019 levels, however, Edinburgh will be borderline recovery, whereas Glasgow should significantly exceed 2019 levels.

The recovery rates for each airport is available below;

- Aberdeen = 64.4%

- Edinburgh = 78.4%

- Glasgow = 91.6%.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Aberdeen Airport shows the following in terms of movements and seats;

TUI

- Movements will increase from 35 to 36 – equating to a increase of 3%

- This means increasing from 17.5 round trips to 18 round trips.

- Seats will increase from 6,615 to 6,804 – also equating to a increase of 3%

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Jet2

- Movements will increase from 98 to 119 – equating to an increase of 21%

- This means increasing from 49 round trips to 59.5 round trips.

- Seats will increase from 18,522 to 25,415 – also equating to a increase of 37%

- As the % increase for seats is higher than movements it suggests that Jet2 will use the larger Airbus A321 on a number of flights.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

easyJet UK

- Movements will increase from 0 to 84 round trips – a new service for Summer 2025

- This means increasing from 0 to 42 round trips

- The number of seats available will increase from 0 to 15,624

Jet2

- Movements will increase from 158 to 163 – equating to an increase of 3%

- This means increasing from 79 to 81.5 round trips

- The number of seats will increase from 29,862 to 30,807 – also equating to an increase of 3%

TUI

- Movements will reduce from 185 to 181 – equating to a decrease of 2%

- This means reducing from 92.5 to 90.5 round trips

- The number of seats will decrease from 34,965 to 34,209 – also equating to a decrease of 2%

San Sebastian

San Sebastian is the newest Spanish destination added to the Scottish portfolio thanks to a Summer seasonal service from Edinburgh operated by British Airways CityFlyer, with services starting in 2024.

In 2024, passenger numbers on the route were 3,084, thus setting this as the benchmark target for Summer 2025.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

British Airways CityFlyer

- Movements will remain the same as Summer 2024 at 40

- This means 20 round trips will operate

- Seats will also increase slightly from 4,176 to 4,240 – equating to an increase of 2%.

- BACF will operate some of their higher density E190 aircraft on the route, allowing for a slight capacity improvement.

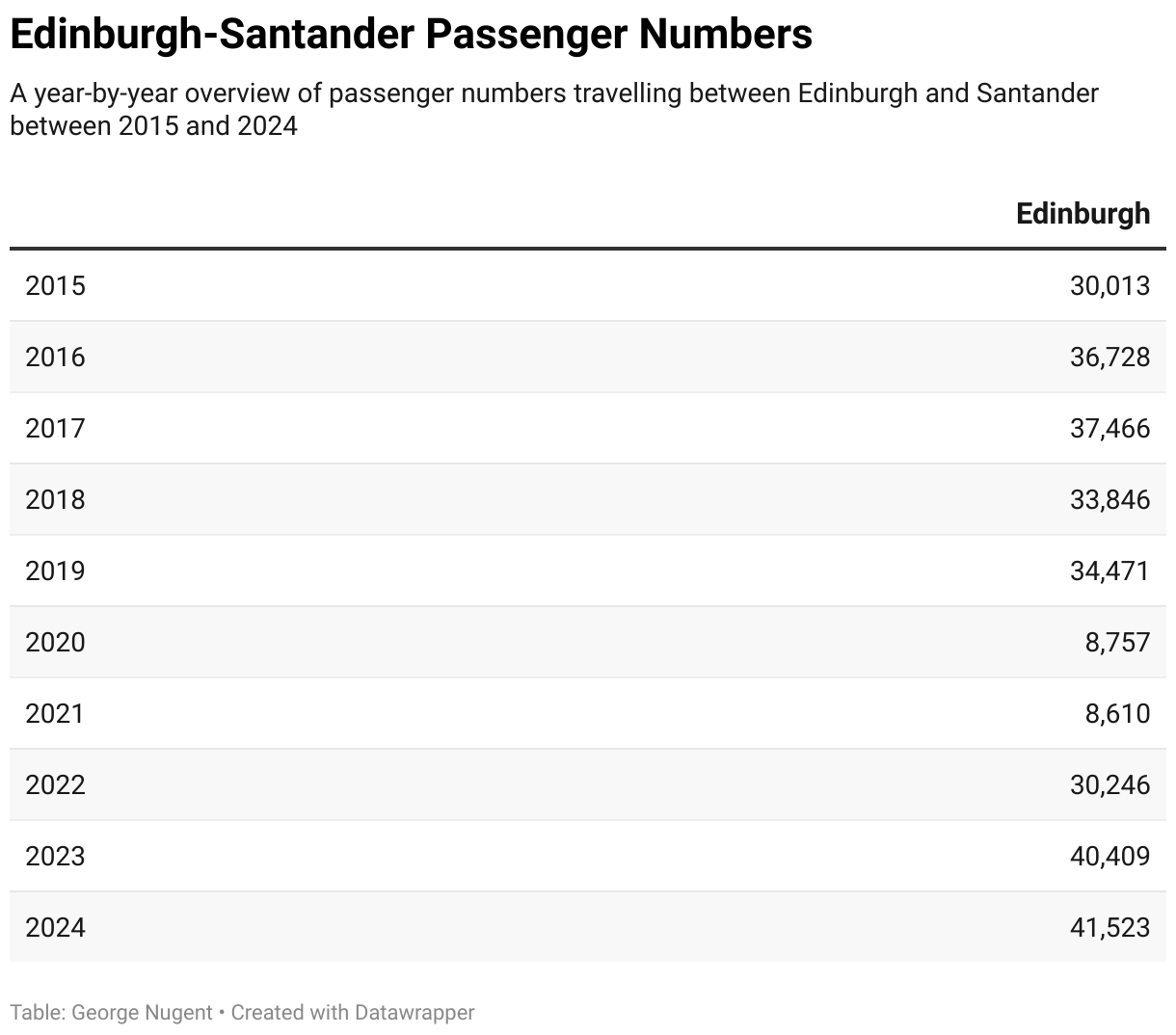

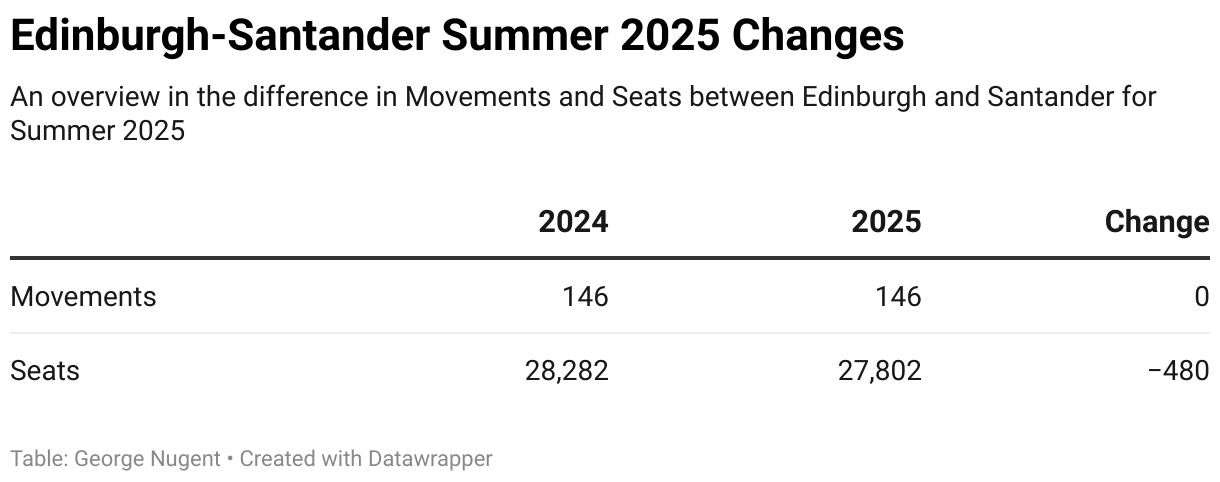

Santander

Santander is an exclusive route to Edinburgh Airport and is solely operated by Ryanair.

Passenger numbers on this route are currently operating at 120.8% of 2019 levels, and are currently operating at a consistent level, however, given the drop in flights to Northern Spain, it is somewhat surprising that passenger numbers have not increased significantly on the route, partially showing how the very presence of a flight route can create demand itself.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Ryanair (FR)

- Movements will reduce from 146 to 86 – equating to a decrease of 41%

- This means reducing from 73 to 43 round trips

- The number of seats available will reduce from 28,282 to 16,462 – equating to a decrease of 42%

Ryanair UK

- Movements will increase from 0 to 60 – a new service for Summer 2025

- The number of seats available will increase from 0 to 11,340

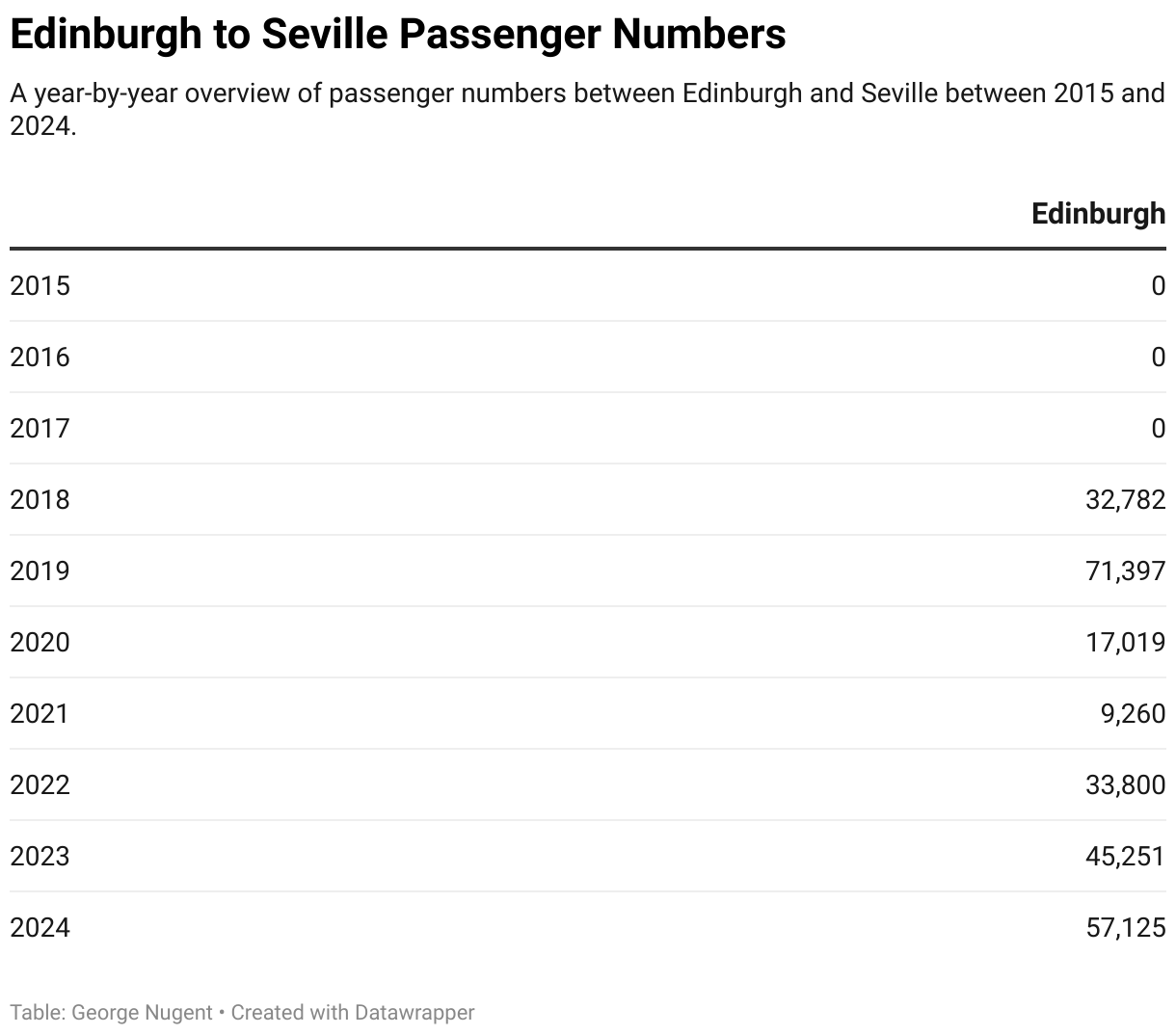

Seville

Seville remains an exclusive route from Edinburgh Airport and is operated by Ryanair, with no other Scottish Airport having seen service since 2015. Traffic levels between Edinburgh and Seville are currently operating at 80% of 2019 levels.

Despite a strong yearly recovery since the pandemic, further growth into Seville is being hampered by a dispute between AENA who operate Seville airport, and Ryanair, who currently operate the route, and with neither side backing down any time soon, passenger numbers on this route are forecast to reduce in 2025.

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Ryanair (FR)

- Movements will reduce from 180 to 120 – equating to a decrease of 33%

- This means reducing from 90 to 60 round trips

- The number of seats available will reduce from 35,044 to 22,688 – equating to a decrease of 35%

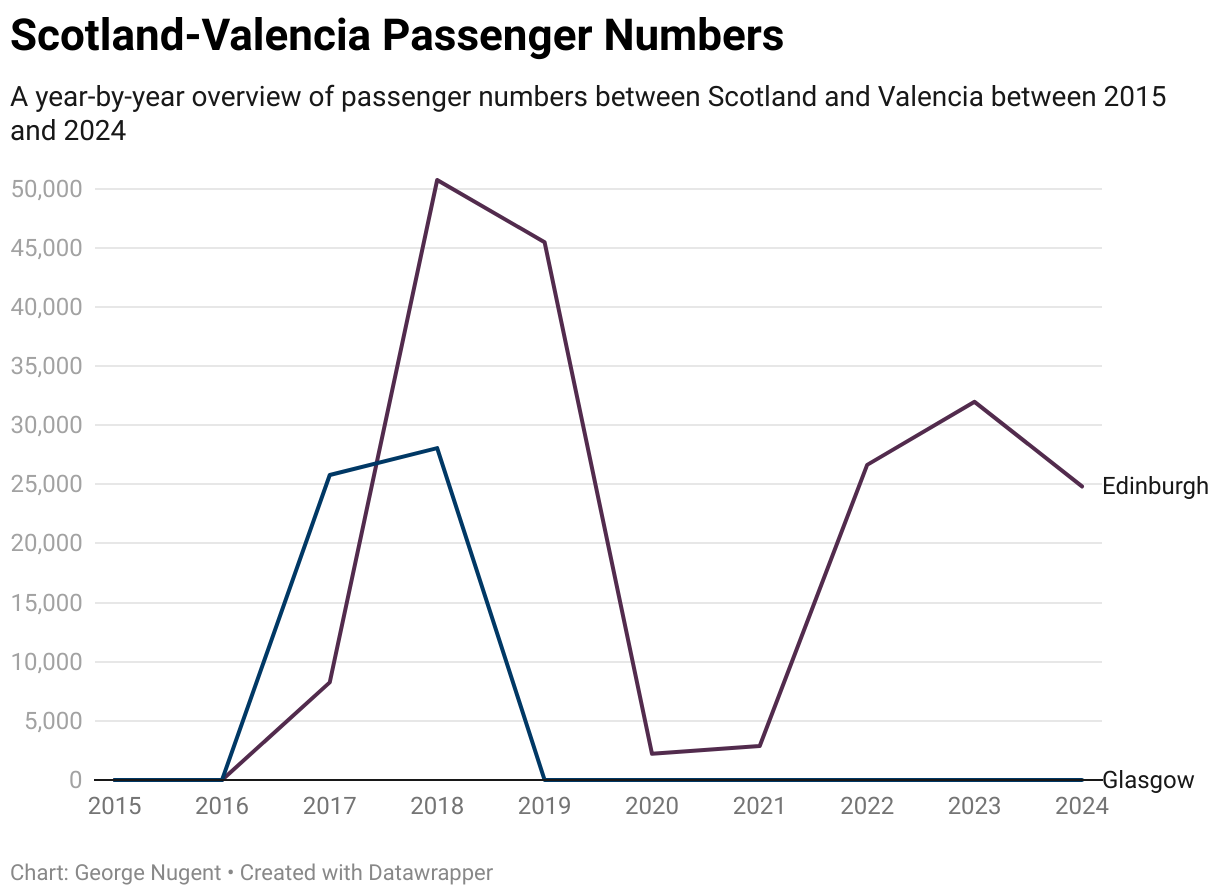

Valencia

Valencia is the second of two routes to have been impacted by the closure of Ryanair’s Glasgow base in October 2018, with the route now being exclusively operated from Edinburgh by Ryanair.

As the graph above shows, recovery to Valencia has been incredibly slow, with a decline recorded in 2024, and as I will outline below, traffic levels are predicted, based on current schedules to remain relatively flat in 2025, this may change if Ryanair reintroduces a winter flying programme from Edinburgh to Valencia.

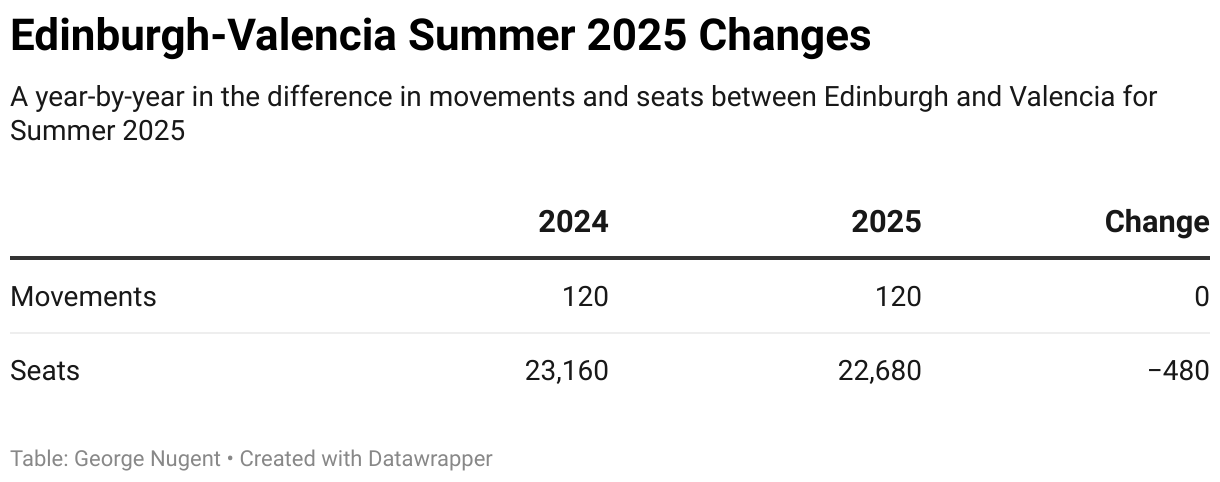

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Ryanair (FR)

- Movements will increase from 60 to 120 – equating to an increase of 100%

- This means increasing from 30 to 60 round trips

- The number of seats available will increase from 11,820 to 22,680 – equating to an increase of 92%

- Ryanair plans to downgrade a small number of flights from the larger Boeing 737-8-200 with 197 seats to the smaller Boeing 737-800 with 189 seats.

Ryanair UK

- Movements will reduce from 60 to 0 – equating to an de crease of 100%

- This means decreasing from 30 to 0 round trips

- The number of seats available will decrease from 11,340 to 0 – equating to a decrease of 100%

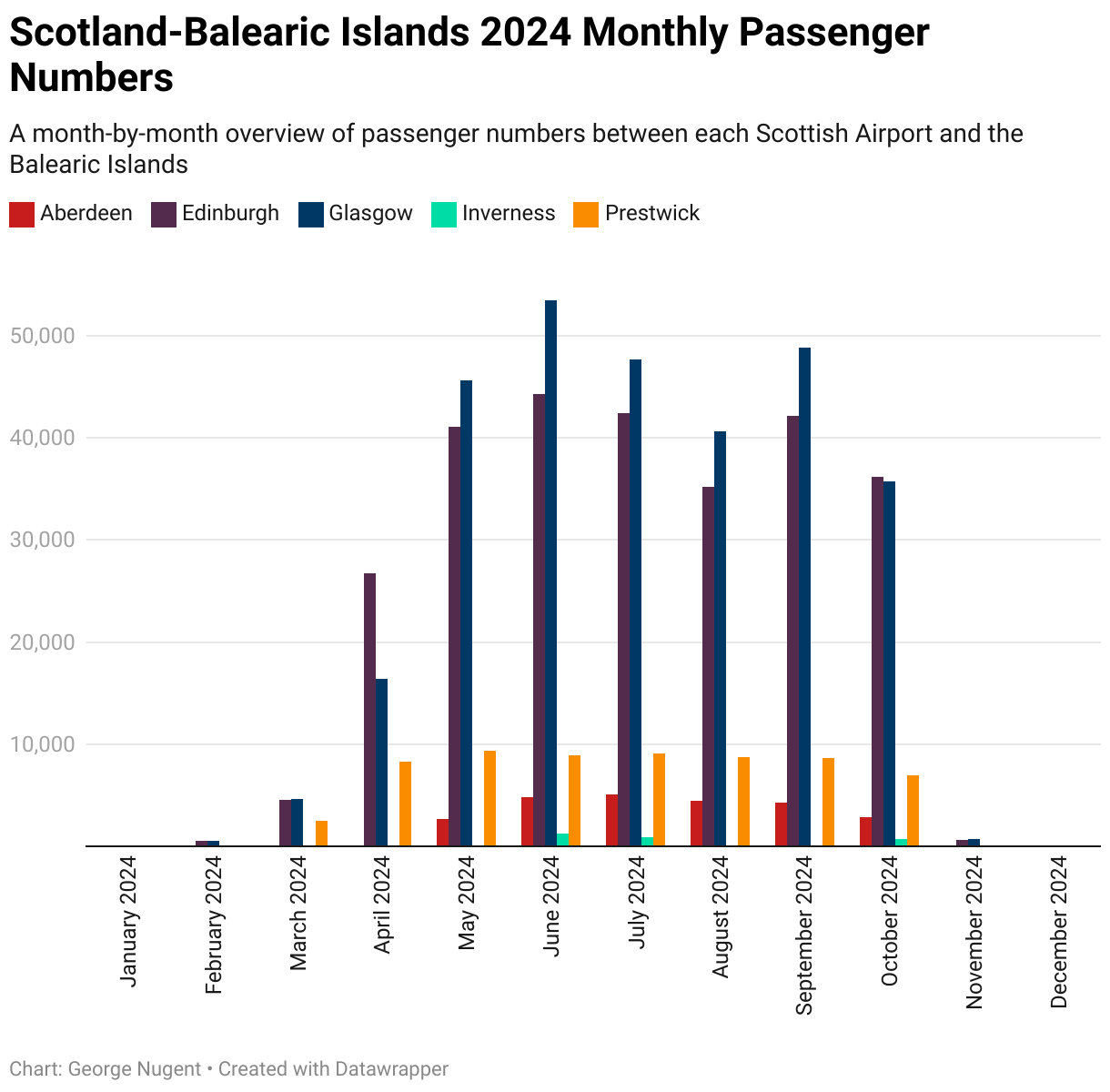

Balearic Islands

All of the data in this section specifically relates to destinations located on the Balearic Islands, all other data has been removed.

Passenger Numbers Per Month

Passenger numbers from Scotland to the Balearic Islands primarily operate in the Summer Season, however, in recent years Jet2 has brought forward its resumption date to February, and easyJet has extended its season briefly into November.

Passenger numbers trend upwards significantly in May as this is the first month that Menorca is served, and TUI significantly boosts its flights to Ibiza and Palma, with easyJet also doing the same with their Palma flights, Ryanair remains consistent throughout the season.

Glasgow on average has the higher passenger numbers, with Edinburgh only being ahead in April and October because of the presence of Ryanair on their flights rather than TUI. Passenger numbers fall in July and August as Jet2 relocate 4 aircraft to England for 6 weeks to cover the English peak holiday season.

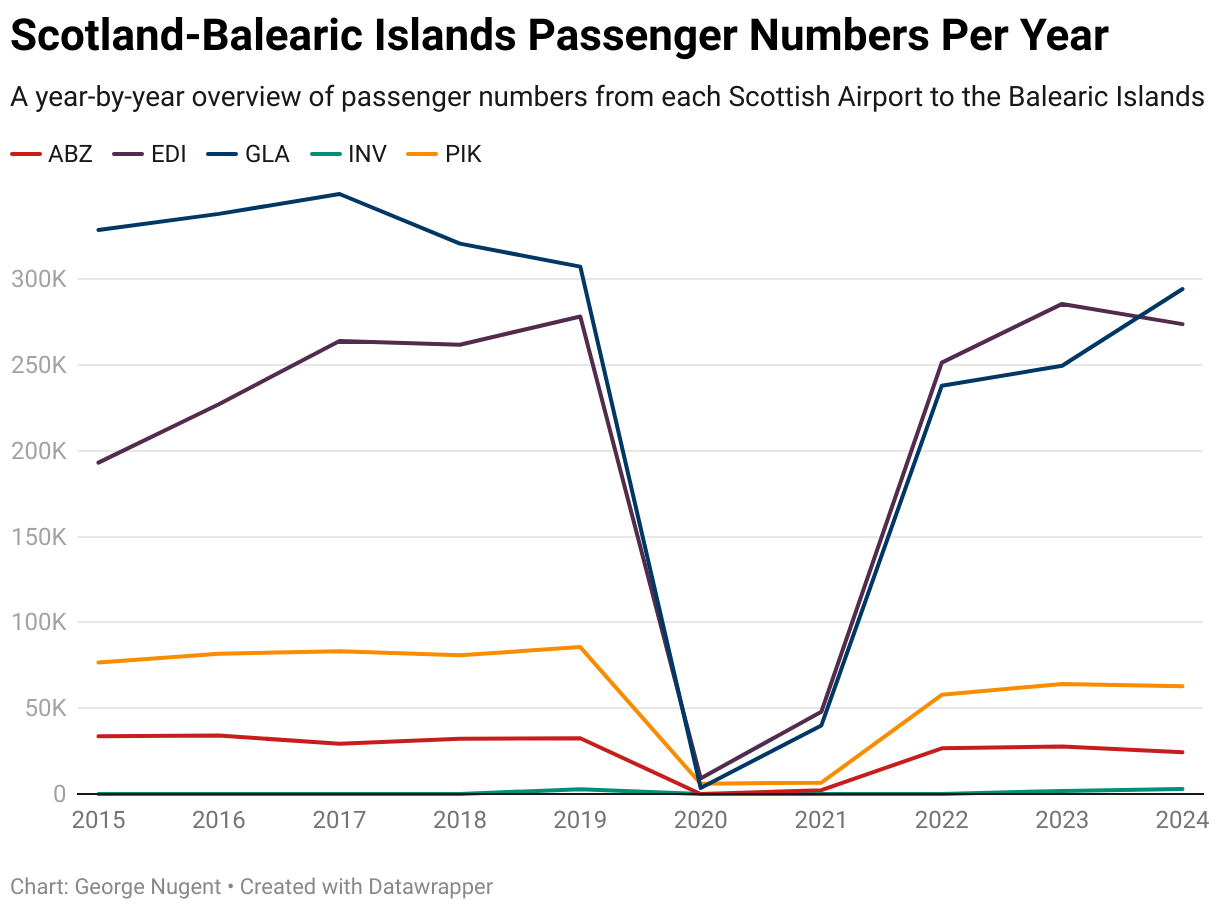

Passenger Numbers Per Year

Passenger numbers from Scotland as a whole are below 2019 levels, with passenger numbers operating at 93.2% of 2019 levels.

I should point out that Thomas Cook collapsed in September 2019, therefore, it is reasonable to assume that the actual passenger numbers for 2019 should have been higher than they were despite airlines best attempts to source additional capacity.

TUI also closed its bases in Aberdeen and Edinburgh, choosing instead to consolidate their operations from Glasgow, with services from other airports significantly reduced.

The recovery rate for each airport compared to 2019 is listed below;

- Aberdeen = 74.9%

- Edinburgh = 98.4%

- Glasgow = 95.8%

- Inverness = 106.1%

- Prestwick = 73.3%

A more detailed route by route breakdown is available in the sections after this that will outline some of the passenger numbers and routes that have not returned.

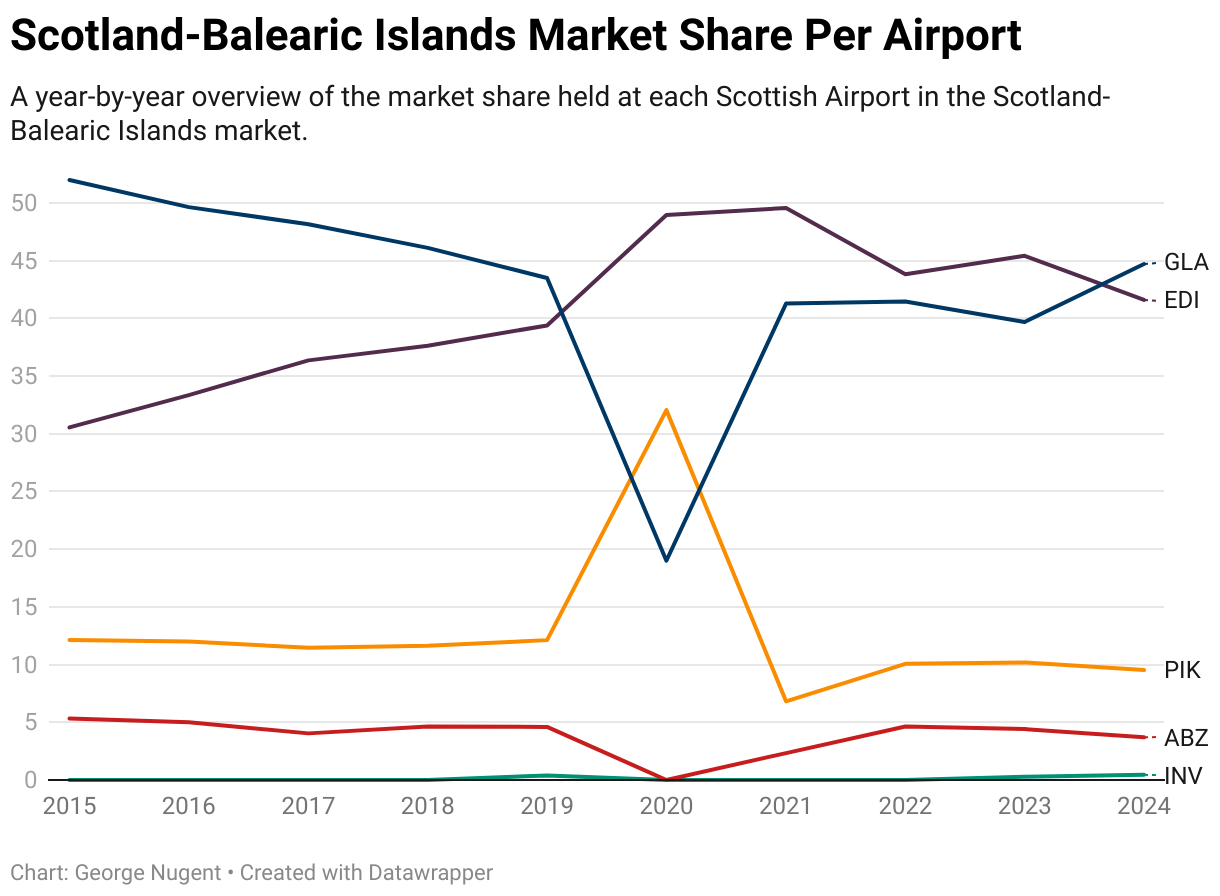

Market Share Per Airport

Market share has varied significantly since 2015, with Edinburgh Airport making year on year progress in closing the gap to Glasgow, with the pandemic finally allowing them to overtake. In 2024, thanks to a decline in passenger numbers at Edinburgh Airport in this market, Glasgow has retaken the position as the largest airport in the market, but has not taken back its 2015 status of having a majority.

Route Specific Information

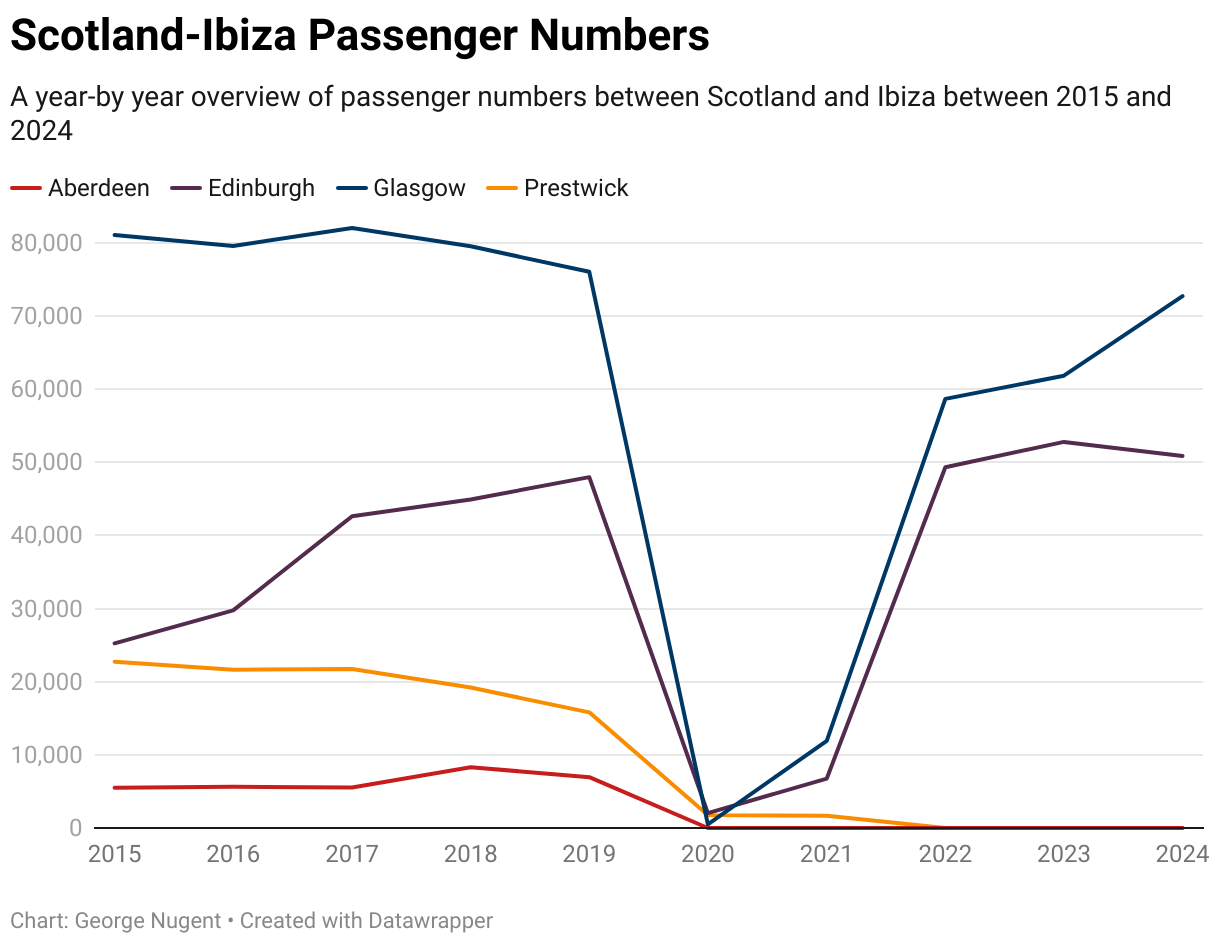

Ibiza

Ibiza is an example of why providing context to statistics is important, as what appears on the surface is sometimes is discussing something deeper behind the surface.

Passenger numbers are highest at Glasgow Airport and grew when compared to 2023, unlike Edinburgh Airport where passenger numbers declined slightly on the year before, the recovery rate for each airport is below;

- Aberdeen – Suspended

- Edinburgh – 106%

- Glasgow – 95.6%

- Prestwick – Suspended

As I mentioned above, despite passenger numbers being higher at Glasgow Airport, full passenger recovery has only occurred at Edinburgh Airport, with Glasgow still recovering and Aberdeen and Prestwick remaining suspended.

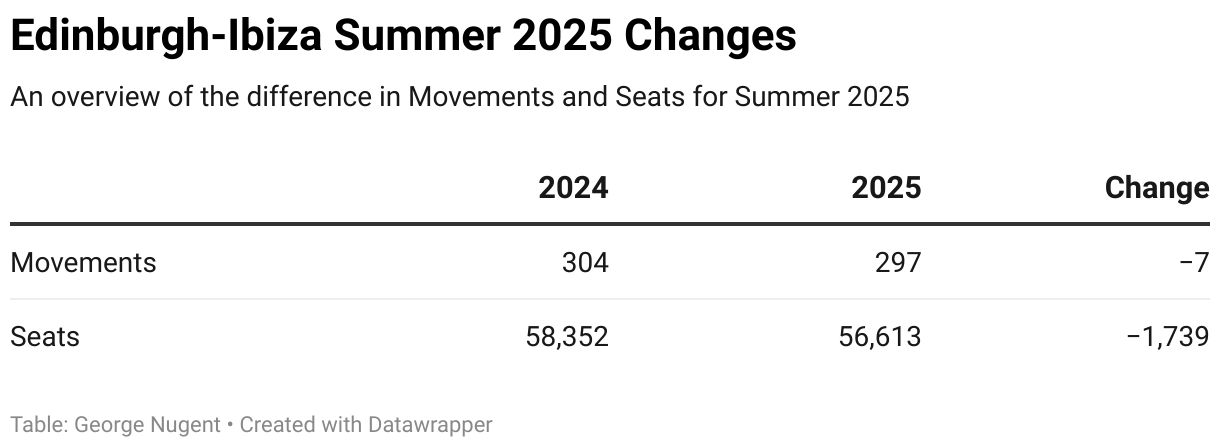

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Jet2

- Movements will decrease from 184 to 177 – equating to a decrease of 4%

- This means decreasing from 92 to 88.5 round trips

- The number of seats available will decrease from 23,576 to 23,160 – equating to a decrease of 4%

Ryanair

- Movements will remain at 120, the same as Summer 2024

- This means 60 round trips will operate

- The number of seats available will decrease slightly from 23,576 to 23,160 – equating to a decrease of 2%

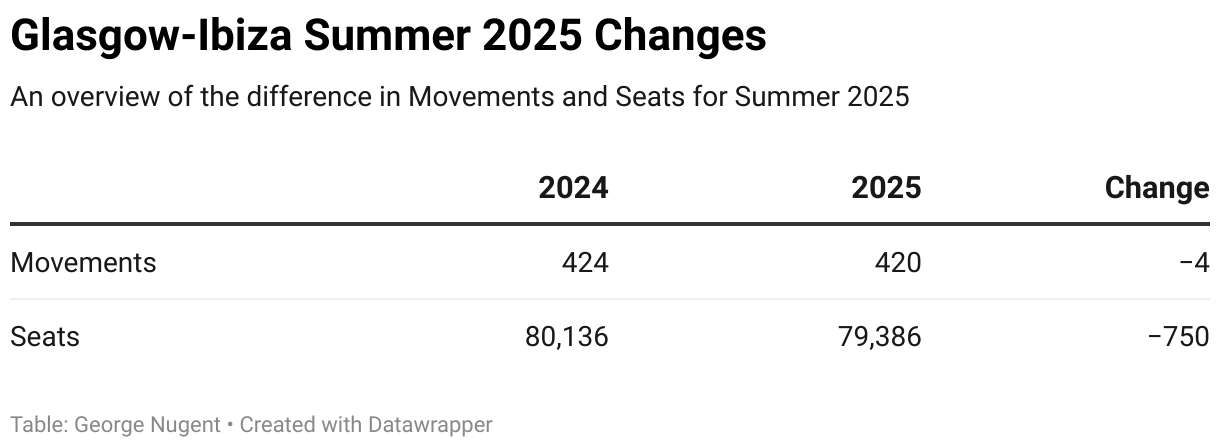

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

Jet2

- Movements will remain at 292, the same as Summer 2024

- This means 146 round trips will operate

- The number of seats available will remain at 23,576

TUI

- Movements will decrease slightly from 132 to 128 – equating to a decrease of 3%

- This means decreasing from 66 to 64 round trips

- The number of seats available will decrease from 24,948 to 24,198

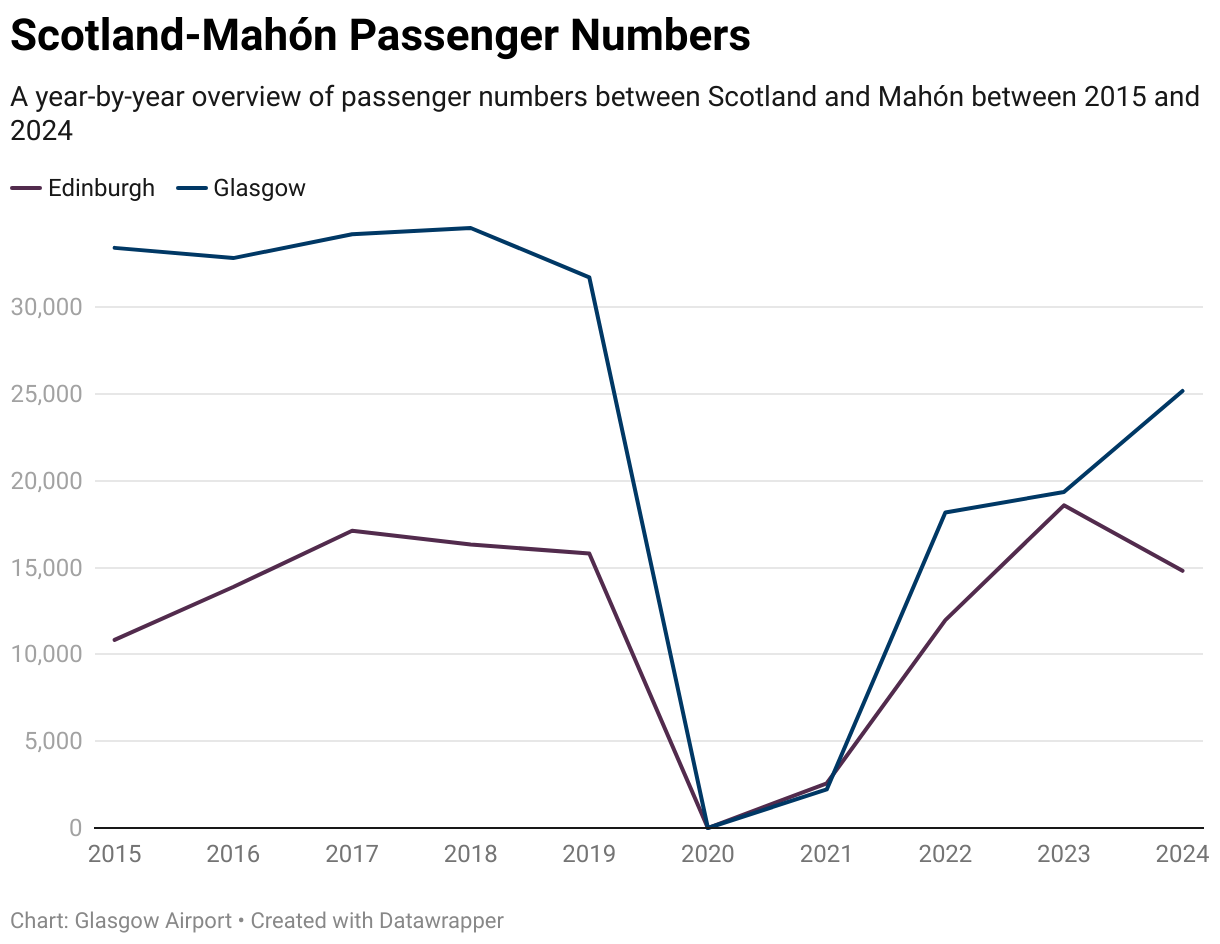

Mahón

When looking at the Balearic Islands, Mahón has the slowest recovery rate of the three destinations served, but was also the most impacted by the collapse of Thomas Cook in 2019.

As of the end of 2024, Edinburgh lost its status as the only airport to have recovered to 2019 levels – not because Glasgow also recovered, but rather because passenger numbers on the route fell by 20%, taking the total to below 2019 levels once again.

Current passenger numbers between Scotland and Mahón are operating at 84.1% of 2019 levels, with little prospect of this figure increasing in 2025.

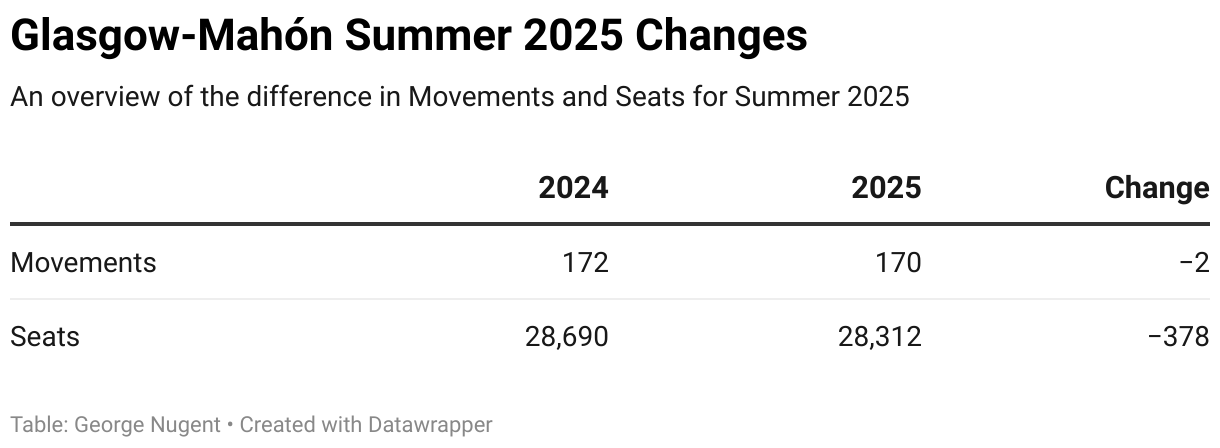

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Jet2

- Movements will remain at 90, the same as Summer 2024

- This means that 45 round trips will operate

- The number of seats available will remain the same at 17,010

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

Jet2

- Movements will reduce slightly from 126 to 124 – equivalent to a decrease of 2%

- This means reducing from 63 to 62 round trips

- The number of seats available will decrease from 23,814 to 23,436

TUI – Operated by British Airways CityFlyer

- Movements will remain at 46, the same as Summer 2024

- This means 23 round trips will operate

- The number of seats available will remain at 4,876

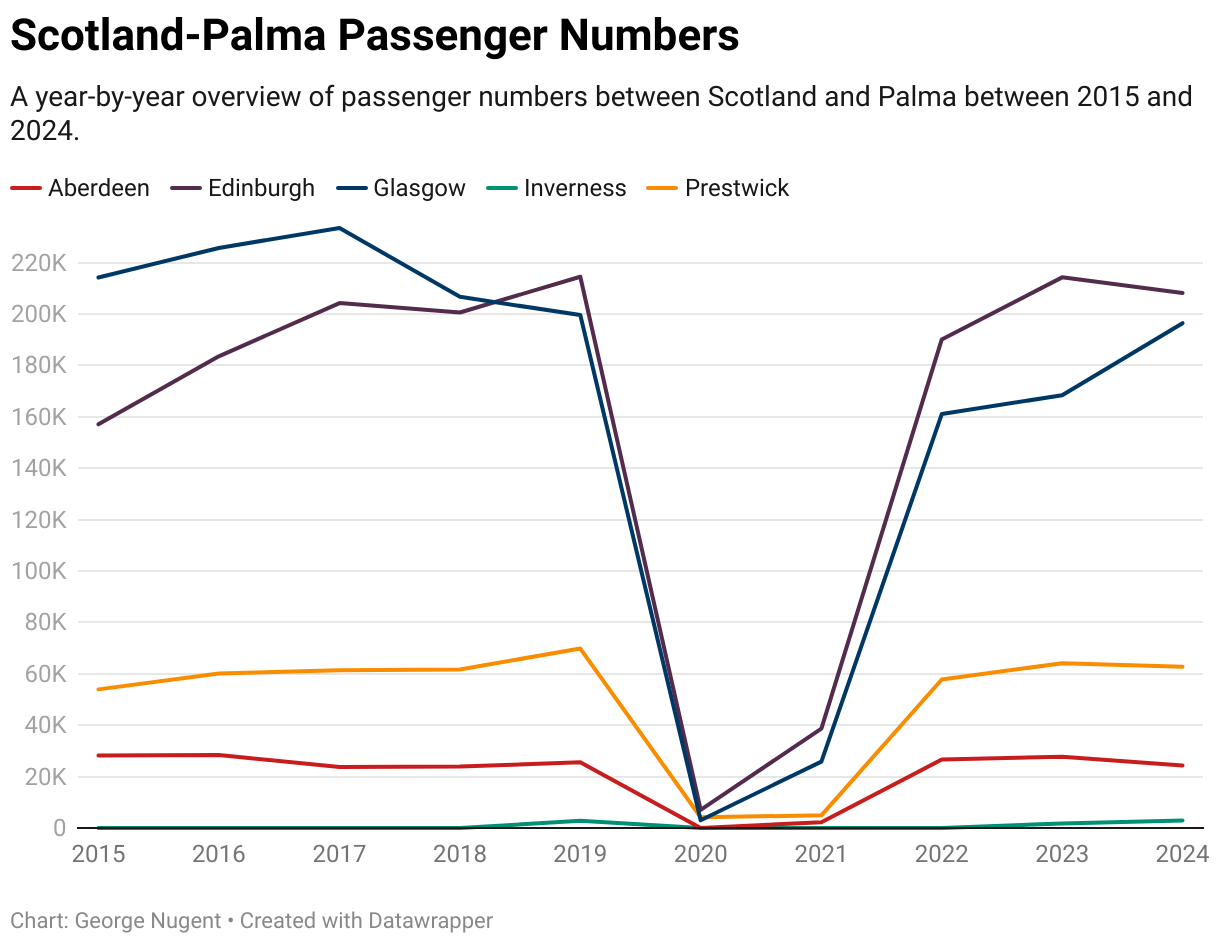

Palma

Passenger numbers between Scotland and Palma continue to operate below 2019 levels, however, recovery has been hindered by the collapse of Thomas Cook, as well as the decision by TUI to close its Aberdeen and Edinburgh bases.

Edinburgh Airport remains the largest source of passengers between Scotland and Palma, however, this is largely as a result of the mix of airlines operating on the route compared to Glasgow. Both airports see services operated by easyJet and Jet2, however, the deal breaker for this route is Ryanair at Edinburgh vs TUI in Glasgow. Ryanair operates consistently from the end of March until the end of October, unlike TUI who slowly build operations up from March-June and then scale back in October.

Services from Aberdeen are operated by TUI, either using their own aircraft or those of a third party on TUI’s behalf, in the case of Summer 2024 this was AlbaStar. Flights from Prestwick are operated by Ryanair, with one of the weekly flights being operated by their Lauda subsidiary.

In terms of recovery, the Scotland-Palma market as a whole is operating at 96.6% of 2019 levels, with the recovery rate for each airport listed below;

- Aberdeen – 95.3%

- Edinburgh – 97.1%

- Glasgow – 98.4%

- Inverness – 106.1%

- Prestwick – 96.6%

As seen above, all airports bar Inverness are below pre-pandemic levels, however, given the changes in travel habits since 2019, this is a very strong recovery and is unusual in the fact that each airport is very close to each other.

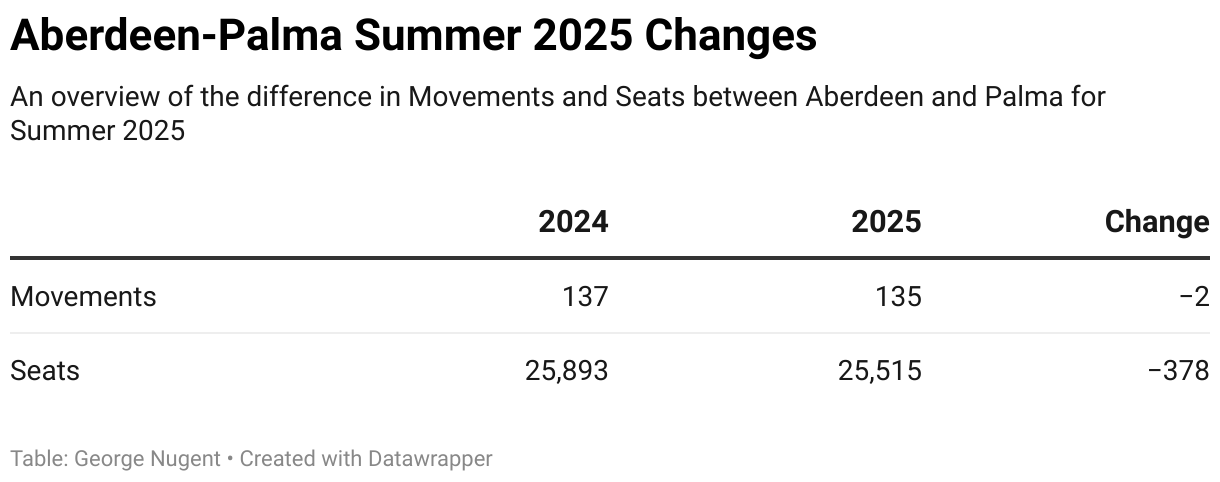

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Aberdeen Airport shows the following in terms of movements and seats;

AlbaStar – Operated a number of TUI flights in 2024

- Movements will decrease from 86 to 0 – equivalent to a drop of 100%

- This means decreasing from 43 to 0 round trips

- Seats will decrease from 16,254 from 0 – equivalent to a drop of 100%

TUI – Operated by TUI Themselves

- Movements will increase from 51 to 135 – equivalent to an increase of 165%

- This means increasing from 25.5 to 67.5 round trips

- Seats will increase from 9,639 to 25,515 – equivalent to an increase of 165%

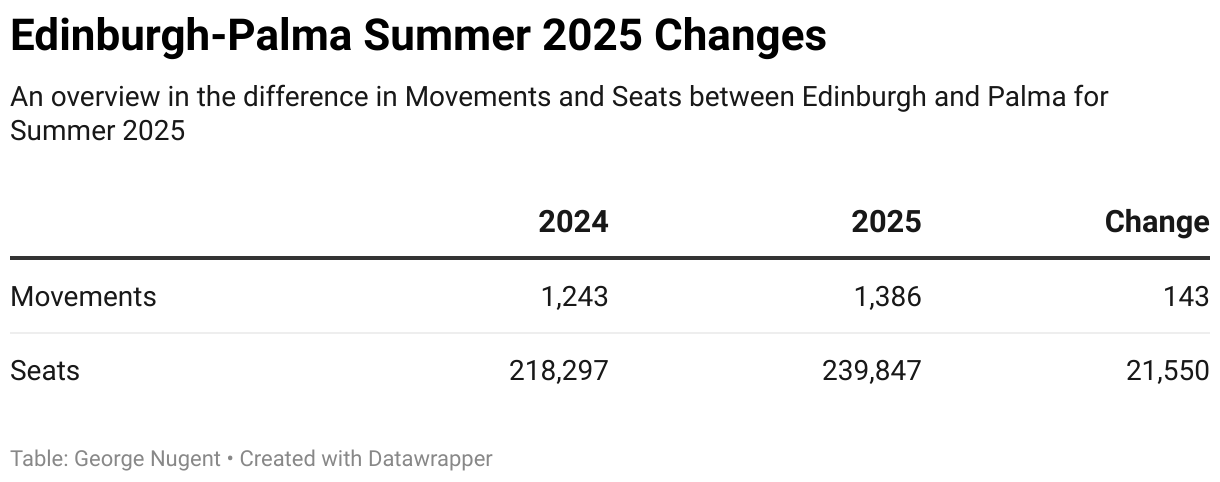

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

British Airways CityFlyer – Includes flights they operated for themselves and also flights operated for TUI

- Movements will increase from 174 to 227 – equivalent to an increase of 30%

- This means increasing from 87 to 113.5 round trips

- Seats available will increase from 18,380 to 24,062 – equivalent to an increase of 31%

easyJet Europe

- Movements will increase from 120 to 180 – equivalent to an increase of 50%

- This means increasing from 60 to 90 round trips

- Seats available will increase from 18,780 to 31,680 – equivalent to an increase of 69%

- easyJet are not only increasing flights, but upscaling the size of aircraft on a number of existing flights

Jet2

- Movements will remain the same at 464, the same as Summer 2024

- This means that round trips operating will remain at 232

- Seats available will increase from 87,696 to 98,962 – equivalent to an increase of 13%

- Jet2 will upscale a number of flights from the smaller Boeing 737-800 to the larger Airbus A321

Ryanair (FR)

- Movements will increase from 376 to 406 – equivalent to an increase of 8%

- This means increasing from 188 to 203 round trips

- Seats available will increase from 72,840 to 75,882 – equivalent to an increase of 4%

Ryanair UK

- Movements will remain the same at 60 movements, the same as Summer 2024

- This means 30 round trips will operate

- Seats available will remain the same at 11,340

TUI – Operated by TUI on their own aircraft

- Movements will remain the same at 49, the same as Summer 2024

- This means 24.5 round trips will operate

- Seats available will remain the same at 9,261

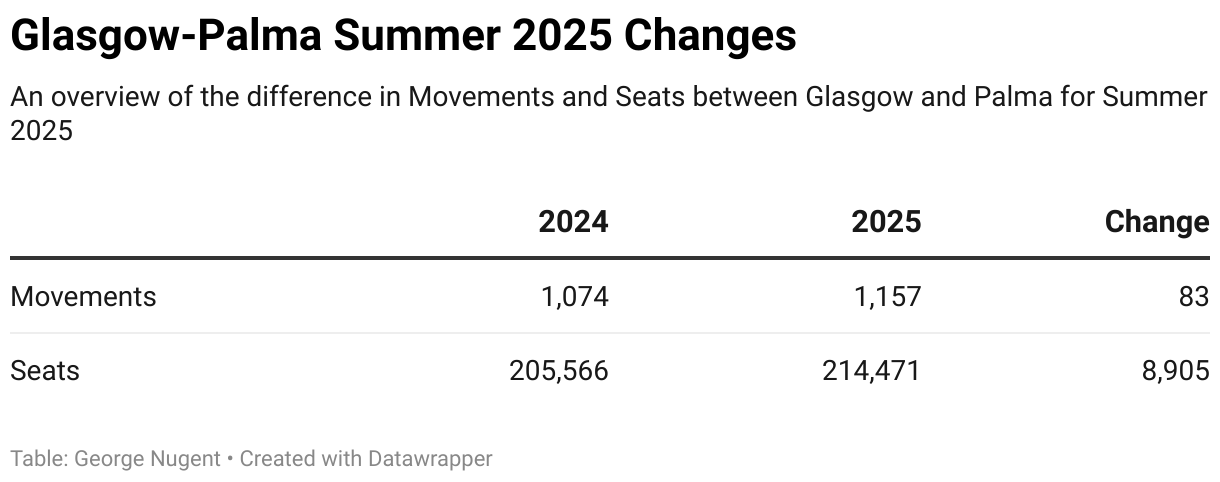

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

British Airways CityFlyer – Operating on behalf of TUI

There was a small problem with this, the ACL SoSR does not feature these flights despite the fact they are operating, therefor I have calculated the movement and seats figures based on the TUI timetable using Embraer 190 aircraft with 106 seats.

- Movements will increase from 0 to 49 – a “new service” for Summer 2025

- This means increasing from 0 to 24.5 round trips

- The number of seats available will increase from 0 to 5194

easyJet Europe

- Movements will increase from 224 to 292 – equivalent to an increase of 30%

- This means increasing from 112 to 146 round trips

- The number of seats available will increase from 39,204 to 49,452 – equivalent to an increase of 26%

easyJet UK

- Movements will remain at 20, the same as Summer 2024

- This means 10 round trips will operate

- The number of seats will remain the same at 3,720

Jet2

- Movements will increase from 560 to 576 – equivalent to an increase of 3%

- This means increasing from 280 to 288 round trips

- The number of seats will increase from 105,840 to 108,864 – equivalent to an increase of 3%

TUI – Operated by TUI themselves on their own aircraft

- Movements will decrease from 270 to 220 – equivalent to a decrease of 19%

- This means decreasing from 135 to 110 round trips

- The number of seats available will decrease from 56,802 to 47,241 – equivalent to a decrease of 17%

Moving to Prestwick Airport, no Start of Season Report is published, however, Ryanair will continue to operate 6 weekly flights, and has also upgraded a number of flights to the larger Boeing 737-8-200 series of aircraft with 197 seats. It should be noted that Ryanair will continue to operate one of these weekly flights with a Lauda A320 with 180 seats.

As a result, passenger numbers on the route should increase when compared to Summer 2024.

Canary Islands

All of the data in this section specifically relates to destinations located on the Canary Islands, all other data has been removed.

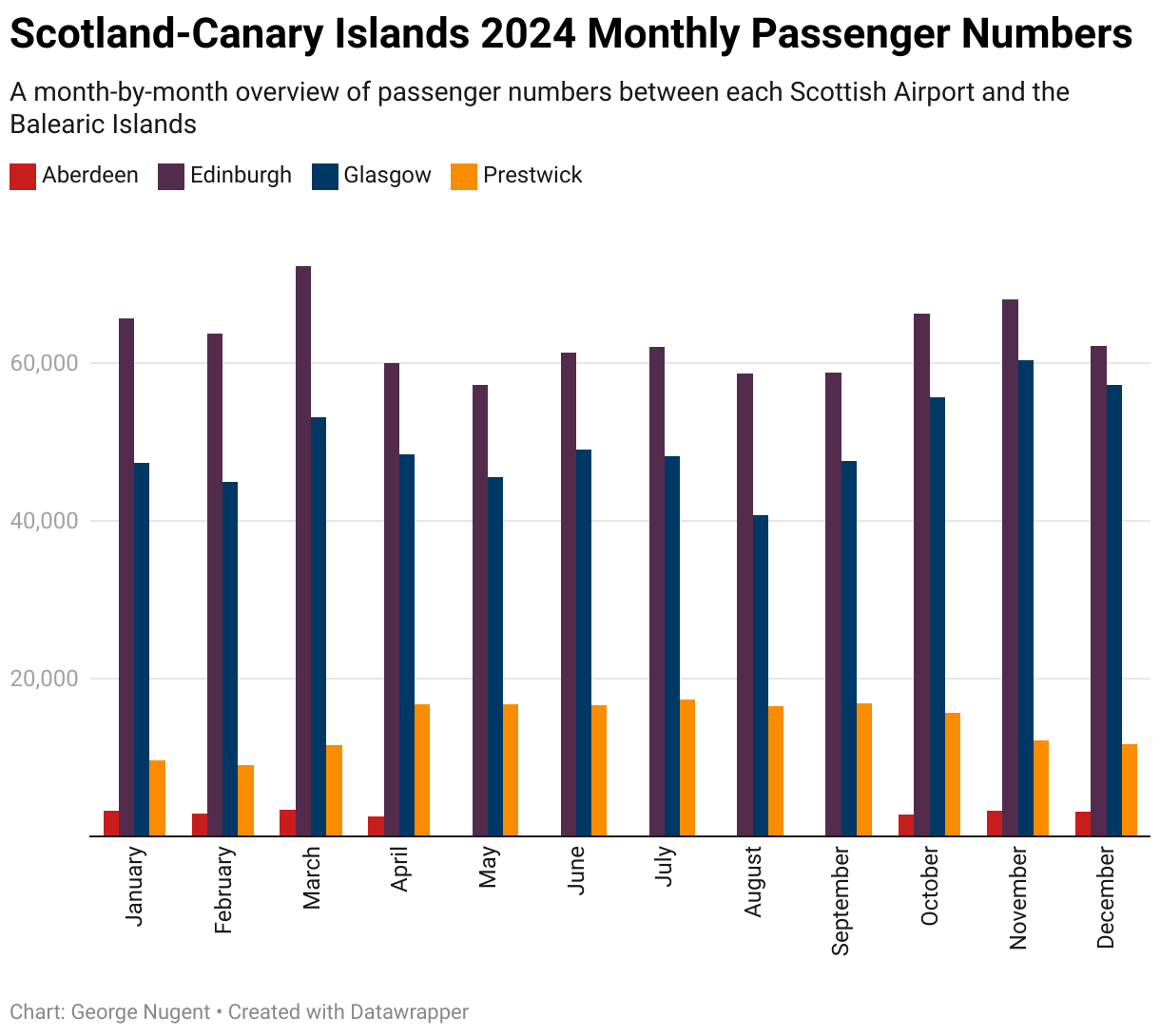

Passenger Numbers Per Month

Passenger numbers from Scotland to the Canary Islands primarily operate throughout the year at a relatively consistent level, however, passenger numbers do fall slightly in the summer months as airlines fly their aircraft elsewhere.

One notable trend in 2024 is the significant closing gap between Edinburgh and Glasgow Airports, with Glasgow making significant progress in narrowing the gap thanks to the addition of two new easyJet routes, adding 4 weekly flights, compared to the 1 weekly new easyJet route added from Edinburgh.

Aberdeen remains a seasonal departure point during the winter as a result of TUI’s decision to remove it’s based aircraft from Aberdeen, meaning there is no longer an aircraft available to operate the route between May and October.

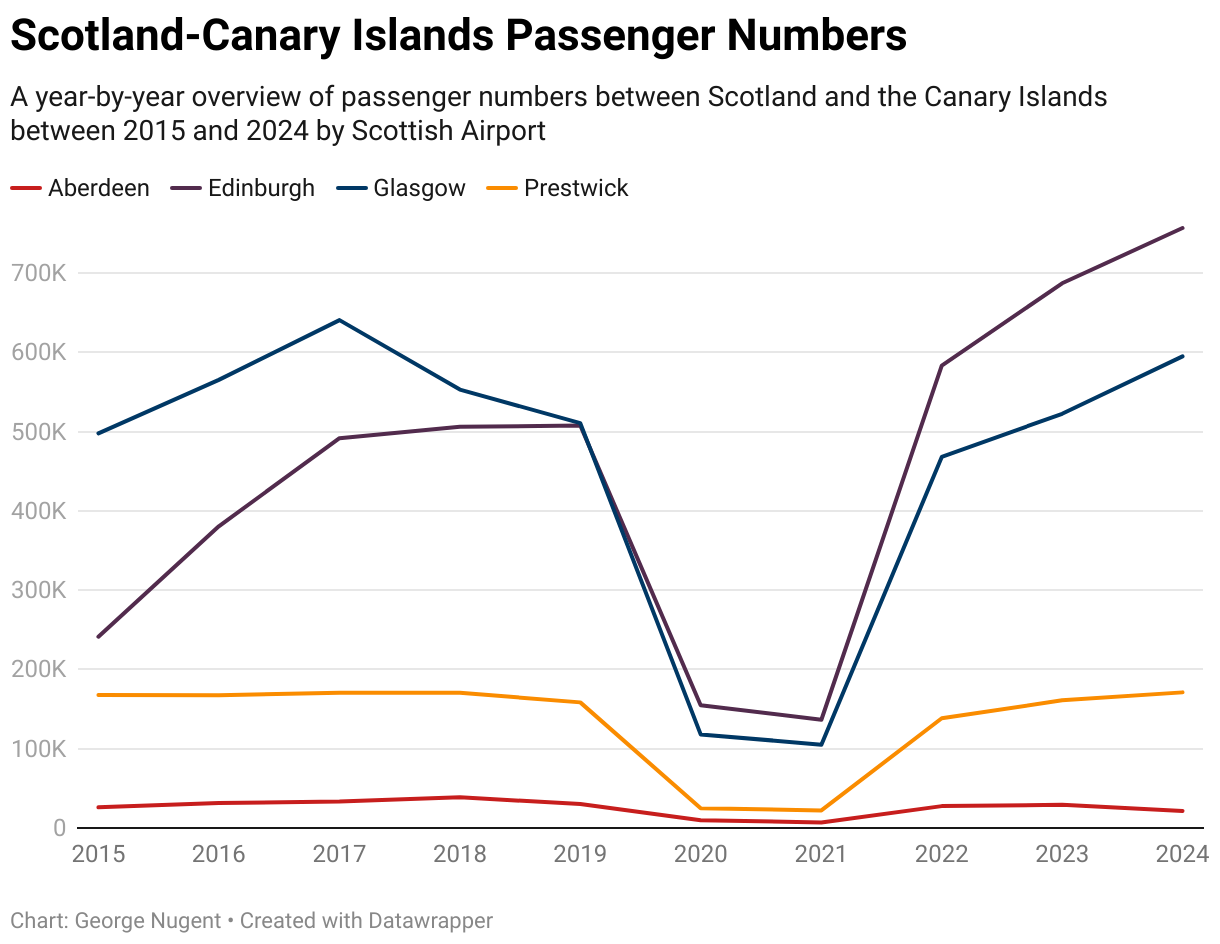

Passenger Numbers Per Year

Passenger numbers from Scotland as a whole are significantly above 2019 levels, at the end of 2024 passenger numbers were 127.95% of 2019 levels, but this was not an even story across the country.

I should point out that Thomas Cook collapsed in September 2019, therefore, it is reasonable to assume that the actual passenger numbers for 2019 should have been higher than they were despite airlines best attempts to source additional capacity.

TUI also closed its bases in Aberdeen and Edinburgh, choosing instead to consolidate their operations from Glasgow, with services from other airports significantly reduced.

The recovery rate for each airport compared to 2019 is listed below;

- Aberdeen = 71.4%

- Edinburgh = 149.1%

- Glasgow = 116.5%

- Prestwick = 108%

A more detailed route by route breakdown is available in the sections after this that will outline some of the passenger numbers and routes that have not returned.

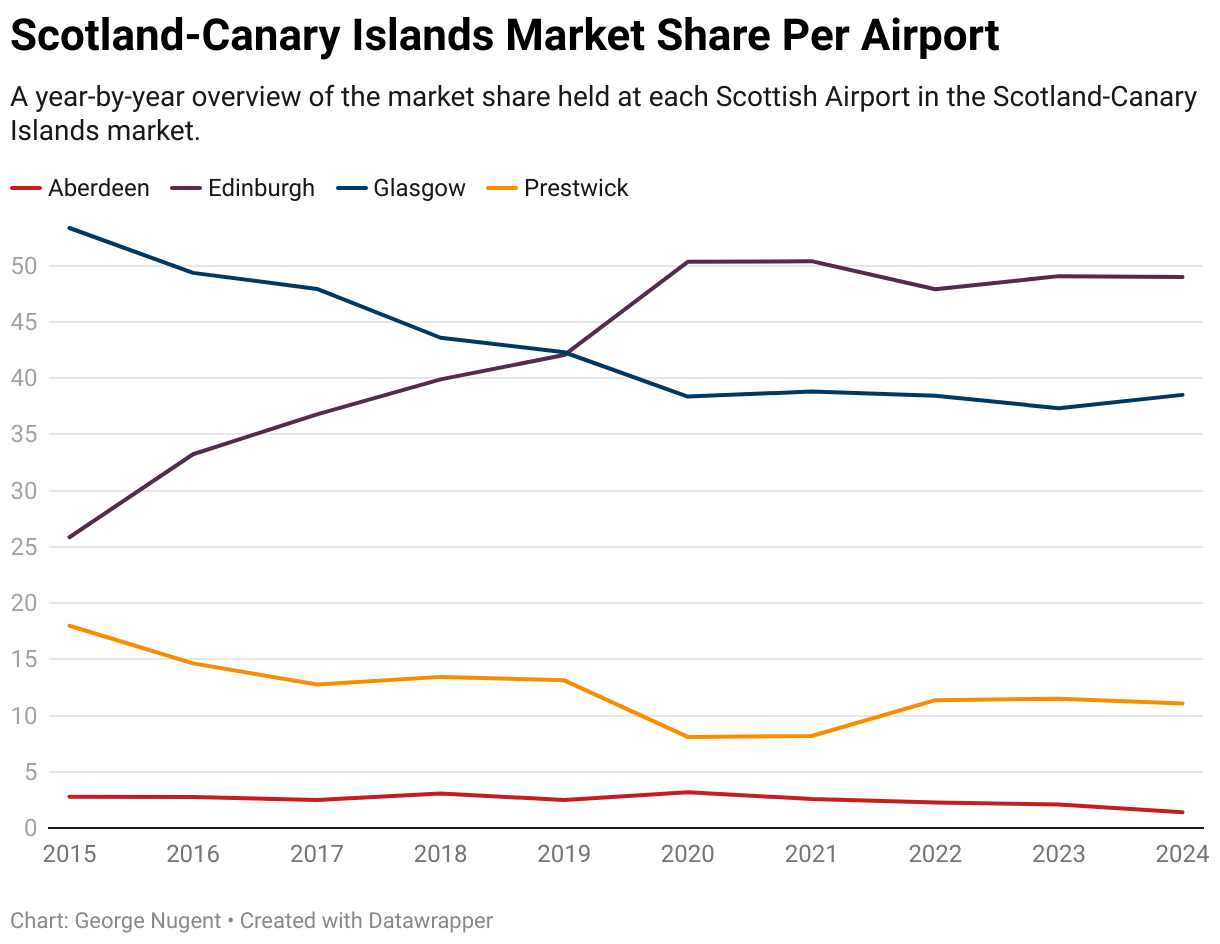

Market Share Per Airport

Before the pandemic there was a clearly emerging trend, market share in Glasgow was reducing significantly in favour of Edinburgh, and actually in 2019, the two airports were level with each other at 42% market share.

Since the pandemic that trend continued, with Edinburgh now 11 percentage points higher than Glasgow in terms of market share, despite both having record passenger levels to the Canaries in 2024

Elsewhere, Prestwick market share remains relatively stable, while Aberdeen declines slightly as a result of the reduction from year round to seasonal Tenerife flights.

Route Specific Numbers

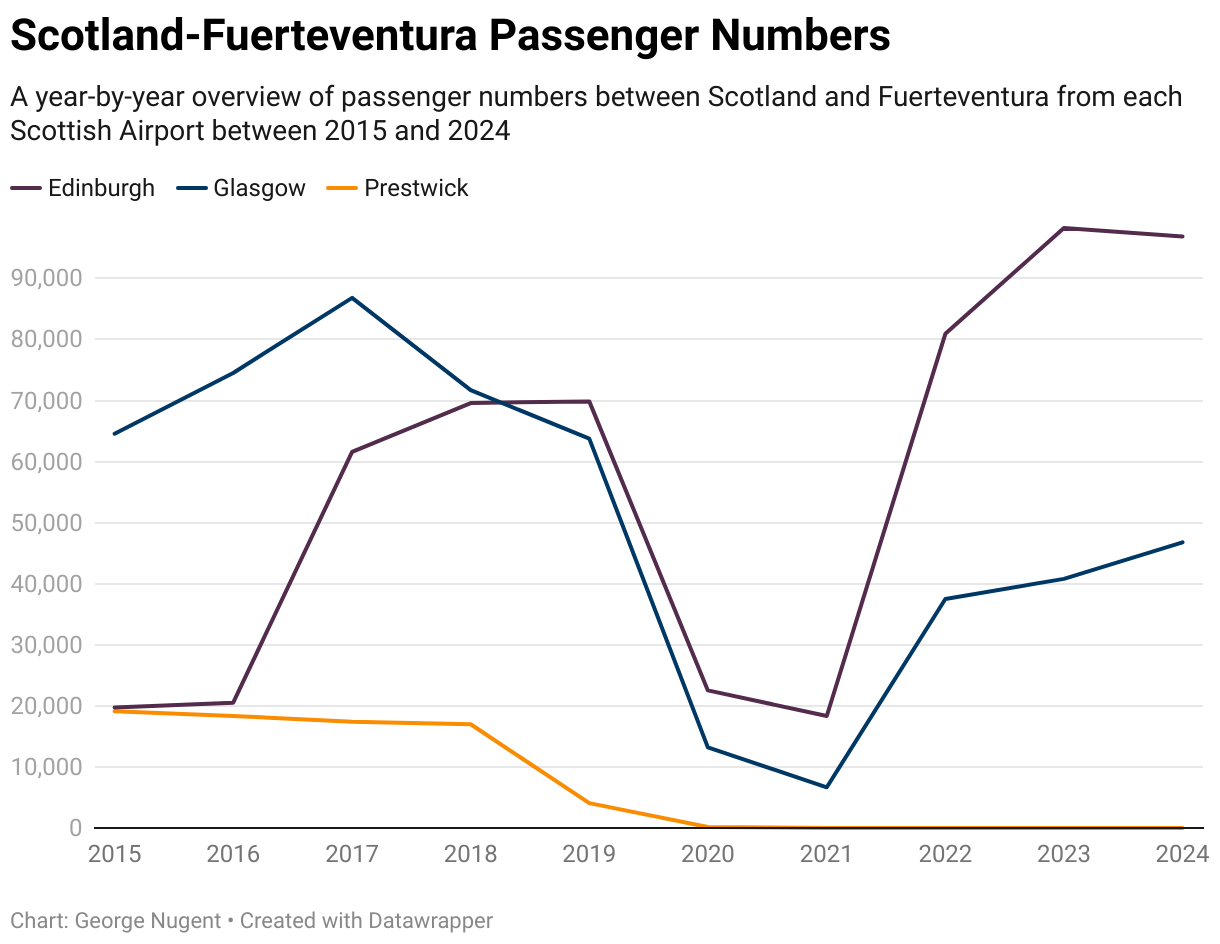

Fuerteventura

Passenger numbers between Scotland and Fuerteventura are operating above 2019 levels, however, this recovery has been very one sided, with only Edinburgh having recovered passenger numbers, meanwhile Prestwick remains unserved as of the end of 2024.

In terms of recovery, the Scotland-Fuerteventura market as a whole is operating at 104.34% of 2019 levels, with the recovery rate for each airport listed below;

- Edinburgh – 138.67%

- Glasgow – 73.38%

- Prestwick – Suspended

As seen above, Edinburgh has absolutely raced ahead of Glasgow in terms of recovery. Part of the reason for this is although Jet2 serve both airports year round and easyJet seasonally during the winter, Edinburgh benefits from also having Ryanair operating the route year round as well (I should point out TUI planned GLA-FUE for 2020).

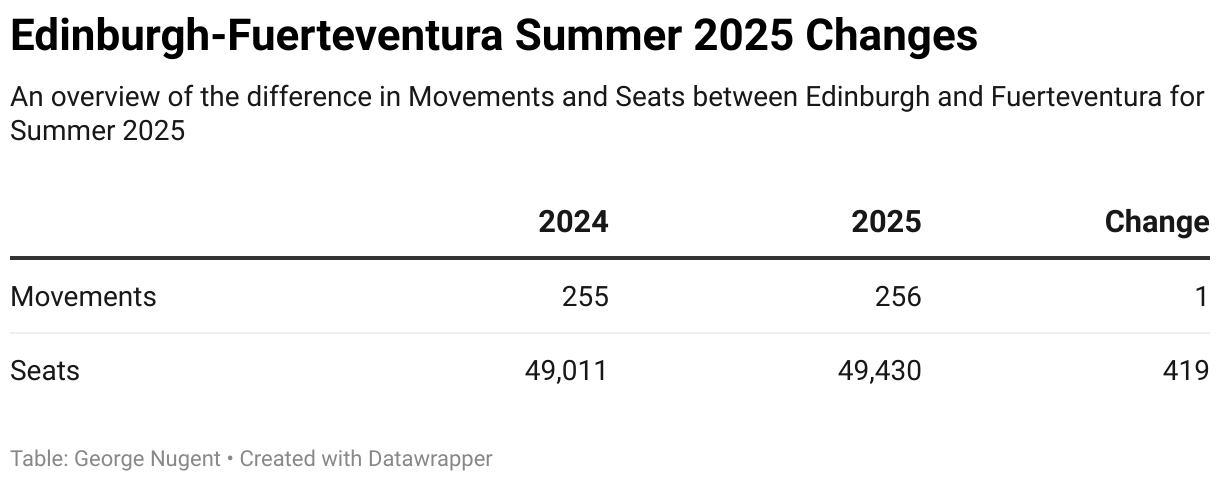

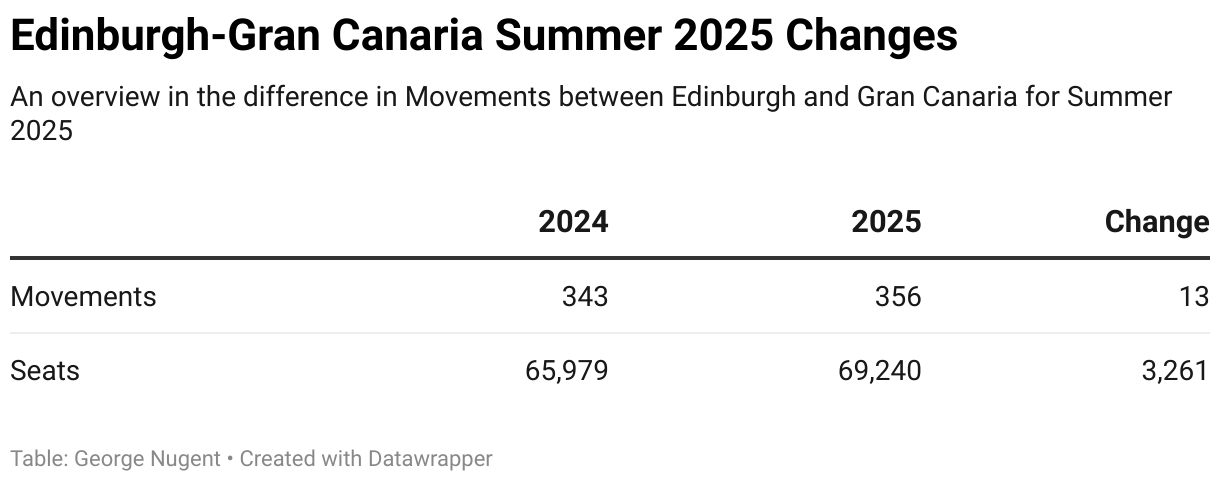

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Jet2

- Movements will increase from 135 to 136 – equating to an increase of 1%

- This means increasing from 67.5 to 68 round trips

- Seats available will increase from 25,515 to 25,790

Ryanair (FR)

- Movements will remain at 120, the same as Summer 2024

- This means 60 round trips will operate

- Seats available will increase slightly from 23,496 to 23,640

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

Jet2

- Movements will increase from 120 to 131 – equivalent to an increase of 9%

- This means increasing from 60 to 65.5 round trips

- Seats available will also increase from 22,680 to 24,759 – equivalent to an increase of 9%

Gran Canaria

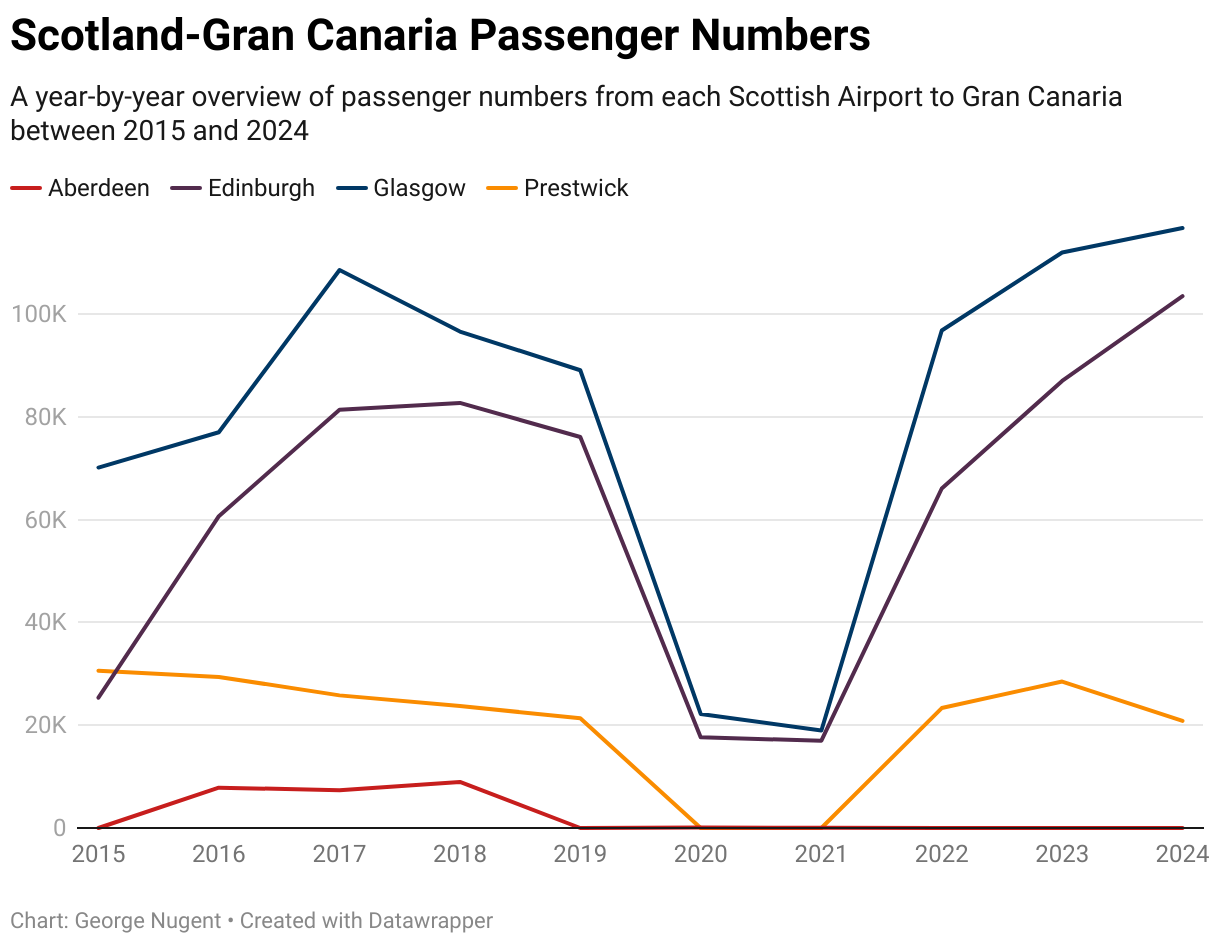

Gran Canaria is for me host to one of the most interesting comparisons, and really shows how Edinburgh Airport has grown passenger numbers through its doors in the last ten years.

In 2015 Prestwick was the second largest source of LPA passengers, with the gap to Edinburgh being 5,254. Fast forward to today, and Edinburgh has overtaken Prestwick for second place, and widened the gap to 82,651.

As a total market, Gran Canaria passenger numbers at the end of 2024 were operating at 129.26% of 2019 levels, with the full recovery rate for each airport below;

- Edinburgh = 136.01%

- Glasgow = 131.07%

- Prestwick = 97.62%

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

Jet2

- Movements will decrease from 181 to 176 – equivalent to a decrease of 3%

- This means decreasing from 90.5 round trips to 88 round trips

- Seats available will decrease from 34,209 to 33,780 – equating to a decrease of 1%

Ryanair (FR)

Seats available will increase from 31,770 to 35,460 – equating to an increase of 12%

Movements will increase from 162 to 180 – equivalent to an increase of 11%

This means increasing from 81 to 90 round trips

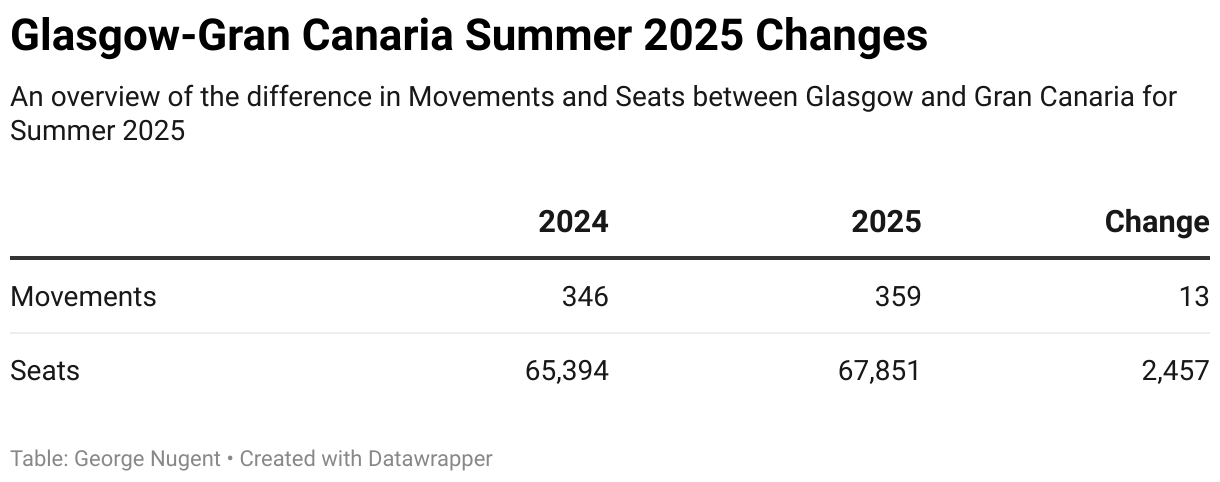

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

Jet2

- Movements will increase from 226 to 239 – equivalent to an increase of 6%

- This means increasing from 113 round trips to 129.5 round trips

- Seats available will increase from 42,714 to 45,171- equating to an increase of 6%

TUI

- Movements will remain at 120, the same as Summer 2024

- This means 60 round trips will operate

- Seats available will remain the same at 22,680

Moving to Prestwick Airport, no Start of Season Report is published, however, Ryanair will continue to operate 2 weekly flights, and has also upgraded a number of flights to the larger Boeing 737-8-200 series of aircraft with 197 seats.

As a result, passenger numbers on the route should increase when compared to Summer 2024.

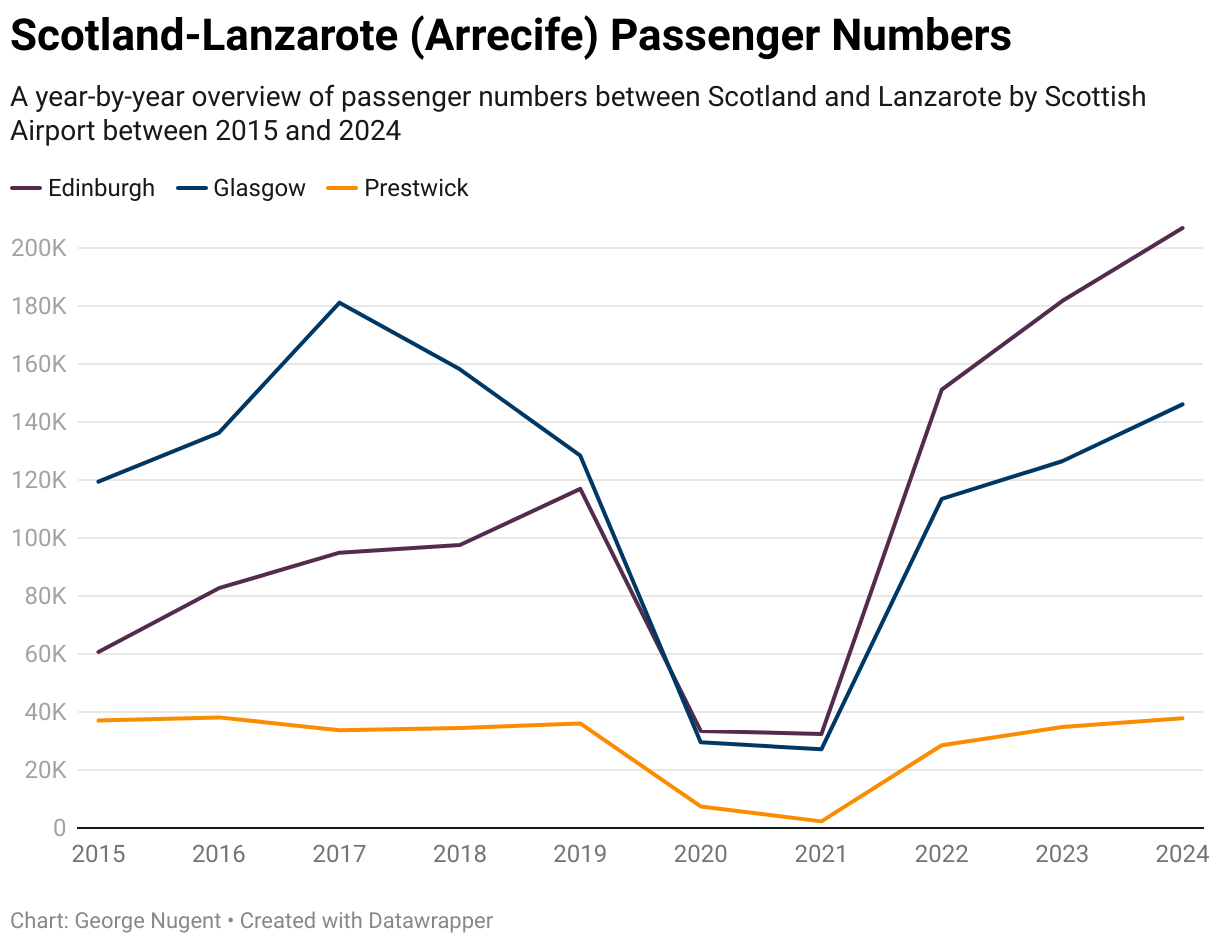

Lanzarote

Lanzarote is another destination that hasn’t been impacted significantly by the pandemic in terms of expected vs actual outcome in terms of passenger numbers. Before the pandemic, Edinburgh was consistently gaining passengers at the expense of Glasgow, all the pandemic did was slow this down.

When taking a wider view of the market, passenger numbers in 2024 were 138.88% of 2019 levels, with the recovery rate for each airport below;

- Edinburgh = 176.92%

- Glasgow = 113.78%

- Prestwick = 104.89%.

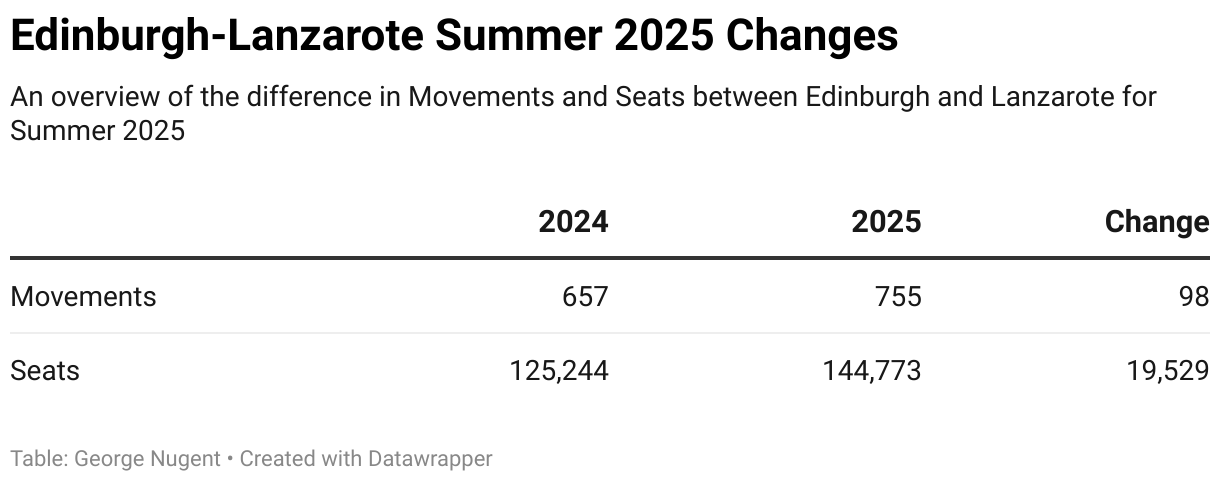

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

easyJet UK

- Movements will increase from 123 to 160 – equivalent to an increase of 30%

- This means increasing from 56.5 to 80 round trips

- Seats available will increase from 22,878 to 29,760 – equivalent to an increase of 30%

Jet2

- Movements will increase from 294 to 295

- This means increasing from 147 to 147.5 round trips

- Seats available will increase from 55,566 to 56,873 – equivalent to an increase of 2%

Ryanair (FR)

- Movements will increase from 180 to 300 – equivalent to an increase of 67%

- This means increasing from 90 to 150 round trips

- Seats available will increase from 35,460 to 58,140 – equivalent to an increase of 64%

Ryanair UK

- Movements will decrease from 60 to 0 – equating to a decrease of 100%

- This means going from 30 to 0 round trips

- Seats available will decrease from 11,340 to 0

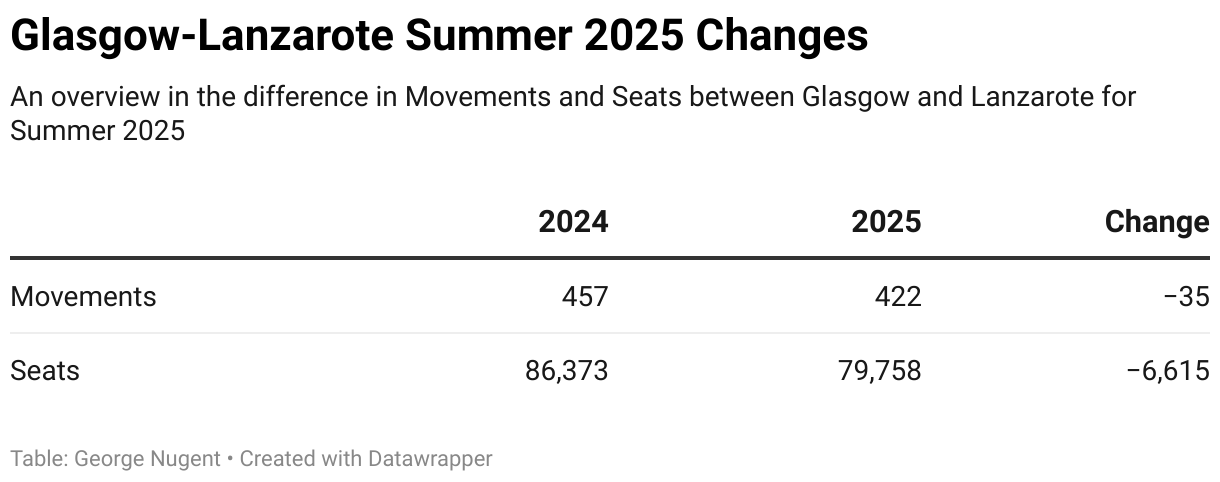

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

Jet2

- Movements will increase from 294 to 302 – equivalent to an increase of 3%

- This means increasing from 147 round trips to 151 round trips

- Seats available will increase from 55,566 to 57,078 – equating to an increase of 3%

TUI

- Movements will reduce from 163 to 120 – equating to a decrease of 26%

- This means reducing from 81.5 round trips to 60

- Seats available will reduce from 30,807 to 22,680 – equating to a decrease of 26%

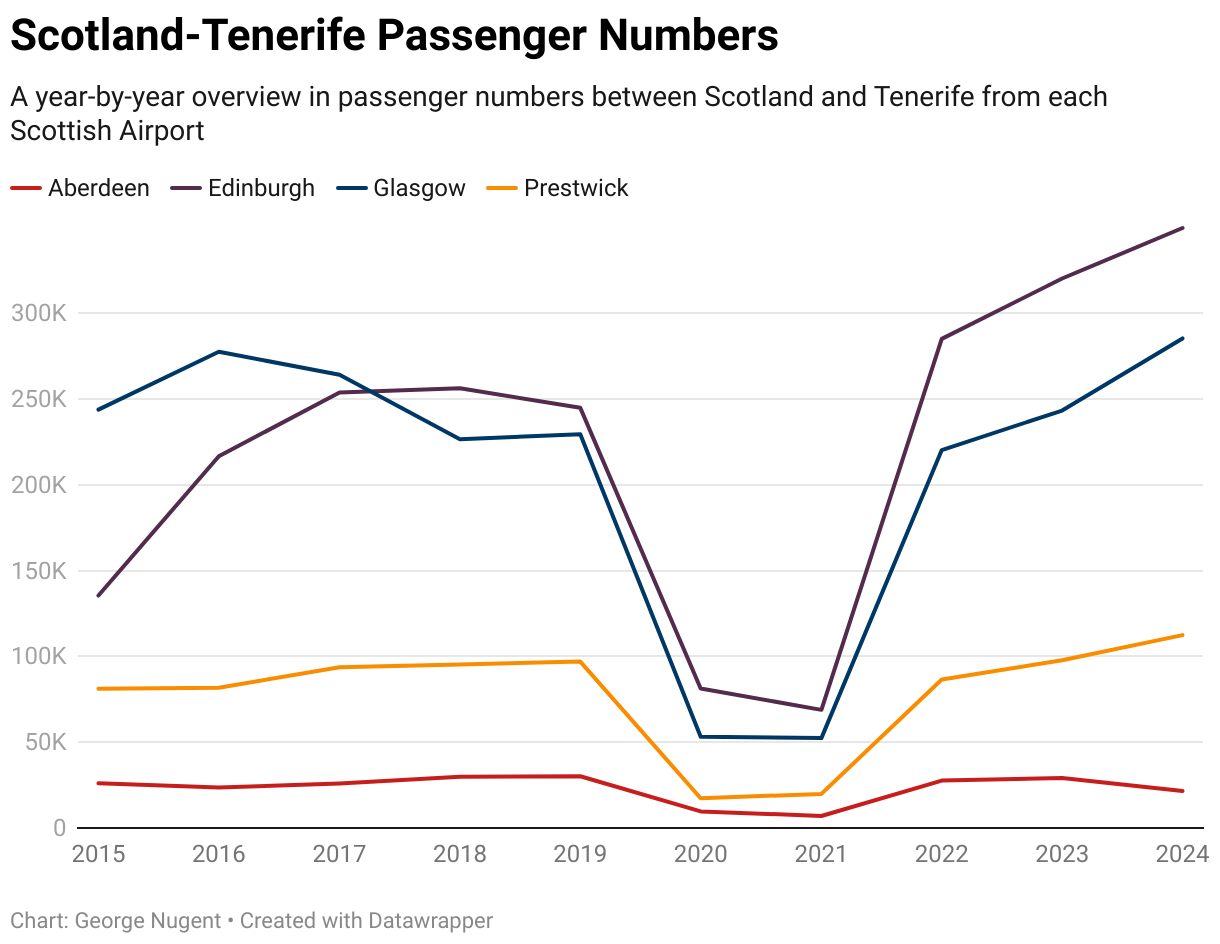

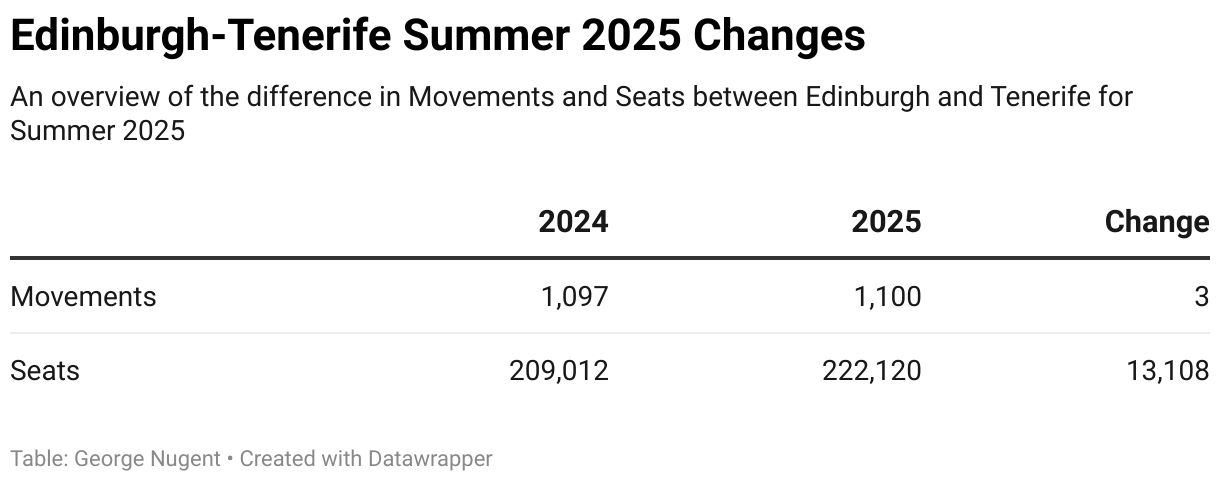

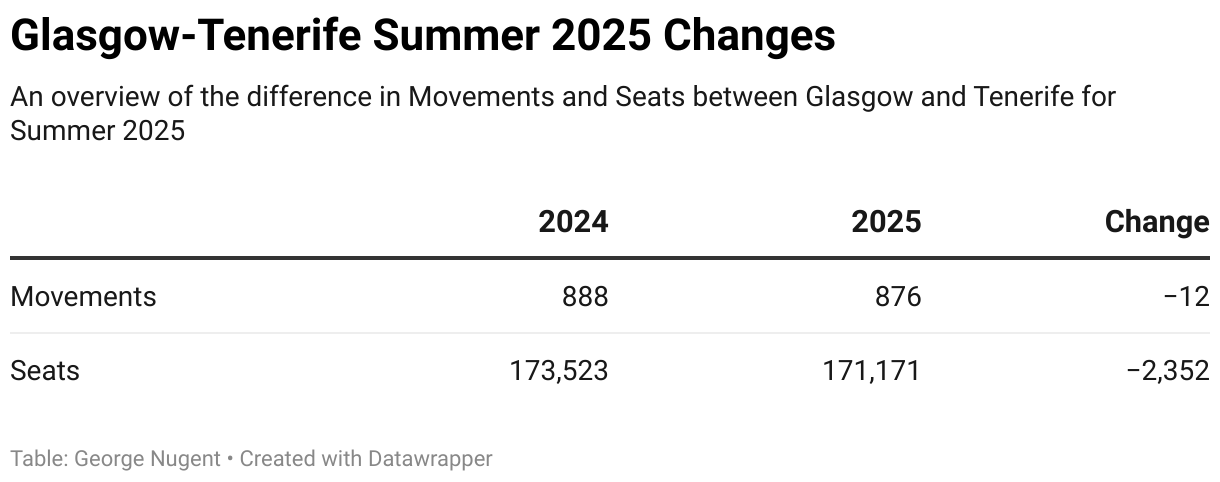

Tenerife

Passenger numbers between Scotland and Tenerife are operating above 2019 levels, however, the central belt of Scotland has been the only area with recovery, as Aberdeen remains below 2019 levels thanks to the removal of TUI’s based aircraft, thus forcing the route to operate in the TUI Winter months only.

Overall, at the end of 2024, passenger numbers were operating at 127.83% of 2019 levels from Scotland, with the recovery rate for each airport listed below;

- Aberdeen = 71.39%

- Edinburgh = 142.81%

- Glasgow = 124.30%

- Prestwick = 115.90%

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Aberdeen Airport shows the following in terms of movements and seats;

TUI

- Movements will remain at 28, the same as Summer 2024

- This means 14 round trips will operate

- Seats Available will remain the same at 5,292

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Edinburgh Airport shows the following in terms of movements and seats;

easyJet UK

- Movements will increase from 299 to 329 – an increase of 10%

- This means increasing from 149.5 to 164.5 round trips

- Seats available will increase from 55,614 to 61,194

Jet2

- Movements will decrease from 456 to 411 – a decrease of 10%

- This means decreasing from 228 to 205.5 round trips

- Seats available will increase from 86,184 to 90,966 – an increase of 6%

- Jet2 will reduce flights, but use larger A321 aircraft on a number of flights to offset this.

Ryanair (FR)

- Movements will decrease from 342 to 300 – a decrease of 12%

- This means decreasing from 171 to 150 round trips

- Seats available will decrease from 67,214 to 58,620 – a decrease of 13%

Ryanair UK

- Movements will increase from 0 to 60, a new service for Summer 2025

- This means 30 round trips will operate

- Seats available will increase from 0 to 11,340

Looking ahead to Summer 2025, the recently published “Start of Season Report” for Glasgow Airport shows the following in terms of movements and seats;

easyJet

- Movements will decrease from 27 to 18 – a decrease of 33%

- This means decreasing from 13.5 to 9 round trips

- Seats available will decrease from 5,022 to 3,348

Jet2

- Movements will increase from 579 to 582 – an increase of 1%

- This means increasing from 289.5 to 291 round trips

- Seats available will increase from 109,431 to 109,998

TUI

- Movements will reduce from 282 to 276 – a decrease of 2%

- This means decreasing from 141 to 138

- Seats available will decrease from 59,070 to 57,825

Moving to Prestwick Airport, no Start of Season Report is published, however, Ryanair will continue to operate 7 weekly flights, and has also upgraded a number of flights to the larger Boeing 737-8-200 series of aircraft with 197 seats.

As a result, passenger numbers on the route should increase when compared to Summer 2024.

Previously Served Destinations

All of the information in this section is about destinations across Spain that are no longer served from any Scottish Airport that saw service between 2015 and 2024.

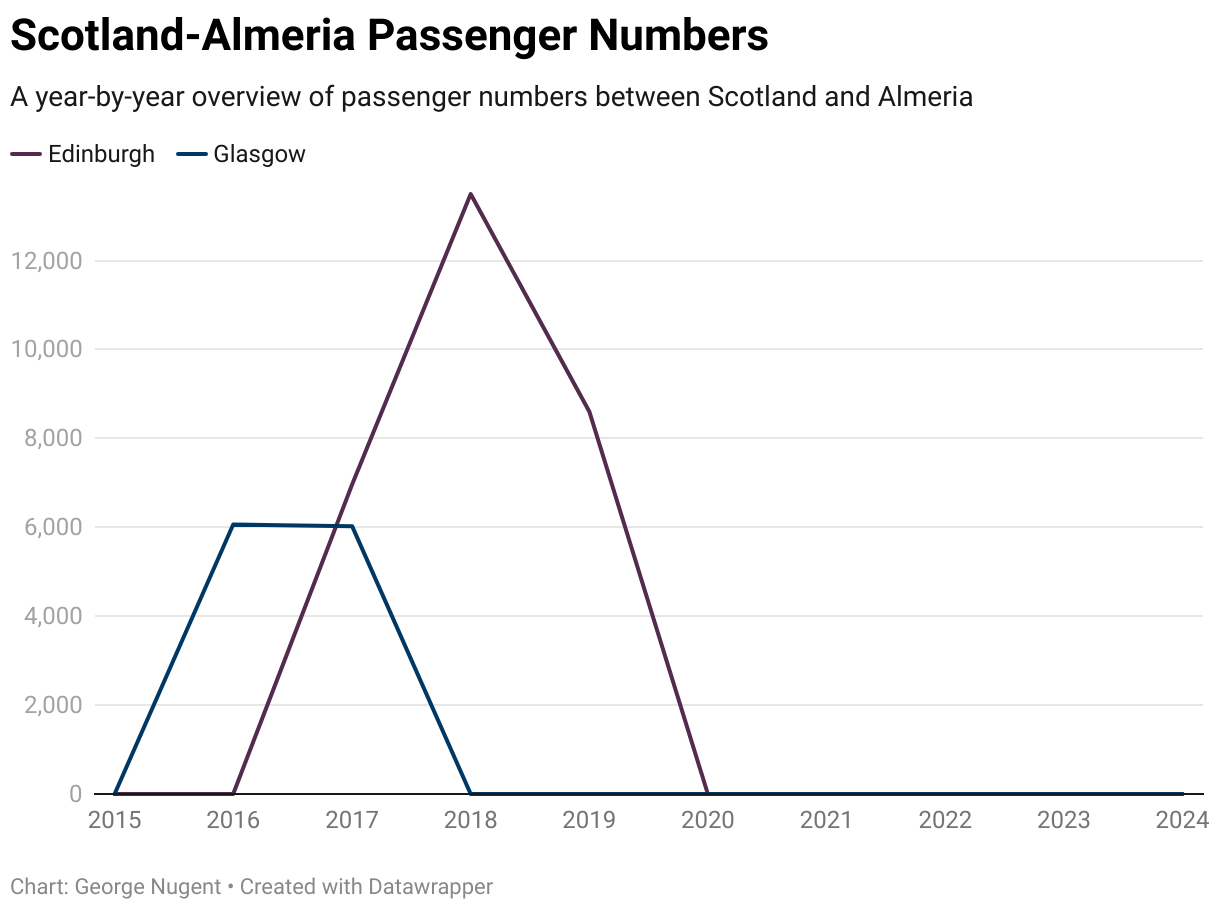

Almeria

Almeria was last served from Scotland in 2019, with flights from Edinburgh Airport, however Glasgow did see a limited number of flights in 2017 and 2018.

Jet2 did intend on launching their own flights from Glasgow to Almeria for Summer 2020, this obviously did not happen thanks to the pandemic, and as of the time of writing, no airline has announced plans for an Almeria service from any airport in Scotland.

It appears that Jet2 has instead decided to focus on rebuilding Girona operations from Scotland instead, with the airline resuming flights from Glasgow in 2023 and Edinburgh in 2026, however, it will be interesting to see if they decide to launch Almeria at some point.

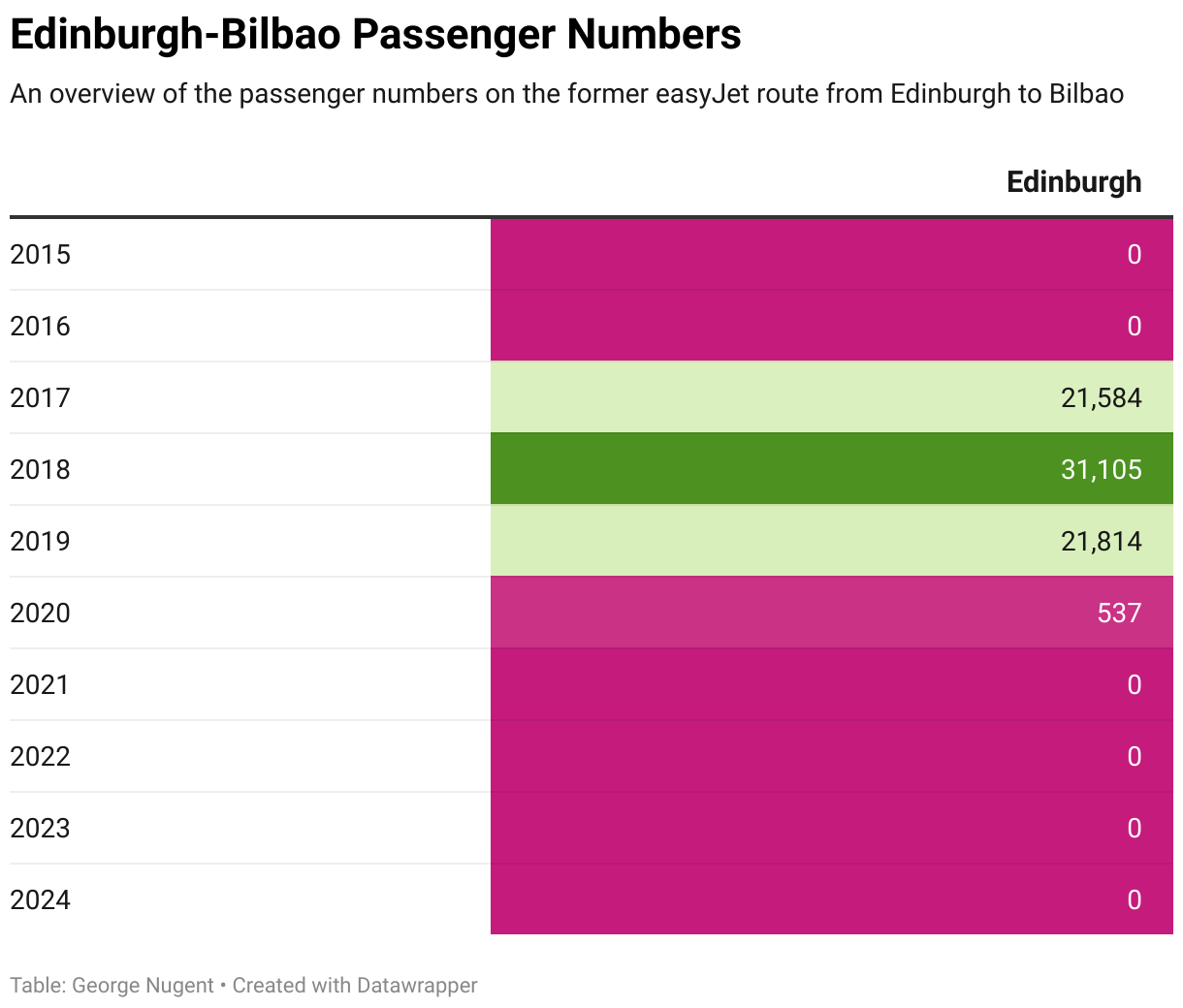

Bilbao

Bilbao was last served from Scotland in 2019, with flights from Edinburgh Airport, these flights were operated by easyJet.

As of the time of writing, no airline has announced any flights from Scotland to Bilbao, however, the city will make a reappearance in CAA Stats from Scotland for 2025 as a result of charter flights for Rangers Europa League matches against Bilbao in April.

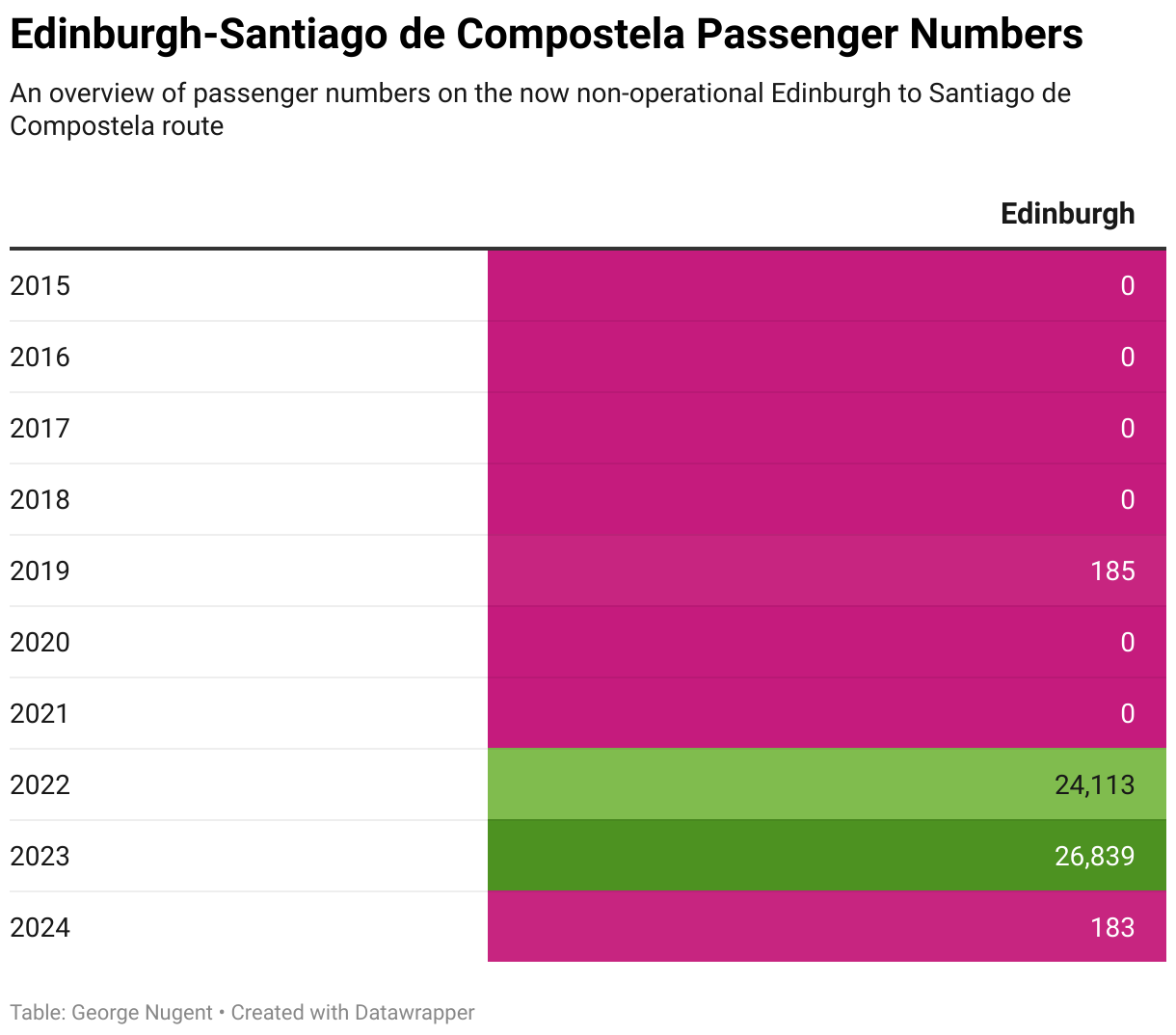

Santiago de Compostela

Santiago de Compostela was last served regularly from Scotland in 2023 with flights operated by Ryanair from Edinburgh Airport.

No official reason was provided by the airline as to why this route was dropped, however, Ryanair has been in a dispute with Spanish Airport Operator AENA over airport charges across Spain, and has made cuts at a number of regional airports across Spain.

Until this dispute is resolved, it is unlikely this route will resume operating any time soon in my opinion.

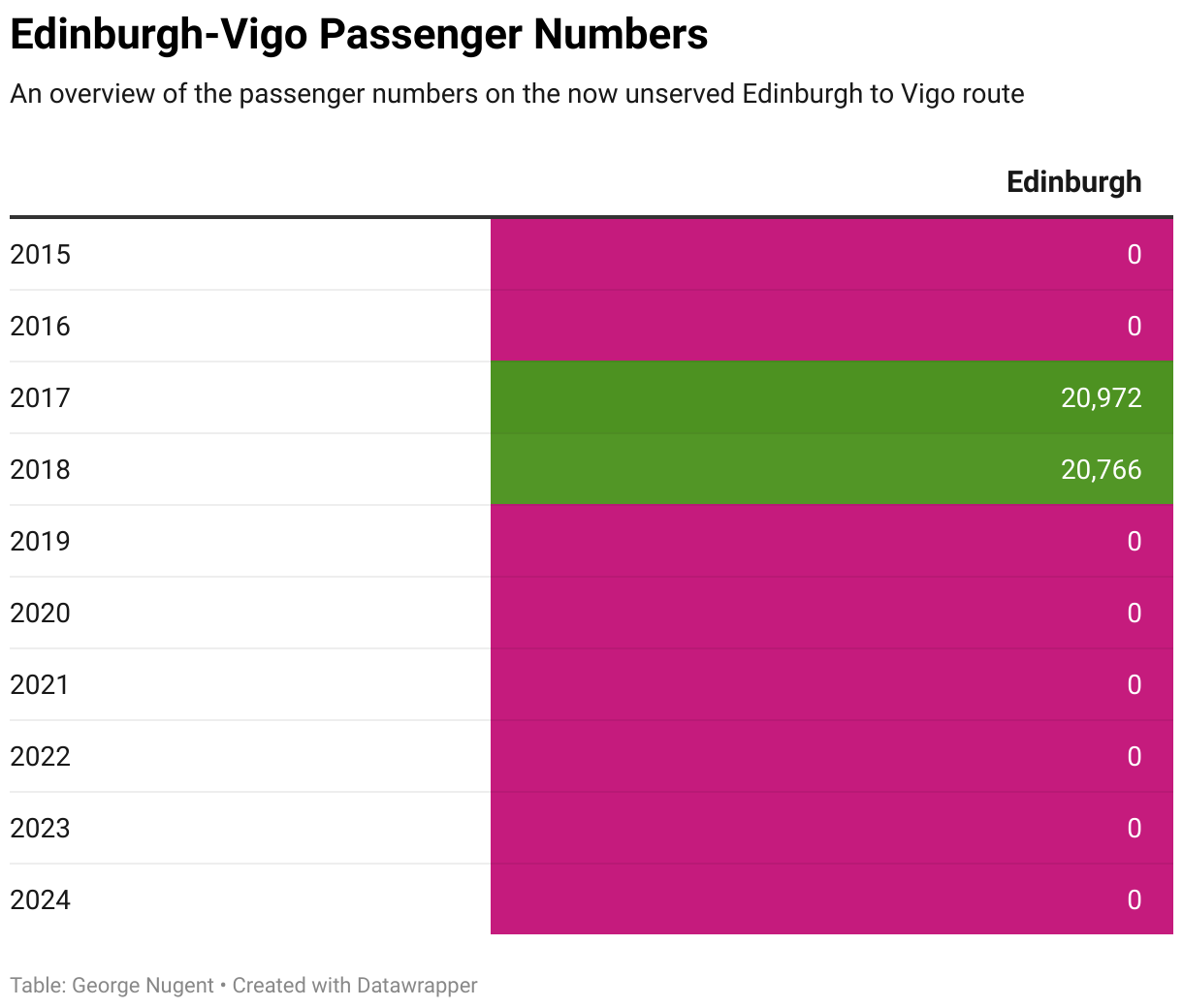

Vigo

Vigo was last served regularly from Scotland in 2018 with flights operated by Ryanair from Edinburgh Airport.

This route remains one of, if not the most, unusual routes that has ever operated from Scotland to anywhere in Spain, and is also, in my opinion the least likely to resume out of the four destinations in this section.

Final Thoughts

I probably don’t need to write this sentence, but this post has been the most data intensive I have ever written, and took me approximately two weeks to collate all of the information and write it.

I was surprised by some routes far more than others, I knew Barcelona was doing well, but I didn’t realise just how big the market was from Scotland, especially from Edinburgh. On the flipside of that, Girona surprised me in just how slow it has been to rebound from the pandemic.

The knock-on effect from the collapse of Thomas Cook in 2019, as well as the consolidation of TUI operations across Scotland at Glasgow Airport has been interesting as well, especially at Aberdeen where there are less airlines available to replace lost capacity on some routes – Tenerife for example.

Looking at Prestwick it has been incredible to see how a once strong airport now has 80% of its route network spread across Spain, even more incredible is how Murcia continues to only operate from the airport, and that it has not followed the usual trend that was occurring in either moving to Edinburgh or being launched at the same time.

Looking ahead to the rest of 2025, it will be interesting to see how this year plays out, especially to the Canary Islands which have been operating well above 2019 levels for the last couple of years, and it is worth remembering that if a slowdown in traffic does occur, it won’t pull the individual routes below 2019 levels.

With British media continuing to report on “Anti-Tourism Protests” across Spain, and also the ongoing Ryanair dispute with AENA, coupled with the rise in other destinations such as Morocco it will be interesting to see if passenger numbers to Spain continue to climb, start to fall, or plateau roughly where they are now.

One thing remains clear, Spain is still a popular destination for Scottish Tourists, and with Iberia, Ryanair and Vueling all serving Scotland, there is a wide range of airlines also suitably catering to the inbound tourist market to Scotland.

About The Author

George Nugent is an independent travel writer focused on honest reviews of rail, air, and coach journeys in the UK, Europe, and USA. Passionate about statistics and clear reporting, George shares insights to help travellers make informed choices.